Buy Indigo Paints Ltd for the Target Rs 1,250 by Motilal Oswal Financial Services Ltd

In-line revenue; focus on market share gain

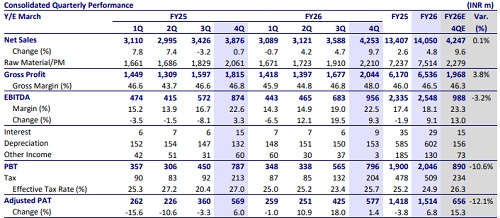

* Indigo Paints (INDIGOPN) reported standalone sales growth of 8% YoY in 4QFY26 on a soft base (flat), while FY26 revenue growth stood at 5%. The company witnessed double-digit growth at the consumer level from Nov’25 onwards, though higher trade incentives impacted primary performance. The Paint industry implemented ~12% cumulative price hikes, and Apr’26 growth was supported by dealer stocking ahead of price increases. Management expects the improving demand trajectory to continue in FY27, though the sustainability of demand momentum will need to be monitored over the coming months. Apple Chemie (subsidiary) reported strong revenue growth of 35% YoY. Consolidated revenue grew 10% YoY (base +1%) to INR4.3b (in line).

* Gross margin expanded 120bp YoY to 48%, supported by an improved product mix, sustaining its position among the best in the industry (Exhibit 1). Management indicated willingness to forgo 200-250bp of GM to drive faster topline growth and market share gains through higher trade incentives and influencer programs. Higher A&P spends (5.6% vs 5.0% in 4QFY25) and employee expenses (up 28% YoY) kept EBITDA margin largely flat at 22.5% (est. 23.3%).

* The paint industry continues to face raw material inflation amid the ongoing West Asia conflict, though cumulative price hikes undertaken by companies have largely offset the impact. The industry is expected to witness double-digit revenue growth in FY27, aided by sharp pricing actions. INDIGOPN aims to outperform the industry through a stronger focus on premium emulsions and differentiated products.

* We model a CAGR of 15%/15% in revenue/EBITDA in FY26-28E. We model an EBITDA margin of 17.1%/18.2% for FY27/FY28. We reiterate our BUY rating with a TP of INR1,250 (based on 28x FY28E EPS), considering its growth outperformance, synergies with Apple Chemie, consistent capacity and distribution expansion, and its favorable valuation multiples vs. peers.

Highlights from the management commentary

* Management indicated that Apr’26 witnessed strong growth across the paint industry, aided by multiple price hikes and dealer stocking ahead of price increases. The company noted a certain degree of channel inventory buildup.

* Sharp raw material inflation and supply disruptions following the Iran war severely impacted smaller and MSME paint players, many of whom struggled to procure raw materials or pass on price hikes effectively.

* The company had more than 12,200 tinting machines and 55 depots across all 28 states. It continues to deepen its presence in Tier-3 and Tier-4 markets while simultaneously expanding in Tier-1 and Tier-2 cities.

* Management stated that no major capex is planned until FY29 as the heavy investment cycle is now largely complete

Valuation and view

* We broadly maintain our EPS estimates for FY27 and FY28.

* INDIGOPN's strategic shift to focusing on non-metro towns and increased investments in distribution and influencers as part of its Strategy 2.0 are proving to be successful endeavors. That said, the company continues to focus on the premium and emulsion segments, with a deliberate shift away from the economy segment.

* We model a CAGR of 15%/15% in revenue/EBITDA in FY26-28E. We model an EBITDA margin of 17.1%/18.2% for FY27/FY28. We reiterate our BUY rating with a TP of INR1,250 (based on 28x FY28E EPS), considering its growth outperformance, synergies with Apple Chemie, consistent capacity and distribution expansion, and its favorable valuation multiples vs. peers

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)