Bulls and Bears : Pain continues; the steepest MoM dip since Mar`20 by Motilal Oswal Financial Services Ltd

* Market slumps for the fourth consecutive month: The Nifty slid 11.3% MoM in Mar’26 – the fourth consecutive month of a decline amid geopolitical tensions in the Middle East. The index oscillated 2,706 points before closing at 2,847 points (or 11.3% MoM) lower at 22,331 – the steepest MoM decline since Mar’20. The Nifty is down 14.5% in CY26YTD. Over the last 12 months, largecaps and smallcaps have been down 5% and 6% YoY, respectively, underperforming midcaps, which have risen 2% YoY. Over the last five years, midcaps (CAGR: 17.3%) have notably outperformed largecaps (CAGR: 8.7%) by 70%, while smallcaps (CAGR: 13.4%) have markedly outperformed largecaps by 35%.

* FII outflows and DII inflows at record highs in Mar’26: Notably, DII inflows (at USD15.4b) and FII outflows (at USD13.3b) were at record highs in Mar’26. FII outflows into Indian equities stand at USD14.9b in CY26YTD. DII inflows into equities continue to be strong at USD27.2b in CY26YTD.

* Breath adverse in Mar’26: All major sectors ended lower – PSU Banks (-20%), Real Estate (-17%), Private Banks (-16%), Automobiles (-16%), and Financials (-14%) were the top laggards, MoM. The breadth was adverse in Mar’26, with 46 Nifty stocks closing lower. Coal India (+5%), Tech Mahindra (+2%), ONGC (+2%), and Sun Pharma (+1%) were the only gainers, while Tata Motors PV (-23%), Bajaj Finance (-20%), Shriram Finance (-19%), Adani Enterprises (-19%), and SBI (-18%) were the top laggards.

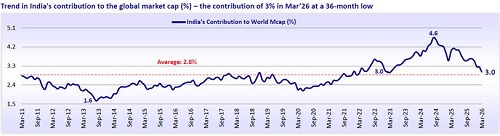

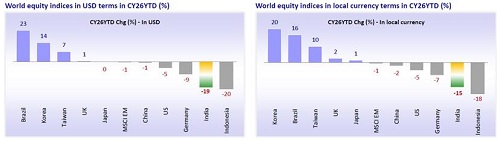

* Major economies end lower in Mar’26: Among the key global markets, Korea (-19%), Indonesia (-14%), MSCI EM (-13%), Japan (-13%), India (-11%), Taiwan (-10%), Germany (-10%), the UK (-7%), China (-7%), the US (-5%), and Brazil (-1%) ended lower MoM. During the last 12 months in USD terms, the MSCI India Index (-13%) underperformed the MSCI EM Index (+27%). Over the last 10 years, the MSCI India Index notably outperformed the MSCI EM Index by 27%. In P/E terms, the MSCI India Index is trading at a 27% premium to the MSCI EM Index, below its historical average premium of 73%.

* The Nifty-50 valuation slips below its historical average; two-thirds of the sectors trade at a discount: The Nifty is trading at a 12-month forward P/E ratio of 17.7x, below its LPA of 20.9x (at a 15% discount). Also, its P/B of 2.6x represents a 8% discount to its historical average of 2.9x.The 12-month trailing P/E for the Nifty, at 20.7x, is below its LPA of 23.2x (at a 11% discount). At 3x, the 12-month trailing P/B ratio for the Nifty is below its historical average of 3.2x (at a 6% discount). India’s market cap-to - GDP ratio has been volatile, plummeting to 57% (of FY20 GDP) in Mar’20 from 80% in FY19 and then sharply rebounding to 132% in FY24 and 126% in FY25. It now stands at 115% of FY26E GDP (9% YoY), well above its long-term average of 87%. Capital Goods, PSU Banks, Metals, Healthcare, and Utilities trade at a premium to their long-period average (LPA) valuations, while Private Banks, Consumer, Technology, Retail, and Automobiles trade at a discount to their LPA.

* View: The ongoing Iran-Israel conflict has escalated beyond a regional dispute due to the closure of the Strait of Hormuz. This development has triggered a sharp correction in Indian equities, as a significant portion of India’s oil and gas imports transit through Hormuz. Concurrently, the Indian rupee has experienced a once-in-a-decade depreciation, complicating India’s external accounts, growth prospects, and inflation expectations. While the US faces immense internal pressure to avoid further escalation, the situation remains highly fluid, necessitating careful and selective stock picking, as a swift resolution could trigger pent-up buying and short-covering. The Nifty-50 and Midcap-100 have corrected ~11%, with sectors such as Banking, Automobiles, Real Estate, and Consumer Goods bearing the brunt due to higher risk aversion, panic-driven selling, and rising oil prices. Although markets typically recover over the long term, current structural disruptions to supply chains and inflation concerns are raising fears of prolonged market instability and delayed monetary easing. The Nifty-50 is trading at a 12 - month forward P/E of 17.7x, below its LPA of 20.9x (at a 15% discount). Further, its P/B of 2.6x represents an 8% discount to its historical average of 2.9x. Given these relative valuations, we find greater value in largecaps vs. midcaps. We are OW on Auto, PSU Banks, Diversified Financials, Technology, Consumer Discretionary, and Capital Goods + EMS, which are our key preferred investment themes. We are Neutral on Telecom, Cement, and Healthcare, while retaining our UW stance on Private Banks, Consumer Staples, O&G, Utilities, and Metals within our model portfolio.

* Top Nifty-50 Ideas: Bharti Airtel, SBI, ICICI Bank, Lenskart, M&M, Titan, Bharat Electronics, Eternal, Tata Steel, Infosys, and Interglobe Aviation. Top Non-Nifty-50 Ideas: TVS Motors, Groww, Indian Hotels, AU Small Finance, Dixon Tech, Premier Energies, Coforge, Radico Khaitan, Delhivery, and ACME Solar.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

.jpg)

Morning Glance 9th June 2026 - ARETE Securities Ltd

.jpg)