Buy HCL Technologies Ltd for the Target Rs. 1,650 by Motilal Oswal Financial Services Ltd

FY27 guidance soft on the back of muted 4Q

Client-specific issues cloud the outlook, made worse by AI deflation

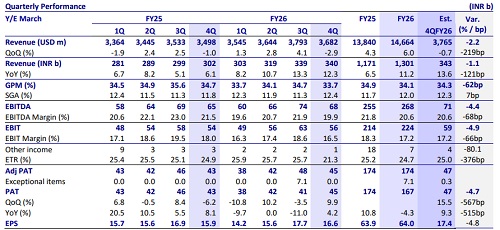

* HCL Technologies (HCLT) reported 4QFY26 revenue of USD3.7b, which declined 3.3% QoQ CC, below our estimate of 0.9% QoQ CC decline. EBIT margin came in at 16.5% vs. our estimate of 17.2%. New deal TCV was USD1.9b (up 35.4% YoY) in 4QFY26. For FY27, revenue growth is guided at 1–4% YoY in CC. Services revenue growth is expected to be between 1.5% and 4.5% YoY in CC (vs. our expectations of 3–6%). EBIT margin guidance of 17.5–18.5% is in line.

* For FY26, revenue/EBIT grew 11.2%/4.6%, while adj. PAT was flat YoY in INR terms. We expect revenue/EBIT/PAT to grow 12.6%/21.0%/8.4% YoY in 1QFY27. Free cash flow stood at 107% of net profit for FY26. FY26 RoE came in at 24.5% (vs. 25.2%/23.5%/23.3% in FY25/FY24/FY23). The company’s relative growth premium vs. large-cap peers narrows in the near term, although its diversified, infra-heavy portfolio remains a structural positive. We reiterate our BUY rating on HCLT with a TP of INR1,650, implying a 15% potential upside.

Our view: AI deflation starting to bite the industry

* Soft guidance due to client-specific situations as well as the March weakness: FY27 guidance of 1–4% YoY CC reflects a combination of client-specific disruptions in March and sharp discretionary cuts in telecom (by two large US clients). In addition, two large client-specific headwinds (one retail, one manufacturing) are expected to create ~50bps drag on services growth in FY27. Europe remains weak due to geopolitical issues, while North America is stable barring these client situations. Software weakness was also led by deal deferrals (the US government shutdown and West Asia crisis).

* That said, this performance is a miss on guidance: HCLT’s premium multiple is premised on the fact that it can grow faster than other largecaps; at the midpoint, that growth premium disappears. We now expect ~3.0% services growth (organic). Importantly, the full impact of the client-specific issues is yet to play out, and we expect 1H to be soft. This, along with a lower-than-expected improvement in FY27 margins, would put HCLT's EPS growth premium at risk in the near term.

* HCLT calls out a 2–3% deflationary impact from GenAI: HCLT’s service line is less exposed to GenAI deflation, with ~2–3% drag on its revenues. For the industry, HCLT estimates a higher drag of 3–5%; taken over 4–5 years, this implies 15–20% of revenues at risk – higher than earlier expected, with the risk that AI swallows a larger part of the services stack.

* Margins guided in-line; reinvestment offsets currency tailwinds: FY27 EBIT margin guidance of 17.5–18.5% is in line. Management indicated that benefits from currency depreciation will be reinvested into sales and GenAI capability buildout, rather than flowing through to margins. Underlying margins remained resilient, but no meaningful operating leverage is expected in the near term.

* Need clarity on AI deflation vs. client-specific issues; the long-term thesis of HCLT's portfolio being more resilient still intact: Near-term performance is impacted by a mix of client-specific issues and early-stage AI deflation, and the interplay remains a key monitorable. That said, HCLT’s exposure to ER&D, chip design, and infrastructure management makes it relatively more resilient vs. application-heavy peers. It has played out in previous downcycles, and we continue to hold this thesis despite today's results.

First cut – 4QFY26: Miss on revenue and margins; FY27E services guidance at 1.5-4.5%

* HCLT’s revenue declined 3.3% QoQ in CC, below our estimate of a 0.9% QoQ CC decline. FY26 revenue stood at USD14.7b, up 6% YoY.

* New deal TCV stood at USD1.9b (down 35.6%/up 35.4% QoQ/YoY) in 4QFY26. For FY26, deal TCV stood at USD9.3b, up 0.6%.

* The IT business grew 0.1% QoQ cc, while ER&D/P&P dipped 1.3%/28.1% QoQ cc.

* For 4QFY26, the EBIT margin was 16.5%, below our estimate of 17.2%. For FY26, EBIT margin stood at 17.2% vs. 18.3% in FY25.

* For FY27, revenue growth guidance was given at 1–4% YoY in CC. Services revenue growth is expected to be between 1.5% and 4.5% YoY in CC (vs. our expectations of 3–6%). EBIT margin guidance of 17.5–18.5% is in line.

* In 4QFY26, adj. PAT declined 6.5% QoQ, but it was up 4.2% YoY to INR45b vs. est. of INR47b.

* LTM attrition improved 10bp QoQ to 12.5%. Net employee headcount improved by 0.4% in 4QFY26 and stood at 2,27,181 as at the end of 4QFY26. HCLT added 1,712 freshers in this quarter.

* LTM FCF to net income stood at 107%.

* The management declared an interim dividend of INR12/share for 4QFY26.

Key highlights from the management commentary

* FY26 saw continued macro uncertainty – tariff changes, lower discretionary spending in traditional IT, and some client cost-cutting; AI-related spending provided partial support.

* Cost-takeout and vendor consolidation continue to dominate the deal mix; discretionary IT spending remains soft across the board, with select telecom clients cutting spend meaningfully for CY26.

* The telecom vertical is the most significant near-term headwind – two large US telecom clients cut discretionary IT spending (digital business and engineering services) during 4QFY26. The impact is expected to persist through CY26 and is fully baked into the lower end of FY27 guidance.

* North America remains the most resilient region with no broad macro challenges; however, two client-specific situations (one retail, one manufacturing) will create a 50bp services growth headwind in FY27.

* AI deflation is estimated at 2-3% incremental impact on HCLT's portfolio mix (vs. the broader industry’s 3-5% range); management views very little of this as having played out in reported numbers yet – the impact is likely to accelerate from FY27.

* Two acquisitions were completed in FY26: 1) Wabi Data Intelligence AI (augments software data offerings); and 2) a definitive agreement signed for Solutions (Singapore-based wealth consulting – adds core banking and wealth management capabilities to BFSI portfolio).

Valuation and view

* We now expect HCL Technologies to deliver a CAGR of ~4.0% over FY25–28 in USD revenue with 17.9% EBIT margin for each year, factoring in softer FY27 guidance, client-specific headwinds, and early signs of GenAI-led deflation. The company’s relative growth premium vs. large-cap peers narrows in the near term, although its diversified, infra-heavy portfolio remains a structural positive. We trim our estimates by 2.5%/4.2% for FY27/FY28E. We reiterate our BUY rating with a revised TP of INR1,650 (based on 20x FY28E EPS).

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)