Buy Bikaji Foods International Ltd for the Target Rs 840 by Motilal Oswal Financial Services Ltd

Double-digit volume growth to continue

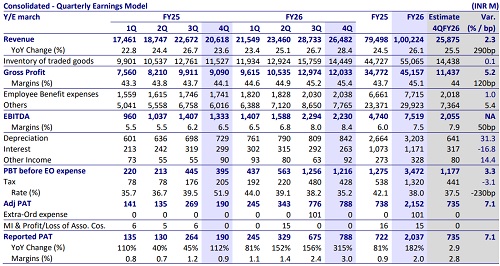

Bikaji Foods International’s (BFL) revenue grew 17.5% to INR7.2b, led by 16.1% YoY volume growth. Its EBITDA/APAT grew 18.1%/ 40.4% YoY. Ethnic Snacks was the fastest growth category with 16.1% YoY growth, followed by Packaged Sweets (+14.4% YoY), Papad (+11.6% YoY), and Western Snacks (+8.6% YoY). Management has taken a ~3% price hike to offset raw material inflation. We expect 15% growth to continue, led by Western Snacks (+30% on a low base), Ethnic Snacks (+13–15%), and Sweets (+11–12%). Total direct coverage stands at 354k outlets; the company added ~42k outlets during FY26 and aims to reach ~500k outlets over the next three years. Management expects focus markets to grow ~18-20%, led by UP, while Delhi continues to remain a relatively weaker market for BFL. The Core market is expected to grow ~12%. The THF business crossed INR1b in revenue during FY26 and is expected to grow at a 50-60% CAGR over the next few years, with an addition of 8-10 stores per year. E-commerce contribution increased from ~2% to ~3% of total revenues with 75-100% YoY growth during FY26

Strong demand recovery led by distribution expansion

BFL reported strong 4QFY26 performance, with 17.5% revenue growth and 16.1% volume growth, driven by improving traction across core markets, successful brand campaigns, and continued distribution expansion. The company witnessed a sharp recovery in demand post-2H, aided by higher advertising spends, Bhujia-focused campaigns, and strong growth in family packs, which grew ~20% during the quarter. Core geographies accelerated to over 15% growth, while focus markets such as Uttar Pradesh delivered robust traction, supported by localized marketing initiatives. Management highlighted that the Ethnic Snacks category continues to remain the key growth driver, while the Western Snacks category is expected to return to a 20%+ growth trajectory despite temporary softness in 4Q.

Operating margin (ex-PLI) to reach 14% by FY28

Gross margin remained resilient despite sharp inflation in edible oil and packaging materials, as margins expanded 210bp YoY to 35.6%. EBITDA stood at INR877m (+18.1% YoY), recording an EBITDA margin of 12.2% (+6bp YoY). Excluding PLI, operating margin stood at 10.4% (40bp lower QoQ) due to higher A&P spends. BFL implemented ~3% price hikes along with selective grammage reductions to offset inflationary pressures. Gross margins remained stable despite higher inflation and management expects operating margins to expand ~60-80bp, supported by operating leverage and manufacturing efficiencies.

Valuation and view: Reiterate BUY

We expect BFL to benefit from accelerating demand for branded snacks, shifting consumer preferences, and increasing traction within modern trade and ecommerce channels. The company is set to deliver industry-leading growth, with revenue, EBITDA (ex PLI), and PAT (ex PLI) CAGRs of 15%, 24%, and 32% over FY26-28. We trim our earnings and reiterate our BUY rating with a DCF-based TP of INR840 (based on an implied P/E of 55x on FY28E). Key risks: geographical concentration on core markets and the potential entry of new competitors in Rajasthan.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

2.jpg)