Buy Shriram Finance Ltd for the Target Rs. 1,200 by Motilal Oswal Financial Services Ltd

Resilient quarter but for minor deterioration in asset quality

FY26 AUM rose 15% YoY; trends in 1HFY27 need to be closely monitored

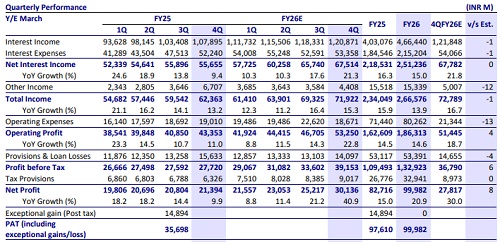

* Shriram Finance’s (SHFL) 4QFY26 PAT rose ~41% YoY to ~INR30.1b (8% beat). FY26 PAT grew 21% YoY to ~INR100b. 4Q NII grew ~21% YoY to INR67.5b (in line). Other income declined ~34% YoY to INR4.4b (12% lower than est.).

* Opex declined ~2% YoY to INR18.7b (13% lower than est.), largely due to sequentially lower employee expenses (3Q had one-time impact from labor code). Transaction costs in the nature of DSA commissions in the 2W loans are now not treated as upfront expenditure and have been amortized at EIR over the loan tenure for loans granted from Jan’26 onward. Consequently, fees and commission expenses were lower by INR515m for the quarter. SHFL guided for a CI ratio of ~26-27%, with operating costs expected to grow at ~10-12% over the medium term.

* 4Q PPoP grew 23% YoY to ~INR53.3b (in line). FY26 PPOP grew ~15% YoY to INR186.3b. Credit costs in 4Q stood at ~INR14.1b (~4% lower than est.), translating into annualized credit costs of ~1.9% (PQ: 1.8% and PY: 2.4%).

* SHFL is targeting 18% AUM growth in FY27, supported by strong capital position and steady demand across key segments. Growth is expected to be led by PV (~20%+) and gold loans (~30%), while CV (~15-18%) and MSME (~13-15%) are likely to witness steady traction, contingent on macro conditions.

* Increasing share of new vehicle financing, alongside continued strength in used vehicles and rising penetration in PL, should support disbursements. Gold loans are set to scale up with distribution expansion, while MSME growth remains calibrated amid external uncertainties.

* Asset quality remained largely stable with no immediate signs of stress, despite a marginal rise in slippages, driven by temporary cash flow mismatches. However, management remains comfortable with the overall risk outlook and expects normalization in slippages, supported by the secured nature of lending and adequate provisioning buffers.

* SHFL delivered a strong FY26 performance with healthy AUM and earnings growth, stable asset quality, and controlled operating costs. Growth visibility remains reasonably robust across key segments, even though risks to growth from macro sensitivity (impact on consumption and economic growth from the West Asia conflict) persist.

* We expect SHFL to deliver a CAGR of ~17%/~26% in AUM/PAT over FY26- 28E, along with RoA/RoE of ~3.8%/13.1% by FY28. Reiterate BUY with a TP of INR1,200 (premised on 2.2x FY28E BVPS).

Margin expansion supported by cost efficiency tailwinds

* Reported NIM rose ~3bp QoQ to ~8.6%. Yields (calc.) declined QoQ by ~25bp to 16.3%, while CoB declined ~15bp QoQ to 8.5%, resulting in spreads of ~7.8% (PQ: 7.9%).

* SHFL’s NIMs improved, supported by lower CoF and favorable repricing of borrowings. Going forward, margins are expected to remain steady with gradual spread expansion and stable yields, even as part of the funding cost benefit is selectively passed on to retain customers.

* The credit rating upgrade is expected to further aid borrowing cost reduction, with management guiding for overall CoB to decline by ~1pp over the next 2-3 years. We expect SHFL to deliver NIM (calc.) of 8.8%/9% for FY27E/ FY28E.

Minor deterioration in asset quality but risks contained for now

* GS3 rose ~4bp QoQ to 4.6% (in the seasonally strongest quarter), while NS3 improved ~5bp QoQ to 2.3%. Net slippages increased ~45bp QoQ to 1.8% (PY: 2.4% and PQ: 1.3%). Stage 2 assets rose ~13bp QoQ to 6.9% (PQ: 6.8% and PY: 6.9%). 30+ dpd rose ~17bp QoQ.

* PCR on Stage 3 rose ~160bp QoQ to ~50% (PQ: ~49% and PY: ~43%). While PCR on S1 was largely stable, PCR on S2 declined ~25bp QoQ to 8%.

* Management indicated that a clearer assessment of the impact from ongoing macro uncertainties will be possible after 1QFY27, as the current environment remains fluid. We build in credit costs (as % of assets) of ~1.9%/1.8% for SHFL for FY27E/FY28E.

Highlights from the management commentary

* Fleet utilization remains healthy, and no immediate concerns are visible; however, a slowdown in consumption could impact utilization and resale values in the coming quarters.

* Demand for used vehicles is expected to remain strong, while tractor demand may soften due to potential monsoon-related concerns.

Valuation and view

* SHFL delivered a resilient operating performance, supported by steady demand across key lending segments and a strong capital base following the MUFG equity infusion, which provides strong headroom to capture growth opportunities. This is further complemented by disciplined cost control and stable credit metrics, aiding profitability and operational efficiency. While the outlook remains constructive, the evolving macro environment warrants close monitoring, with Apr-Jun’26 quarter expected to offer greater clarity on credit trends and underlying demand conditions.

* The stock is currently trading at 2.1x FY27E P/B. We expect SHFL to deliver a CAGR of ~17%/~26% in AUM/PAT over FY26-28E, along with RoA/RoE of ~3.8%/13.1% by FY28. Reiterate BUY with a TP of INR1,200 (premised on 2.2x FY28E BVPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412