Buy Jindal Steel Ltd for the Target Rs. 1,400 by Motilal Oswal Financial Services Ltd

Operating performance beat over better volume and NSR; outlook remains strong

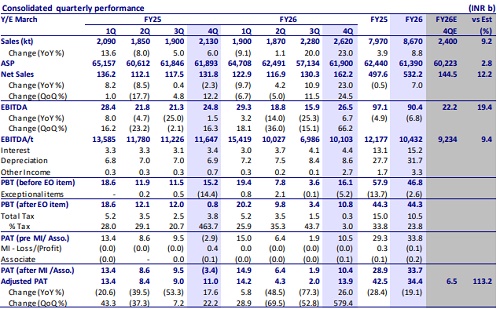

* Jindal Steel’s(JINDALST) revenue stood at INR162b (+23% YoY and +25% QoQ), against our estimate of INR145b during 4QFY26. The growth was primarily attributed to strong volume and realization during the quarter.

* Production for 4QFY26 stood at 2.65mt (+26% YoY and +6% QoQ),mainly driven by newly added Angul capacity, whereas sales volume stood at 2.6MT (+23% YoY and +15% QoQ). Share of exports declined to 5% in 4QFY26 vs 6% in 3QFY26. Net realization rose 8% QoQ (flat YoY) to INR61,000/t on account of strong recovery in steel prices during the quarter.

* Adj. EBITDA stood at INR27b, rising 7% YoY and 66% QoQ (against our est. of INR22b), led by strong volume and NSR improvement. This translates into EBITDA/t of INR10,100 (-13% YoY and +45% QoQ) vs our estimate of INR9,250/t in 4QFY26.

* APAT for the quarter stood at INR13.9b (+26% YoY), vs INR2b in 3QFY26.

* In FY26, revenue came in at INR530b (+7% YoY), while EBITDA and PAT stood at INR90.4b (-7% YoY) and Adj. PAT was INR34.4b (-19% YoY). FY26 sales volumes grew by 9% YoY to 8.7mt, while NSR declined 2% YoY to INR61,390/t. The NSR moderation led EBITDA/t to decline by 14% YoY to INR10,432/t.

* Net debt stood at INR160b as of Mar’26, translating intoNet debt/EBITDA of 1.66x in 4QFY26, compared to 1.72x in 3QFY26. Total capex for the quarter was INR25.7b, largely driven by expansion projects at Angul.

* The Board has recommended final dividend of INR2/share in FY26.

Key highlights from the management commentary

* The company hassuccessfully ramped up the new Angul capacity and expects to close sales volume of 10.5-11mt in FY27.

* The mix of Flat and Long stood at 52% and 48% during 4QFY26. ? NSR has improved by INR4,700 QoQ, and steel prices continue to remain firm in April.

* Coking coal costs were USD20/t higher in 4QFY26 and are expected to increase by USD20-25/t in 1QFY27 on a consumption basis.

* The company will continue to utilize the by-product internally to cater to the metallic requirements of the newly added capacity.

* The slurry pipeline is expected to be commissioned in 1HFY27 and save INR750-1,000/t of costs once fully ramped up.

Valuation and view – reiterate BUY

* JINDALST’s 4QFY26 performance was strong on account of higher NSR and improved volumes, driven by the recently added capacity. We expect earnings to improve in FY27, aided by steel price recovery and volume from capacity ramp-up, which could be partially offset by an increase in coking coal costs.

* We expect the long-term outlook to remain positive for the company. With the recentincrease in its crude steel capacity to 15.6mtpa and finished steel to 13.8mtpa, there issignificant headroom for earnings growth. With the safeguard duty in place, we expect steel prices to remain steady at healthy levels and support margins.

* A large proportion of capex has already been incurred, and the rest would be funded through internal accruals, keeping net debt/EBITDA below the threshold level of 1.5x. Net debt stood at INR160b as of FY26-end, translating into a net debt/EBITDA of 1.7x in 4QFY26.

* We cut our EBITDA estimates for FY27 by 9% to incorporate the increase in coal costs and the gradual improvement in volumes. We largely retain our estimates for FY28. At CMP, the stock trades at 7.8x EV/EBITDA on FY28E. We reiterate our BUY rating with a TP of INR1,400, based on 8.5x EV/EBITDA on the FY28 estimate.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)