IT Sector Update : Infosys and Wipro preview: No change in relative positioning despite worsening macros - ICICI Securities

Follow us Now on Telegram ! Get daily 10 - 12 important updates on Business, Finance and Investment. Join our Telegram Channel

https://t.me/InvestmentGuruIndiacom

Download Telegram App before Joining the Channel

Infosys (Infy) Q4FY23 preview: High quality company with ability to gain market share in current environment; upgrade to BUY (from Add) on attractive valuations.

* Demand and margin outlook as per Infy: Macro situation has worsened in Q4FY23 vs Q3FY23, but this has not translated to client cutting spending on existing projects. Already signed deals are progressing as per plan, and therefore, there is no delay in conversion of orderbook to revenue. However, there is more scrutiny in new deal signings especially in discretionary spending. Q4FY23 deal wins as well as current deal pipeline has higher share of cost optimisation, efficiency gain and vendor consolidation deals vs digital transformation deals. Infy’s exposure to regional banks is not material; however, due to the ongoing uncertainty in the US and European banking industry, we expect moderation in BFSI revenue growth in the near term. The company had called out softness in mortgage, home lending, investment banking, retail and technology verticals in Q3FY23 and the same has continued in Q4FY23. Additionally, the company is seeing softness in telecom vertical as 5G spends are coming under higher scrutiny in certain client pockets.

* Margin headwinds in Q4FY23 are visa costs and lower working days, whereas improving sub- con costs, utilisation will be key tailwinds. Pricing improvement is not a big tailwind as per the company. Attrition is closer to desired levels and supply-side pressures are easing off.

* Infosys has witnessed the exit of two key presidents (Mr. Mohit Joshi and Mr. Ravi Kumar) in the last six months. Transition after Ravi Kumar’s exit in Oct 22 has been smooth. The company has a large bench of ~30-35 EVPs to take over top leadership roles as and when required and does not expect significant disruption due to leadership change.

* Our Q4FY23 estimates for INFY: We expect INFY’s revenue growth to be soft at 0.1% QoQ CC, given Q4FY23 is a seasonally weak quarter for INFY. This translates to 16.4%YoY CC growth in FY23E within the company’s guided range of 16-16.5%. We estimate 110bps cross-currency tailwinds in Q4FY23. We model 21.5% EBIT margin, flat QoQ in Q4FY23 and 21.2% in FY23, in line with management commentary of achieving margins near the lower end of guidance of 21 22%. Large deal wins were strong in Q3FY23 atUS$3.3 bn (20% QoQ, 31% YoY), partly aided by the closure of a bunch of license deals. Pipeline is replenished, but we expect deal TCV in the range of US$2.5-3bn, decline on QoQ basis. We expect INFY to start the year with conservative guidance of 6-8% given the recent events in global banking industry (BFSI accounts to 32% of INFY’s annual revenue) and overall caution in new deal singings.

* Change in estimates: We have cut INFY’s FY24 US$ revenue estimate by 1.2% and assume 7.4% YoY CC growth in FY24 on slower tech spending in BFSI vertical and its follow-on effect on other verticals. We see right shifting of demand to FY25 with no change in US$ revenue assumption for FY25 and FY26 and thus, higher revenue growth assumption of 12.7%/13.8% YoY CC in FY25E/FY26E. We cut EBIT margin estimates by ~40bps in FY24 due to lower leverage from revenue growth and largely maintain FY25/26 margin estimates. As a result, our EPS estimates are cut by 3%/1%/0.7% for FY24/25/26, respectively.

* Upgrade INFY to BUY: We continue to value INFY at 23x FY26E EPS of Rs86 (discounted back 1-year with WACC of 12%) to arrive at our 12-month target price of Rs1,759 (earlier: 1,772), implying 28% potential upside. The stock has corrected ~7% in the last one month and is trading at an attractive valuation of 19x/16x on FY25/26 EPS. We upgrade INFY to BUY (earlier: Add) on attractive valuations. Given INFY’s strong digital capability and management execution with focus on winning large deals amid vendor consolidation, we expect INFY to be the fastest growing large-cap IT services company globally.

To Read Complete Report & Disclaimer Click Here

https://secure.icicidirect.com/Content/StaticData/Disclaimer.html

Above views are of the author and not of the website kindly read disclaimer

More News

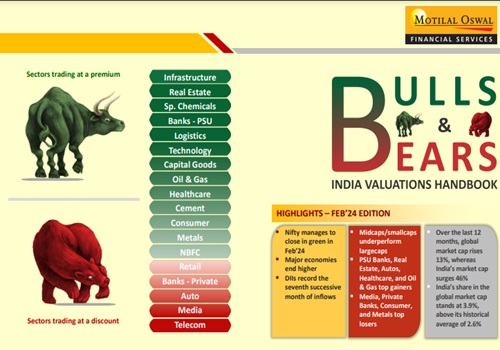

Bulls & Bears : India Valuations Handbook By Motilal Oswal Financial Services Ltd