Asia stocks take a breather for earnings, rate calls

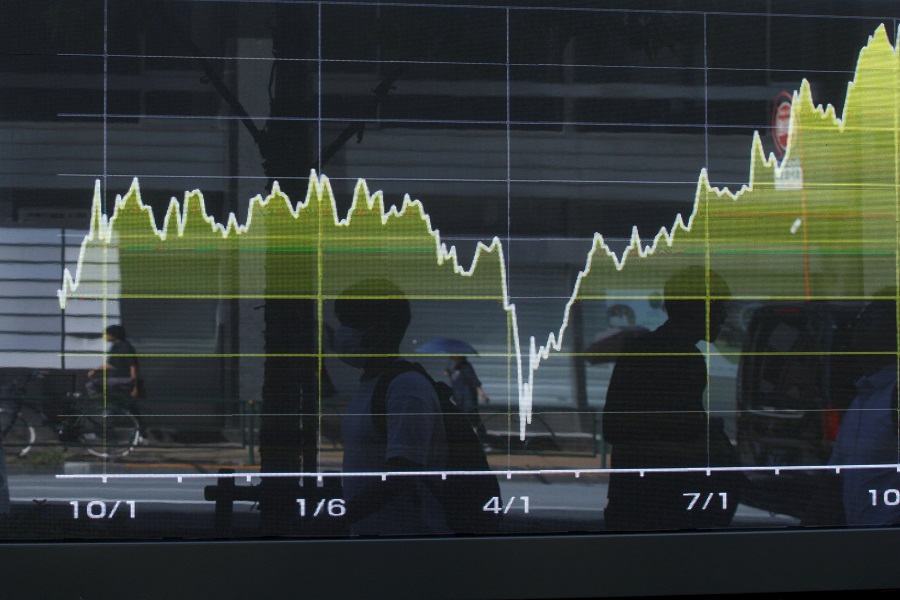

Asian shares consolidated recent hefty gains on Tuesday as hopes for an easing in global trade tensions kept risk appetites keen, while the bull run in tech stocks counted on a bumper round of big-cap earnings this week.

The likelihood of lower borrowing costs in the United States and Canada this week supported bonds, while the dollar paused to see just how dovish the Federal Reserve might be on the outlook.

Meanwhile, safe-haven gold huddled around $4,000 an ounce, as a drop of 9% in five sessions squeezed leveraged money out of a very crowded trade. [GOL/]

"What began as a price rise supported by fundamentals now looks driven by retail enthusiasm," said Neil Shearing, group chief economist at Capital Economics.

"And with prices still at record highs in real terms, the next big move in gold is more likely to be down than up," he added. "Indeed, our new forecast is that the price will fall to $3,500/oz by the end of 2026."

Several Asian share markets have also hit all-time highs and were overdue a breather. The Nikkei eased 0.2%, having surged 2.5% on Monday as a rally in all things tech lifted it to gains of almost 27% so far this year.

Japan's new Prime Minister Sanae Takaichi met U.S. President Donald Trump in Tokyo to discuss defence ties, trade and a package of U.S. investments in a $550 billion deal struck earlier this year.

South Korean stocks slipped 1.4%, giving back just some of Monday's 2.6% jump. Sentiment was aided by data showing the economy outpaced forecasts in the third quarter, led by strength in consumption and exports.

MSCI's broadest index of Asia-Pacific shares outside Japan edged down 0.1%, while Chinese blue chips were little changed.

EUROSTOXX 50 futures and DAX futures held steady, as did S&P 500 futures and Nasdaq futures.

Tech stocks had again led Wall Street higher overnight, with Qualcomm jumping 11% after it unveiled two artificial intelligence chips for data centres.

AN END TO QT?

There are lofty expectations for the "Magnificent Seven" tech heavyweights reporting this week, with Microsoft, Alphabet, Apple, Amazon and Meta Platforms all needing strong results to justify stretched valuations.

Aiming to curb expenses, Amazon is planning to cut as many as 30,000 corporate jobs starting on Tuesday, sources told Reuters.

In bond markets, 10-year Treasury yields held at 3.98% as investors wait on Wednesday's Fed meeting. A quarter-point rate cut is considered a done deal, with the real focus on whether the Fed validates market pricing for a December easing as well.

There are also hopes the Fed will end the rundown of its balance sheet, otherwise known as quantitative tightening.

Canada's central bank is also expected to cut rates this week, while the European Central Bank and the Bank of Japan are seen holding steady.

The BOJ is likely to debate whether conditions are right to resume rate hikes as worries about a tariff-induced recession ease, but political complications may keep it on hold for now.

Wagers on a dovish Fed outlook kept the dollar restrained at 152.35 yen, having stopped short of the recent 153.29 peak overnight.

The euro nudged up to $1.1659, but remains short of resistance at $1.1728. The dollar index eased 0.1% to 98.666, but remained well within the recent trading range.

In commodity markets, oil prices slipped on a Reuters report that eight OPEC+ nations are leaning towards making another modest increase in oil output for December when they meet on Sunday, as Saudi Arabia pushes to reclaim market share. [O/R]

Brent dropped 0.2% to $65.46 a barrel, while U.S. crude eased 0.2% to $61.17 per barrel.