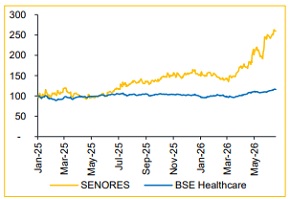

Buy Senores Pharma Ltd For Target Rs.1,640 by Choice Institutional Equities Ltd

SENORES is strengthening its position as a US-focused player through a differentiated product portfolio, expanding commercial presence and integrated manufacturing capabilities. To gain deeper insights into the company's growth strategy and execution roadmap, we visited its Ratnatris Plant and interacted with Mr. Swapnil Shah (MD) and Mr. Deval Shah (CFO). The visit provided valuable insights into the company's US-focussed growth strategy, ANDA pipeline build-out and the newly-created Zoraya and Amerisyn front-end commercial JVs. The management reiterated that ~70% of revenue will continue to come from the US, supported by a visible pipeline of 97 ANDAs (58 approved plus 39 in pipeline which includes 5 approved), addressing a peak TAM of over USD 7 Bn. We believe the front-end JVs – Zoraya (51%-owned, direct marketing) and Amerisyn (70%-owned, government supply) – meaningfully expand SENORES' addressable US market at near-zero incremental capex. This complements a continued CDMO scale-up (commercialised molecules up from 13 to 16). We raise our FY27E/FY28E EPS estimate by 19.5%/19.8% and roll forward our target multiple to 35x (from 30x) FY28E EPS, arriving at a revised TP of INR 1,640. A PEG of 1.1x further provides confidence on our valuation.

* The management reiterated a US-first strategy, targeting ~70% of revenue from the US in the foreseeable future.

* This will be supported by the APNAR facility, which is USFDAapproved and separately approved by Health Canada and the UK MHRA.

* APNAR will also absorb non-government retail volumes shifted from the core US site.

* The ANDA pipeline stands at 58 approved products, of which 22 have launched and 36 are set to launch over the next 8–10 quarters.

* Additionally, 39 own-development pipeline products are in progress, of which 5 are filed.

* This builds to a visible base of 58 approved ANDAs.

* This pipeline places Senores among the top 10 US-focussed Indian pharma companies in terms of product count.

* Two new front-end commercial JVs — Zoraya (51%-owned, direct marketing) and Amerisyn (70%-owned, government/federal supply) — will internalise business earlier routed through third-party partners.

* Both JVs are structured on a profit-share basis (Zoraya: 25% rising to 49% over 2–3 years; Amerisyn: 30%) with minimal upfront investment.

* Zoraya could scale up to USD 200-300 Mn of revenue over time, though the management flagged the ramp-up timeline as uncertain.

* The management was clear this is an additional commercial vertical, not a change in core strategy. ? CDMO's share of the mix is expected to moderate as own-label ANDA revenue scales.

* The CDMO/CMO pipeline stands at 20-25 contracted products.

* R&D is being scaled up meaningfully, with headcount rising from ~50 to 120 within a year. The company also plans to add a new ~30,000 sq. ft. R&D centre.

* FY27E R&D spend is guided at ~6-7% of sales. The management intends to progressively shorten R&D amortisation over the next 2– 3 years.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131