Buy Ellenbarrie Industrial Gases Ltd for the Target Rs 330 by Motilal Oswal Financial Services Ltd

Capacity ramp-up and margin improvement to drive earnings Earnings (adjusted for non-recurring items) in line

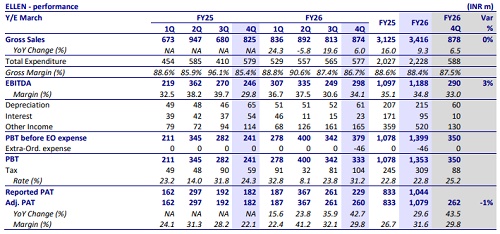

* Ellenbarrie Industrial Gases (ELLEN) delivered a strong performance in 4QFY26, with adj. EBITDA increasing 21% YoY to INR298m (adjusted for the impact of a one-time provisioning for employee leave encashment and a one-time settlement with an onsite customer), reflecting improving operating leverage in the core gases business

* We expect growth momentum to accelerate, driven by the ramp-up of the Uluberia-II (220 TPD) facility, commissioning of the East India onsite plant (320 TPD) in 1QFY27, and upcoming merchant plants in North and Central India expected to become operational in FY27 and FY28, respectively.

* We raise our earnings estimates of FY27/FY28 by 6% each, driven by the rampup of the newly commercialized plants and the strategic efforts towards power cost optimization. We reiterate our BUY rating with a TP of INR330 (based on 26x FY28E EPS).

Strong operating leverage in the gases segment offsets weakness in project engineering

* ELLEN reported a total revenue of INR874m (in line) in 4QFY26, up ~6% YoY.

* EBITDA adjusted for a one-time provisioning for employee leave encashment and a one-time settlement with an onsite customer grew 21% YoY to INR298m. Adj. EBITDA margin stood at 34.5% (est. 33%) vs. 29.8% in 4QFY25.

* Adj. PAT grew 43% YoY to INR260m (est. INR262m; further adjusted for other income – impairment on a legacy non-core investment).

* Gases, related products & services revenue grew 8% YoY to INR860m, EBIT grew 31% YoY to INR343m, and EBIT margin was 40% (vs. 33% in 4QFY25).

* Project engineering revenue stood at INR14m (down 53% YoY), and operating loss stood at INR24m (vs. the operating loss of INR14m in 4QFY25)

* For FY26, the company’s revenue/EBITDA/adj. PAT grew 9%/6%/25% to INR3.4b/INR1.2b/INR1b

* CFO as of Mar’26 stood at INR1.3b compared to INR42.8m as at Mar’25

Valuation and view

* Going forward, the company’s strategic efforts towards power-cost optimization led by the Power Purchase Agreement, along with higher contributions from Argon and capacity ramp-up, are expected to improve margins.

* Further, ELLEN’s growth story will be led by

1) capacity expansion across India,

2) normalization of Argon prices along with stable prices of Oxygen and Nitrogen,

3) increasing traction in the solar cell segment,

4) stable demand from well-diversified core industries

5) ramp-up of Uluberia-2.

* We raise our earnings estimates of FY27/FY28 by 6% each, fueled by the rampup of the newly commercialized plants and the strategic efforts towards power cost optimization. We reiterate our BUY rating with a TP of INR330 (based on 26x FY28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412