Add Bajaj Consumer Care Ltd For Target Rs.715 by Choice Institutional Equities Ltd

Growth Momentum Continues

Q1FY27 results were ahead of expectation; while revenue came in line with estimate, led by continued strong momentum in ADHO (Almond Drop Hair Oil) portfolio (volume growth est. 11-12%) driven by strong growth in sachets. EBITDA margin was ahead of expectation on the strength of better gross margin expansion (price hike), cost savings to the tune of 600 bps YoY and operating leverage

Key Management Guidance:

Q2FY27 gross margin is expected to remain under pressure as compared to Q1 on account of higher raw material cost. However, Q3 and Q4 is expected to see recovery as recent raw material price trend saw a decline. Moreover, the current EBITDA margin of 24.4% is on the upper end of guided range; while long-term EBITDA margin guidance is expected to be in low to mid 20s range.

Valuation & Rating:

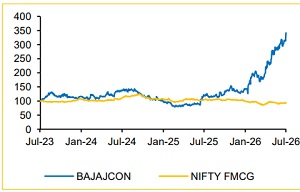

We remain constructive on Bajaj Consumer Care’s longterm growth strategy, driven by the recovery in ADHO, scaling up of the nonADHO growth portfolio, premiumisation and Project Aarohan-led distribution expansion. Sustained double-digit growth, an improving product mix and operating leverage are expected to drive Revenue/EBITDA/PAT CAGR of 14%/20%/20%, respectively, over FY26–29E. We have revised our one-year DCF-based TP to INR 715 (earlier: INR 690), implying an upside of 9% from the CMP (implied P/E of ~32.4x FY28E EPS and PEG of 2.3). Given the sharp appreciation in the stock price, up ~88% since April 2026 (~25% since our Initiating Coverage) and the limited upside from the current level, we have changed our rating on the stock from BUY to ‘ADD.’

Q1FY27 Result: ADHO Continues to Drive Growth

* Revenue was up 24.9% YoY and up 4.6% QoQ to INR 3,416 Mn (vs. CIE estimate of INR 3,402 Mn). Q1FY27 ADHO volume grew in early teens (est. 11-12%) led primarily by sachets.

* EBITDA was up 103.1% YoY and up 8.9% QoQ to INR 834 Mn (vs. CIE estimate of INR 743 Mn). EBITDA margin was up 939 bps YoY and up 98 bps QoQ to 24.4% (vs. CIE estimate of 21.8%). BAJAJCON under took price hikes and grammage cut on back of increase in raw material prices. Its cost-saving program and operating leverage supported overall EBITDA growth.

* PAT was up 84.9% YoY and up 11.1% QoQ to INR 707 Mn (vs. CIE estimate of INR 620 Mn)

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131