Monthly Equity Views by Sorbh Gupta, Quantum Mutual Fund

Below are Views On Monthly Equity Views by Sorbh Gupta- Quantum Mutual Fund

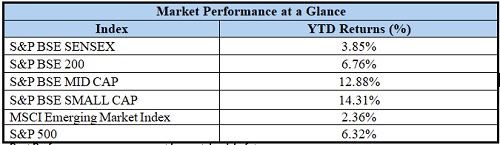

S&P BSE Sensex appreciated by 0.85% on a total return basis in the month of March 2021. On trailing twelve month (TTM) basis the index has returned 69.82%. A favourable base of March 2020 is getting reflected in the TTM return. S&P BSE Sensex performance was worse than developed market indices such as S&P 500& Dow Jones Industrial Average which appreciated by3.34% & 5.71% respectively, during the month. However, the Sensex has outperformed the MSCI Emerging Market Index which fell by -2.48%.

The broader market has done better than the Sensex in the month of March 2021. TheS&P BSE Midcap Index appreciated by 1.20% and the S&P BSE Small-cap Index rose by 2.48%.Technology, Consumer Staples & Metals were the winning sectors for the month. The technology stocks have rallied taking cues from good results of some global technology stocks. Metal have reacted positively to the up move in global commodity prices. Banking & Real Estatestocks underperformed during the month, as resurgence of Covid-19 made investors nervous about its impact on near term business prospects.

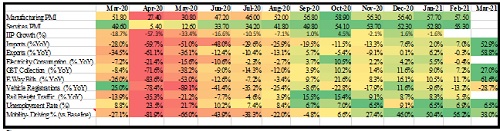

Economic Recovery is flattening: The economic indicators continue to reflect improving economic recovery. However, some of the data indicates flattening of m-o-m recovery momentum of late. The index of industrial production (IIP) has averaged just ~0.6% YoY in past five months. Most of the macro data points & corporate earnings will look attractive from a y-o-y basis for the next few months (starting from March 2021) as the base gets favourable (last March-April was a period of strict nation-wide lockdown).

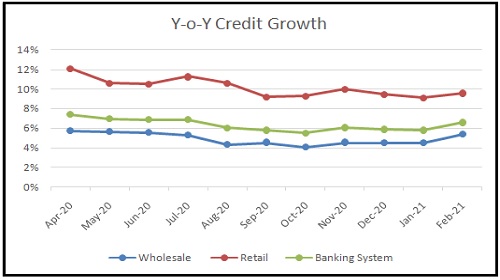

Credit growth pick up is gradual:The mid-march banking data indicates credit growth is recovering but the pick-up is gradual (6.5% YoY growth). The sectoral data indicates, credit growth is being driven by retail while the corporate loan books are flat on y-o-y basis. This clearly means the private corporate capex cycle is yet to pick up (it remains the key for a sustainable economic recovery).

Flows: Inflows have continued in the New Year.

Indian Equities have seen $ 2.3bn of net buying by foreign investors in the month of March 2021. One an YTD basis FPI inflows stand at US$ 7.4 bn. This is on the back of US$ 23 bn of FII flows in CY2020.DIIs have turned buyers in the month of March 2021, after four months of being sellers. They have bought stocks worth US$ 205 mn this month. Indian rupee appreciated by 0.49% during the month.India’s nominalGDP growth trajectory is improving and will look better than the western world in the medium term. This makes it a sought after destination for yield & growth seeking developed world investors. This means strong FII inflows can continue.

Covid 19: Resurgence risk more apparent now. Universal immunization still some time away

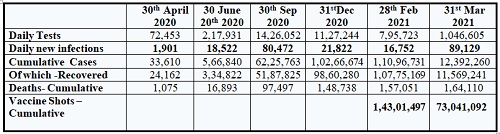

The resurgence in Covid-19 cases in March poses a challenge.The state of Maharashtra is worst effected and there has been instances of weekly lockdowns & night curfews in some towns. But till now local governments have not imposed a strict lockdown akin to March-April 2020. As of Mar 27, 0.65% of population has been fully vaccinated and 3.13% of population has taken the first dose. At the current daily run rate of 2.2 mn, India would take close to three years in achieving universal immunisation. The government has set a stiff target of vaccinating 300 mn (22% of population) by August.

Quantum Long Term Equity Value Fund saw a 1.67% appreciation in its NAV in the month ofMarch 2021. This compares to a1.29% appreciation in its benchmark S&P BSE 200. Outperformance for the month was driven by holdings in IT, Materials & Metals. Cash in the scheme stood at approximately 6% at the end of March.

The two near term macro risks we have been highlighting in our previous newsletters; Covid-19 resurgence & inflation, have come to the fore. Equity markets are clearly not factoring the further worsening of both these factors. The government’s fiscal expansion driven spending is focussed on capital expenditure rather than consumption boost and will not lend a helping hand to soften the near term macro headwinds. We remain constructive on Indian equities with longer-term view & recommend investors to use the near term corrections as buying opportunity to create a long term equity exposure.

Above views are of the author and not of the website kindly read disclaimer