Bulls & Bears : India Valuations Handbook By Motilal Oswal Financial Services Ltd

Strategy: Nifty bids adieu to CY24 with 9% returns; DII inflows at record high

* Record-breaking year for Nifty: CY24 concluded with yet another year of positive returns for the Indian markets, marking nine consecutive years of growth! The last three years have been remarkable, as domestic markets have navigated through global hurdles, all while facing significant selling from FIIs. During the last 12 months, midcaps and smallcaps both have gained 24% and outperformed largecaps, which have risen 9%. During the last five years, midcaps have significantly outperformed largecaps by 140%, while smallcaps have outperformed largecaps by 128%.

* DII inflows vs. FII outflows – the persisting tug of war: DII flows into equities were the highest ever at USD62.9b in CY24 vs. inflows of USD22.3b in CY23. With just one year of outflows since CY15, DIIs have invested USD175.9b cumulatively over the last 10 years (CY15-CY24). Conversely, FIIs witnessed equity outflows of USD0.8b in CY24 vs. inflows of USD21.4b in CY23. During the last 10 years, FIIs have invested USD54.4b cumulatively in the Indian market, with only three years of outflows.

* All major sectors deliver positive returns in CY24: Among the sectors, the top gainers were Healthcare (+39%), Real Estate (+34%), Telecom (+26%), Automobiles (+23%), and Technology (+22%). The breadth was favorable in CY24, with 32 Nifty stocks closing higher. Trent (+133%), M&M (+74%), Bharat Electronics (+59%), Bharti Airtel (+54%), and Sun Pharma (+50%) are the top performers, while IndusInd Bank (-40%), Asian Paints (-33%), Nestle (-18%), Tata Consumer (-15%), and HUL (-13%) are the top laggards.

* India among the laggards in Dec’24: Among the key global markets, Russia (+15%), Japan (+4%), Taiwan (+3%), and China (+1%) ended higher in local currency terms. However, Brazil (-4%), the US (-2%), Korea (-2%), India (- 2%), the UK (-1%) ended lower MoM in Dec’24. Over the last 12 months, the MSCI India Index (+14%) has outperformed the MSCI EM Index (+5%). Over the last 10 years, the MSCI India Index has outperformed the MSCI EM index by a robust 168%. Over the last 12 months, global market cap increased 10.9% (USD12.2t), whereas India’s market cap surged 23.6%. Barring Brazil, Korea, the UK, and Indonesia, all key global markets have seen a rise in market cap over the last 12 months.

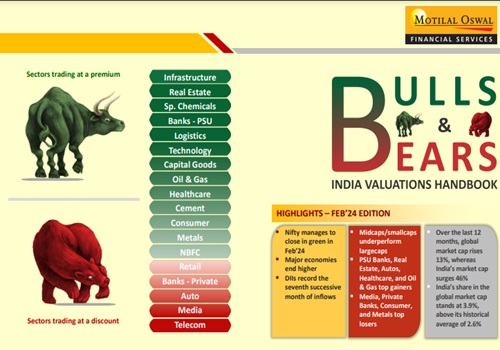

* Valuations – two-thirds of the sectors trade at a premium to their historical averages: Following the recent correction, the Nifty now trades at a 12-month forward P/E of 19.9x, near its LPA of 20.5x (3% discount). Conversely, the P/B ratio at 3.2x represents a 12% premium to its historical average of 2.8x. The market capitalization-to-GDP ratio is at a year-end high of 138% (we expect nominal GDP to grow 9.2% YoY in FY25). Consumer, Retail, and NBFCs now trade within a reasonable range of their long-period average (LPA) valuations, while Real Estate, Technology, and Healthcare – after their sharp run up – trade at 49%/34%/25% premium to their LPA. PSU Banks are trading at a 33% premium to their LPA on a P/B basis.

* Back to the Future – CY25: The past year experienced a slowdown in earnings and consumption, rising global interest rates, geopolitical uncertainties, and high valuations in some mid- and small-cap sectors. CY25 may alleviate some concerns, with a gradual recovery in corporate earnings and consumption expected due to increased government spending in early CY25 and improved rural incomes after a successful kharif season. However, there may be some volatility in global trade and currencies after the new US administration takes charge, and persistent inflation could slow anticipated interest rate cuts. Our model portfolio reflects our conviction in domestic structural as well as cyclical themes. We are OW on IT, Healthcare, BFSI, Consumer Discretionary, Industrials, and Real Estate. On the other hand, we are UW on Metals, Energy, and Automobiles.

* Top ideas: Largecaps – HDFC Bank, SBI, L&T, HCL Tech, M&M, Zomato, Bharti Airtel, Titan Company, Mankind Pharma, and Dixon Technologies; Midcaps and Smallcaps – Indian Hotels, Cummins India, Kaynes Technology, BSE, Godrej Properties, Coforge, Metro Brands, IPCA Laboratories, Angel One, and JSW Infrastructure.

For More Motilal Oswal Securities Ltd Disclaimer http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412