April 2026: Reversals, Resilience & Remaining Cracks: Vallum Capital

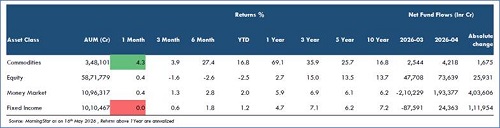

According to Vallum Capital’s Monthly Macro Grid Chartbook report, across asset classes, April’s defining story was a broad reversal. Equity attracted Rs 73,639 Cr, up Rs 25,931 Cr versus March, while Money Market and Fixed Income both snapped out of heavy outflows, painting a picture of normalisation after March’s quarter-end disruption.

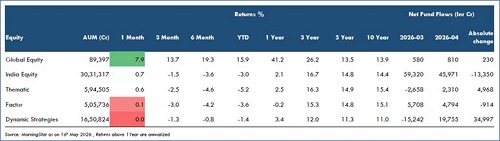

Equity: Flows Up, but Selectivity Rising

Within equity, Dynamic Strategies delivered the month’s most dramatic shift, recording a Rs 34,997 Cr swing from Rs15,242 Cr outflows to Rs19,755 Cr inflows. This made it the largest monthly reversal across all equity sub-categories. The engine behind it was Arbitrage Funds, which alone accounted for Rs33,173 Cr of that swing as institutional positioning unwound.

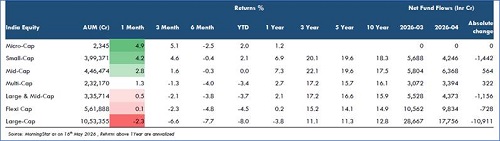

Large-Cap fund inflows moderated to Rs17,756 Cr, down Rs10,911 Cr from the previous period. However, it remains the dominant destination despite posting -8.0% YTD, the weakest performance across segments. Investors are systematically SIPing into underperformance rather than rotating away, a hallmark of India’s maturing SIP culture.

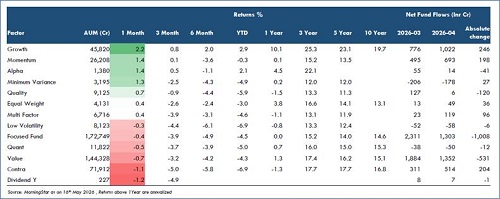

In the Factor space, Growth stood out as the only factor delivering on both fronts, with +2.2% in April and +2.9% YTD, alongside rising inflows of Rs1,022 Cr. Focused Funds, meanwhile, saw the steepest flow decline at -Rs1,008 Cr, reflecting fading confidence in concentrated bets amid a volatile market.

Thematic: Sharp Divergences

PSU executed the single biggest thematic turnaround, moving from Rs4,497 Cr outflows to Rs489 Cr inflows, a Rs4,986 Cr swing.

BFSI reinforced this divergence. Broad BFSI underperformed across themes yet attracted massive net flows, both within the BFSI pack and the wider thematic universe. Within BFSI, Capital Markets led performance with 18.1% YTD and 7.4% in one month, supported by growing investor interest.

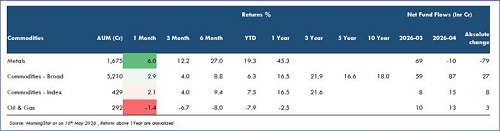

On commodities, Metals led with 19.3% YTD and +6.0% in April. Healthcare held strong across sub-categories, although Pharma’s 8.8% April return was offset by Rs 62 Cr net outflows.

Technology remains the chartbook’s deepest wound. The IT Index is down -26.3% YTD and -11.9% in April, with only Digital India attracting any dip-buying at Rs42 Cr.

Global & Forex

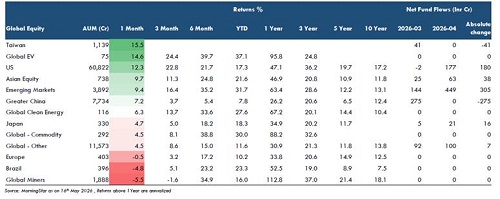

Country allocation leadership is concentrated in South Korea, Taiwan and broader ex-China exposure, while India remains a short-term laggard despite improving global breadth.

Global thematic leadership is decisively growth-oriented, with semiconductors, software, robotics, quantum computing and electrification outperforming, while global defence momentum has recently cooled.

INR weakness across most major and Asian currencies reinforces a global risk-on, Asia-led positioning backdrop, but also raises imported inflation and external vulnerability risks.

April corrected March’s distortions but revealed where real conviction sits: SIP-driven Large-Cap allocations, PSU/BFSI value-hunting, and a structural retreat from Technology. Until broader equity turns YTD-positive, Indian capital remains disciplined, not bold.

Above views are of the author and not of the website kindly read disclaimer

.jpg)