Buy Delhivery Ltd for the Target Rs 580 by Motilal Oswal Financial Services Ltd

Strong express growth and PTL margin expansion strengthen growth outlook

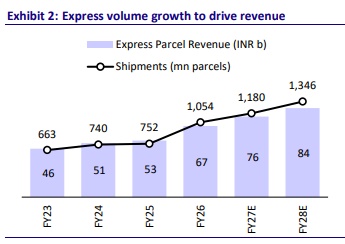

* Delhivery’s Express segment recorded a robust 73% YoY volume growth in 4QFY26 (including the Ecom Express acquisition), despite a challenging operating environment arising from the West Asia crisis and the typical moderation witnessed post the festive-led 3Q season. The strong growth was driven by healthy consumption-led demand, increased outsourcing by customers, and sustained momentum from large e-commerce players. Margins remained robust, driven by strong volumes and tight cost control.

* The PTL business is also witnessing a structural turnaround, with service EBITDA margins expanding sharply from -8.5% in 1QFY24 to 13.4% in 4QFY26. The improvement was driven by a favorable shift in the customer mix toward higheryielding SME and retail customers, rationalization of low-profit contracts, and expansion of the sales team to strengthen customer acquisition and pricing discipline, resulting in yield expansion. Going forward, we expect the company to sustain healthy PTL volume growth and continue gaining market share, supported by its pan-India network, scale advantages, and cost-efficient operations, with growth likely to outpace broader industry trends over the next few years.

* Looking ahead, we estimate the Express segment to clock a 12% revenue CAGR over FY26–28, aided by healthy e-commerce volumes and industry consolidation, whereas margin expansion is likely to be driven by operating leverage and a favorable product mix. The PTL segment offers significant headroom, with organized players handling less than 25% of industry volumes; we project a 17% revenue CAGR over FY25–28, led by SME and retail expansion, yield improvement, and increasing adoption of value-added services. Overall, we expect the company to report a sales/EBITDA/APAT CAGR of 13%/33%/ 83% over FY26-28. We reiterate our BUY rating with a DCF-based TP of INR580.

Strategic inorganic expansion to strengthen market leadership and fuel network advantage

* The INR14b acquisition of Ecom Express (completed in Jul’25) consolidates Delhivery’s leadership in express parcel logistics and adds a complementary rural network, boosting its reach and customer base. This integration is likely to drive network density gains, footprint rationalization, and cost synergies.

* With rural and Tier 2-4 cities forming a major share of e-commerce volumes, the acquisition deepens Delhivery’s competitive moat against peers. The combined entity is well-positioned to gain market share as 3PL players benefit from rising cost pressures on captive logistics arms and industrywide pricing normalization.

* The company remains open to pursuing inorganic growth opportunities, subject to reasonable valuations, as it believes it has the capability to absorb incremental revenues efficiently and scale them at relatively higher margins.

Strong momentum in Express and PTL underpins earnings visibility

* The Express segment continues to witness robust growth, supported by ongoing industry consolidation and rising shipment volumes. Service EBITDA margins are expanding, aided by operating leverage and a favorable low-weight product mix. We project a 12% revenue CAGR in the Express segment over FY26–28, underpinned by strong e-commerce volume growth during the same period.

* The PTL segment remains a fragmented market, with organized players handling less than 25% of the volume. Following the Spoton integration, Delhivery has demonstrated consistent outperformance through wide geographical coverage, faster turnaround times, and tech-driven process optimization. We project a 17% CAGR in PTL revenue over FY26–28, underpinned by SME and retail segment expansion, yield improvement, and the adoption of value-added services.

* The Supply Chain Services (SCS) segment is scaling profitably by exiting unprofitable contracts while benefiting from the increasing formalization of warehousing, GST-led network redesign, and demand for integrated multilocation solutions like the ‘Prime’ service.

Margin expansion inevitable in the core business

* We expect Delhivery’s EBITDA margin to expand to 8.4% in FY28 from 6.1% in FY26, supported by operating leverage, improved asset utilization, and technology integration across the value chain. Management expects PTL’s service EBITDA margin to reach 16–18% over the next 2-3 years (from ~13.4% in 4QFY26), while the express parcel service’s EBITDA margin is likely to be sustained at ~18% (vs. ~18.8% in 4QFY26) or higher due to network optimization.

* Capital intensity has been moderating as the major network buildout nears completion. Steady-state capex is expected to decline to ~4–5% of revenue by FY28. A strong balance sheet with negligible debt offers significant headroom for strategic capex and acquisitions.

Valuation and view

* Delhivery remains well-positioned for future growth, driven by strong momentum in its core transportation businesses and a disciplined focus on profitability. With steady volume growth and healthy service EBITDA margins in both the Express Parcel and PTL segments, the company is well-placed to sustain margin strength going ahead.

* The integration of Ecom Express is set to enhance network efficiency and reduce capital intensity, while new services such as Delhivery Direct and Rapid offer longterm growth potential in on-demand and time-sensitive logistics.

* We expect the company to report a sales/EBITDA/APAT CAGR of 13%/33%/83% over FY26-28. We reiterate our BUY rating with a DCF-based TP of INR580.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412