Buy Monolithisch India Ltd. for Target Rs. 960 by Choice Institutional Equities

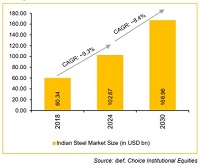

A Refractory-Led Play on India’s Steel Capacity Expansion: India’s crude steel production is expected to increase from 168.4 MnT in FY26 to 255 MnT by FY31, with the induction furnace (IF) route remaining a key contributor to growth. As induction furnace steel production expands from 45.8 MnT to 69.4 MnT during the same period, demand for ramming mass - a critical refractory consumable used in induction furnaces - is expected to grow in tandem. With a strong presence in Eastern India, which houses most of the country’s IF steel capacity, MONOLITH is well positioned to benefit from this structural demand growth. Unlike steel producers, whose earnings are influenced by commodity price movements, MONOLITH’s growth is primarily driven by steel production volumes, providing a relatively visible and recurring demand outlook.

Structural Advantages Driving Market Share Gains: The market share expansion is supported by three key structural catalysts: the formalisation of the unorganised sector, higher furnace throughput, which increases replacement demand and an ironclad logistics advantage. By strategically locating its manufacturing base within the Eastern India steel belt, MONOLITH enjoys a non-replicable freight cost advantage of INR 800 - 1,200 per tonne versus western competitors, strengthening both its competitiveness and profitability.

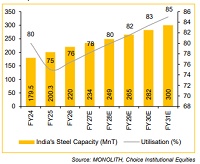

Capacity Multiplication and Operating Leverage Propel Revenue Trajectory: MONOLITH is entering a new growth phase with installed capacity increasing from ~2,10,000 MTPA to ~5,75,000 MTPA by early FY27. The expanded capacity provides a platform for higher production and sales volumes, which are expected to grow from 1,71,200 MT in FY26 to 4,87,300 MT by FY29E. Alongside volume growth, realisations are projected to improve, driven by a better product mix and favourable demand conditions. The combination of higher volumes and improving realisations is expected to drive revenue growth from INR 1,353 Mn in FY26 to INR 4,532 Mn by FY29E. As utilisation levels increase to ~85% by FY29E, operating leverage is expected to support further margin expansion, resulting in earnings growth outpacing revenue growth over the forecast period.

Target Price Derivation - EV/EBITDA Methodology: Based on our EV/EBITDA valuation framework, we apply a 22x multiple to FY28E consolidated EBITDA of INR 926 Mn to arrive at an EV of INR 20,374 Mn. We derive a target price of INR 960 per share and initiate coverage with a BUY rating, implying a 48.6% upside from the current market price of INR 647.

Unpriced Optionality: Potential migration to the NSE Main Board, geographical expansion beyond Eastern India and opportunities for backward integration provide additional optionality beyond our forecasts. These initiatives could support higher earnings growth and valuation re-rating over time.

Key Risks: Capacity expansion execution delays, high customer concentration risk, elevated working capital cycle, competitive intensity and slower market share gains, SME market liquidity and valuation de-rating risk.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

Tag News

Healthcare Sector Update : Pan-India operator built on an acquisition-led playbook by Emkay ...

More News

Renewable Equipments Sector Update : MNRE extends ALMM List-II exemption till Dec'26 by Prab...