Buy Happy Forgings Ltd for the Target Rs 1,652 by Motilal Oswal Financial Services Ltd

Earnings beat led by better-than-expected margins Healthy demand momentum likely to sustain

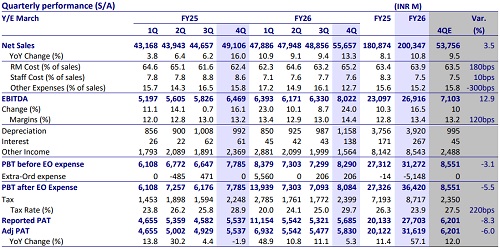

* Happy Forgings’ (HFL) 4QFY26 earnings at INR836m beat estimates by 5%, led by better-than-expected margin, even as revenue was in line with our estimates. EBITDA margin expanded 240bp YoY to 31.5% (vs an estimate of 30.4%), recording a new high.

* Led by a better-than-expected performance in 4Q and a strong outlook, we have raised our FY27/FY28E EPS by 7%/6%. Given its healthy new order wins, we expect HFL to post a 25% standalone revenue CAGR over FY26-28. Further, while there could be some margin pressure due to rising input costs in the near term, we expect HFL to post a 60bp margin expansion to 31% over FY26-28, led by an improved mix, operating leverage benefits, and the advantage of solar power generation in the coming years. We, thus, expect HFL to post a 31% earnings CAGR over FY26-28. We reiterate our BUY rating on the stock with a TP of INR1,652 (based on 30x FY28E EPS).

Earnings beat led by better-than-expected margins

* Standalone revenue grew 20.4% YoY in 4Q to INR4.2b (in line), driven entirely by volume growth, which stood at 17,298 MT. Realization/kg remained flat at INR245.

* Revenue mix in FY26 (vs. FY25): CV- 37% (38%), Farm Equipment - 32% (32%), Off-highway - 11% (12%), Industrials - 14% (14%), PV - 6% (4%). Domestic – 74% (71%), Deemed Exports – 11% (11%), Direct Exports – 15% (18%).

* EBITDA margins expanded 240bp YoY to 31.5% (100bp above est.) on the back of an improving product mix and operating leverage. As a result, EBITDA grew 30% YoY to INR1.3b (5% above est).

* PAT grew 23% YoY to INR836m vs. est. of INR797m due to strong margin performance.

* FY26 performance: Revenue/EBITDA/PAT grew 10%/16%/13% to INR15b/INR5b/INR3b. OCF/FCF stood at +INR4.4b/-INR163m in FY26 vs. +INR2.9b/+INR119m in FY25. RoE/RoCE stood at 15.2%/13.6%, respectively.

Valuation and view

HFL’s cost-competitive advantage is expected to help the company drive sustainable outperformance to the core. Supported by a better-than-expected performance in 4Q and a strong outlook, we have raised our FY27/FY28E EPS by 7%/6%. Given its healthy new order wins, we expect HFL to post a 25% standalone revenue CAGR over FY26-28. Further, while there could be some margin pressure due to rising input costs in the near term, we expect HFL to post a 60bp margin expansion to 31% over FY26-28, led by an improved mix, operating leverage benefits, and the advantage of solar power generation in the coming years. We, thus, expect HFL to post a 31% earnings CAGR over FY26-28. We reiterate our BUY rating on the stock with a TP of INR1,652 (based on 30x FY28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Buy Time Technoplast Ltd for the Target Rs 280 by Motilal Oswal Financial Services Ltd