Buy Reliance Industries Ltd for the Target Rs.1,655 by Motilal Oswal Financial Services Ltd

Energy profitability weak; resilient consumer business softens the blow

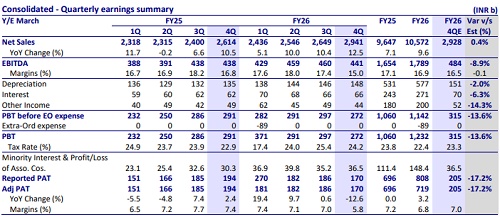

* RIL reported a subdued 4Q, with consolidated EBITDA declining 4% QoQ (flat YoY) to INR441b (vs. our/consensus estimates of INR484b/INR469b), primarily driven by weaker profitability in Energy business due to the disruptions caused by the West Asia conflict. RIL’s consumer-facing businesses remained resilient.

* Reliance Retail’s (RR) revenue growth picked up to 11% YoY, though EBITDA growth was modest at ~3% YoY (flat QoQ, 6% beat), as margins contracted ~60bp YoY (in line) due to the ramp-up of low-margin hyper-local deliveries.

* RJio EBITDA was up ~2.1% QoQ (in line, 14% YoY) driven by ~9.1m net sub adds and stable ARPU (despite two fewer days QoQ). RIL’s digital services EBITDA was up 3.7% QoQ (+16% YoY, in line).

* Consol. O2C EBITDA declined 12% QoQ (down 4% YoY, 20% miss) due to increased crude sourcing premium and higher freight and insurance costs.

* Consol. E&P EBITDA declined 14% QoQ (-18% YoY, 9% miss) due to the natural decline in well production and higher refurbishment costs.

* Attributable 4Q PAT declined 12% YoY to INR170b (-7% QoQ), and was 17% below our estimate due to weaker EBITDA and lower other income.

* Committed capex in 4Q jumped to INR405b (vs. INR338b QoQ, +13% YoY). RIL’s reported net debt rose ~INR76b QoQ to INR1,247b (vs. INR1,171b YoY).

FY26 performance summary:

* RIL’s consolidated EBITDA grew 8% YoY to INR1,789b, while adjusted attributable PAT grew by a modest ~3% YoY to INR719b, due to higher interest and depreciation expenses.

* FY26 committed capex increased ~10% YoY to INR1,443b, while cash capex moderated ~12% YoY to INR1,229b (~20% YoY lower RJio capex).

* Calculated debt (including spectrum liabilities and creditors for capex etc.) inched up by ~INR58b in FY26 to INR2,818b, on our estimates.

* Consol FCF for FY26 improved to INR406b (vs. INR66b), boosted by Asian Paints stake sale. Even excluding other/interest income, RIL’s consolidated FCF improved to ~INR180b (vs. outflow of INR98b YoY), driven by improvement in RJio’s FCF generation (INR213b vs. INR39b YoY).

* We cut our FY27E EBITDA and PAT by 3-4% due to the challenges in the Energy business and delays in tariff hikes in RJio. Overall, we build in a CAGR of 9-10% in RIL’s consolidated EBITDA/adj. PAT over FY26-28E.

* We reiterate our BUY rating with a revised TP of INR1,655 (earlier INR1,715). While the energy business weakness drives the near-term earnings downgrade, sustained mid-to-high teen growth in RR and a tariff hike, along with impending JPL IPO, remain the key triggers for RIL’s stock price.

Reliance Retail – Growth picks up; margin moderates due to QC ramp-up

* RRVL net revenue grew 11% YoY (vs. 9% YoY in 3Q) and was higher at ~14% YoY on a comparable basis (adjusted for FMCG demerger from Dec’25).* Quick commerce (QC) offering, JioMart, has scaled up rapidly, with the number of daily average orders rising 29% QoQ (4x YoY) as hyperlocal deliveries scaled up to electronics and fashion & lifestyle categories, with 2- hour delivery promise.

* Store additions remained calibrated, with 181 net additions (333 additions, 152 closures); retail area inched up 1% YoY to 78.3msf (+0.2msf QoQ).* Operating EBITDA rose by a modest 3% YoY (5% beat) due to an accelerated scale-up of lower-margin hyperlocal deliveries (margin -60bp YoY, in line).

* Despite subdued net area additions, RRVL’s cash capex rose to INR291b (vs. INR187b), while gross block additions remained steady YoY at INR229b.

* FY26 OCF (post interest and leases) improved to INR218b (vs. INR176b YoY), aided by improved profitability and working capital release. FCF outflow rose to INR69b (vs. INR8b outflow YoY) due to elevated capex.

* As a result, RRVL’s effective net debt rose ~INR30b YoY to INR357b.

* We expect store pickup additions and increased momentum in QC to support double-digit revenue growth for RR over the medium term. However, near-term profitability is likely to be adversely impacted by losses in QC.

* We fine-tune our FY27-28 estimates and now project a ~12%/10% CAGR in RR’s revenue and EBITDA over FY26-28.

* Reliance Consumer Brands (RIL’s FMCG arm) delivered INR75b in revenue (2x YoY). Campa surpassed ~INR47b in FY26, sustaining its double-digit market share in key markets. Independence brand delivered INR26b in revenue.

RJio – Largely in line; FCF generation picks up as capex moderates

* RJio’s standalone revenue grew ~2% QoQ (+11% YoY), driven by ~9.1m subscriber net adds. ARPU remained stable (despite two fewer days QoQ).

* EBITDA grew ~2% QoQ (+14% YoY) to INR181b (in line), driven by lower network opex (+1% QoQ, 1% below).

* EBITDA margin expanded ~10bp QoQ to 54.3% (~10bp beat) with incremental EBITDA margin at ~59% (slightly higher vs. our estimate of ~55%).

* JPL’s non-mobility revenue and EBITDA continued to see acceleration, with 8% and 44% QoQ growth, benefitting from rising FWA base and traction in B2B.

* FY26 cash capex (incl. payment of creditors for capex and principal component of spectrum repayments) declined ~20% YoY to INR372b (vs. INR462b YoY), while gross block additions (a proxy for committed capex) in FY26 declined modestly to INR412b (vs. ~INR422b YoY).

* FY26 FCF (post interest, leases and spectrum repayments) improved significantly to INR213b (vs. INR39b in FY25), driven by moderation in capex.

* Effective net debt (including spectrum debt and creditors for capex) declined by INR223b in FY26 to INR1.65t.

* Management expects ~4-5% YoY ARPU growth, driven by customer uptrading and bundling of value-added services in the absence of a tariff hike.

* We cut our FY27 revenue and EBITDA estimates by ~1-2%, led by delays in the tariff hike and rising share of M2M subs in the mix. We continue to build in the next round of tariff hikes (~15% or INR50/month on the base pack) in 2QFY27, but note that there could be a delay of few months to 3Q.

* We expect FY26-28E revenue/EBITDA/PAT CAGR of ~15%/18%/24% for RJio, driven by tariff hike flow-through in wireless and acceleration in FWA offerings. JPL’s IPO is imminent and its valuations remain a key near-term monitorable.

Standalone: Weak O2C and E&P performance drive miss

* Revenue stood at INR1,418b (+7% YoY). EBITDA came in 34% below our estimate at INR120b (est. INR181b; -21% YoY). Reported PAT also stood 38% below our estimate at INR74b (-34% YoY).

* As of 31st Mar’26, RIL’s standalone CWIP stood at INR1,376b (vs. INR824b on 31st Mar’25). Net debt stood at INR688b (vs. INR619b as of 31st Mar’25). In FY26, the company generated CFO of INR791b (flat YoY).

* O2C SA: 4Q EBITDA declined 15% YoY to INR105b, despite strong fuel cracks, as margin gains were offset by higher crude premiums, freight, insurance and fuel costs. Consumer-focused actions (LPG diversion, KGD6 allocation, stable retail fuel prices) led to under-recoveries, while SAED on exports and weak polymer spreads further weighed on profitability.

* Production meant for sale decreased 4% YoY. The Jio-BP network added 283 new outlets in the last 12 months, resulting in robust YoY volume growth of 24%/37% in HSD/MS. Polymer margins declined amid rise in naphtha prices, with PE/PP margins down 4%/28% YoY and PVC margin up 2% YoY. Consol. O2C EBITDA (incl. other income) decreased 4% YoY to INR145b.

* E&P: 4Q revenue declined 8.9% YoY, driven by lower gas realizations in KGD6 and CBM, along with reduced KGD6 volumes (down 6% YoY at 59.6BCFe). KGD6 prices fell to USD9.63/mmbtu (vs. USD10.09/mmbtu), while CBM prices declined to USD9.01/mmbtu (vs. USD10.36/mmbtu). EBITDA dropped 18.1% YoY to ~INR42b due to lower revenue and higher operating costs from maintenance and government levies. Near-term dynamics:

* Energy markets are likely to remain volatile, driven by geopolitics and trade tensions.

* Oil demand is expected to decline marginally by ~0.08 mb/d in CY26. * Constrained refining capacity and prolonged disruptions should keep fuel cracks elevated, with gradual normalization as supply recovers.

* The board has recommended a dividend of INR6/sh (FV: INR10/sh).

Valuation and view

* We cut our FY27E EBITDA and PAT by 3-4%, due to challenges in the Energy business and delays in tariff hikes in RJio.

* We expect RJio to remain the biggest growth driver (digital to contribute ~80% of RIL’s incremental EBITDA), with 18% EBITDA CAGR over FY26-28E, driven by the wireless tariff hike (~15% in 2Q), market share gains in wireless, and the continued ramp-up of Homes and Enterprise offerings.

* We expect RR to deliver ~12% revenue CAGR over FY26-28E, driven by a mix of store rollouts, improved productivity and scale-up of hyper-local offerings. However, the faster ramp-up of lower-margin businesses could weigh on blended EBITDA margin, driving ~10% EBITDA CAGR over FY26-28E.

* After a subdued FY25, RIL’s O2C EBITDA improved in FY26 but was hit by higher crude premiums and high freight and insurance costs due to the West Asia conflict. Going ahead, we expect only a modest recovery over FY26-28E. Our FY28E consolidated EBITDA for O2C and E&P is broadly similar to FY24. * Overall, we build in a CAGR of ~9-10% in RIL’s consolidated EBITDA and PAT over FY26-28E.

* We model an annual consolidated capex of INR1.25t for RIL over FY26-28E (similar to FY25) as we believe the peak of capex is likely behind, which should lead to healthy FCF generation (~INR1t over FY26-28E) and a corresponding decline in consol. net debt.

* For RR, we ascribe a blended EV/EBITDA multiple of 28x (30x for core retail and ~6x for connectivity) to arrive at an EV of ~INR8.5t (or ~USD91b) for RRVL and an attributable value of INR500/share (earlier INR550/share) for RIL’s stake in RRVL. Sustained mid-teen revenue growth in RR remains the key for RIL’s re-rating.

* We value RJio on DCF implied ~11.6x Mar’28E EV/EBITDA to arrive at our enterprise valuation of INR11.3t (USD120b) and assign ~USD8b (INR740b) valuation to other non-mobility offerings under JPL to arrive at INR12t (or ~USD128b) enterprise valuation for RIL’s digital services segment. Factoring in net debt and ~33.5% minority stake, the attributable equity value for RIL comes to INR525/share (vs. INR540 earlier).

* Using the SoTP method, we value the O2C/E&P segments at 7.5x/5.0x Mar’28E EV/EBITDA to arrive at an enterprise value of INR5.8t (or ~INR427/sh) for the standalone business. We ascribe an equity valuation of INR525/sh and INR500/sh to RIL’s stake in JPL and RRVL, respectively. We assign INR174/sh (~INR2.4t equity value) to the New Energy business, INR26/sh (~INR350b) to RIL’s stake in JioStar and INR39/sh (~INR530b, based on 2x FY28 gross sales) to RCPL (RIL’s FMCG arm). We reiterate our BUY rating with a revised TP of INR1,655 (earlier INR1,715).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

.jpg)