Bulls & Bears : India Valuations Handbook By Motilal Oswal Financial Services Ltd

Strategy: Gaining momentum; largecaps outperform midcaps/smallcaps

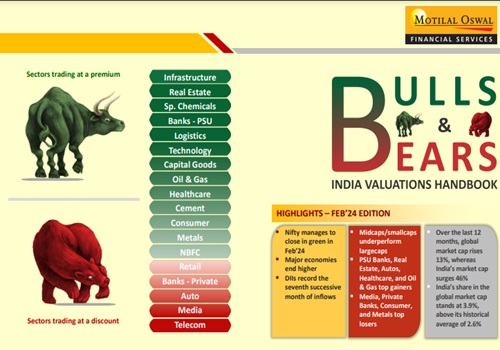

* Market sees elevated volatility; manages to close in green:

The Nifty managed to close in green (up 1.2% MoM) in Feb’24 after consolidating in Jan’24. Notably, the index was extremely volatile and swung around 767 points before closing 257 points higher. During the last 12 months, midcaps and smallcaps have gained 60% and 74%, respectively, while largecaps have risen 27%. During the last five years, midcaps have outperformed largecaps by 85%, while smallcaps have outperformed largecaps by 65%.

* FII flows muted, but DII flows continue to be healthy:

In Feb’24, FIIs posted the muted inflows at USD0.5b. DIIs recorded the seventh consecutive month of inflows at USD3.1b. FII outflows into Indian equities stood at USD2.7b in CY24YTD vs. inflows of USD21.4b in CY23. DII inflows into equities in CY24YTD continue to be strong at USD6.3b vs. USD22.3b in CY23.

* Major sector end higher, breadth favorable in Feb’24:

Among the sectors, PSU Banks (+10%), Real Estate (+6%), Automobiles (+6%), Healthcare (+6%), and Oil & Gas (+6%) were the top gainers. While, Media (-5%), Private Banks (-2%), Consumer (-2%), and Metals (-1%) were the key laggards. BPCL (+20%), M&M (+17%), SBI (+17%), Sun Pharma (+11%), and Maruti Suzuki (+11%) were the top performers among the stocks, while Hindalco (- 13%), UPL (-13%), ITC (-8%), Kotak Mahindra Bank (-7%), and Bajaj Finance (-5%) were the key laggards.

* Major economies end higher in Feb’24: Barring the UK (flat MoM), Feb’24 saw key global markets such as China (+8%), Japan (+8%), Taiwan (+6%), Korea (+6%), the US (+5%), MSCI EM (+5%), Russia (+2%), Indonesia (+2%), India (+1%), and Brazil (+1%) close higher in local currency terms. Over the last 12 months, the MSCI India Index (+36%) has outperformed the MSCI EM Index (+6%). Over the last 10 years, the MSCI India Index has notably outperformed the MSCI EM index by 214%.

* Earnings review – 3QFY24: Earnings beyond expectations!:

The 3QFY24 corporate earnings ended on a strong note, with widespread outperformance across aggregates driven by continued margin tailwinds. Domestic cyclicals such as Autos and Financials, along with global cyclicals (i.e., Metals and O&G) drove the beat. Technology posted a marginal decline in earnings, its first in 26 quarters. The aggregate earnings of the MOFSL Universe companies exceeded our expectations and rose 29% YoY (vs. our est. of +19%). Earnings for the Nifty50 jumped 17% YoY (vs. our est. of +11%).

* Real GDP growth crosses 8% for the third successive quarter in 3QFY24:

Real GDP growth came in much higher than expected at 8.4% in 3QFY24 vs. 8.1% (revised higher from 7.6%) in 2QFY24 and 4.3% in 3QFY23 (revised lower from 4.8%). 1QFY24 GDP growth has also been revised higher to 8.2% from 7.8%. Consequently, GDP growth for 9MFY24 stood at 8.2%. Higher-than-expected GDP growth was partly led by a downward revision in 3QFY23 growth (to 4.3% from 4.8% earlier) and a very high growth in real net indirect taxes, driven by lower subsidies.

* Our view: India is currently enjoying the confluence of the best macro and micro tailwinds with ~7% GDP growth, moderating inflation prints, range-bound crude prices, easing 10-year G-sec yield, stable currency, and resilient corporate earnings. Nifty is trading at a 12-month forward P/E ratio of 19.5x, which is in line with its long-period average (LPA) even as broader markets trade at expensive valuations (the NSE Midcap 100 index is trading at ~33% premium to Nifty). We prefer PSU Banks, Industrials (Capital Goods and Cement), Real Estate, Consumer Discretionary, and NBFCs, while we are UW on IT and Metals. We recently upgraded Energy to Neutral and downgraded Autos and Pharma to Neutral in our model portfolio. Markets, in the near term, will take cues from: 1) the outcome of the Lok Sabha elections scheduled in Apr/May’24, and 2) the timing and quantum of easing in the interest rate cycle, both globally and in India.

* Top ideas: Largecaps – L&T, SBI, ICICI Bank, Coal India, Titan, M&M, GAIL, ITC, HCL Tech, Cipla, Zomato; Midcaps and Smallcaps – Indian Hotels, Godrej Properties, Sobha Developers, Dalmia Bharat, Angel One, IIFL Finance, Cello World, PNB Housing, Lemon Tree, and Restaurant Brands Asia.

For More Motilal Oswal Securities Ltd Disclaimer http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Tag News

Cement Sector Update : Weak print, yet gradual recovery aligns with expectations by Motilal ...

More News

BFSI - Banks Sector Update : Interested, but waiting on the edge By JM Financial Services