The Eagle Eye : Geopolitical easing strengthens India’s market stability – Motilal Oswal Financial Services Ltd

‘Big Tech’ stocks and tech-heavy markets overshadow India and other key EMs in both size and growth

* The AI-led rally has dramatically reshaped global market cap rankings. In USD terms, Big Tech companies such as NVIDIA, Alphabet, and Apple have grown to match and, in some cases, exceed the entire listed market cap of India and several other countries, despite being significantly smaller than these markets just a few years ago.

* This highlights the extraordinary scale and growth of AI and Big Tech players. Capital, earnings, and investor flows are becoming increasingly concentrated in a handful of technology leaders, raising market concentration risks even as the AI theme continues to drive global equity market performance

AI reshapes Indian IT: Breaking point or turning point

* The ongoing AI-driven disruption is likely to exert pressure on the existing revenue streams of Indian IT services companies, as automation and productivity gains may lead to deal-related revenue deflation.

* However, management commentary suggests that AI is significantly expanding the addressable market by creating new technology spending opportunities. In addition, the absence of large legacy managed-services commitments in AI-based opportunities positions Indian IT firms well to capture new business, drive market-share gains, and support long-term revenue growth.

Our take:

* While ~15–20% of IT services revenue may face AI-led productivity and automation pressures, the impact is likely to be inherently prone to error and risk oversimplifying a far more dynamic transition.

* The key differentiator will be the ability of incumbent IT firms to replicate, scale, and commercialize AI-native delivery models faster than peers.

* The sector is likely heading toward a business model reset, with AI capabilities and strategic M&A emerging as critical determinants of market share gains over the next 24–36 months.

Strong AI demand to sustain elevated memory pricing

* Memory prices have surged sharply, with DRAM contract prices rising over 4x and NAND flash spot prices ~7x since Sep’25, driven by tight supply and robust AI-led demand.

* AI infrastructure expansion is accelerating demand for High Bandwidth Memory (HBM), prompting leading memory manufacturers such as Samsung, SK Hynix, and Micron to reallocate production capacity from conventional memory (DDR, LPDDR, etc.) to HBM, further tightening supply.

* Although capacity expansions are underway, demand from AI data centers, agentic AI applications, and server deployments is expected to outpace incremental supply, keeping the market structurally undersupplied.

* Memory prices are therefore expected to remain elevated over the medium term, as AI-driven demand continues to exceed industry capacity additions, supporting a sustained tight supply environment.

INR rebounds as global risks ebb

* After experiencing its weakest performance in over a decade and coming under pressure earlier this month amid heightened geopolitical tensions and a sharp rise in crude oil prices, the INR, along with several global currencies, has recovered from its Jun’26 low of nearly INR97 to below INR95 per USD.

* The easing of geopolitical tensions following the US-Iran peace agreement, the reopening of the Strait of Hormuz, and the subsequent decline in crude oil prices have significantly improved global risk sentiment. A softer US dollar, stable capital flows, and easing uncertainty have supported the INR's recovery, further aided by India's strong macroeconomic fundamentals and resilient domestic inflows.

Crude oil prices significantly cool off from the recent highs

* The announcement of the US-Iran ceasefire and improved traffic through the Gulf of Hormuz have driven a sharp decline in crude oil prices from their Apr– May'26 peaks to USD72–75 per barrel.

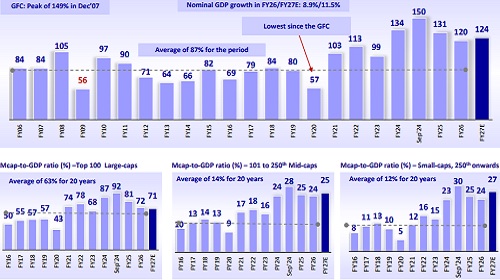

Corporate profit-to-GDP: Reaches unprecedented heights!

* The Nifty-500 corporate profit-to-GDP ratio surged to an all-time high of 5.2% in FY26, supported by corporate profit growth of 15.6% YoY, following 11.0% YoY growth in FY25 despite a high base of 32.6% YoY growth in FY24.

* Nominal GDP growth moderated to 8.9% YoY in FY26 from 9.7% YoY in FY25 and 11.0% YoY in FY24, resulting in corporate profits growing faster than the overall economy.

* The moderation in GDP growth was driven by a sharp slowdown in manufacturing activity and softer external demand, partly offset by continued strength in services, improving agricultural growth, and accelerating investment spending.

Valuations correct broadly; mid-caps remain firm on earnings strength

* The Nifty-50's one-year forward P/E stands at 18.6x, trading at an 11% discount to its long-term average of 21x and 25% below the peak levels seen in Sep'24. The Nifty Midcap-100 and Nifty Smallcap-100 continue to command valuation premiums, trading at 27.3x and 22.4x one-year forward P/E, respectively. While these multiples remain 16% and 27% above their LPAs, they are 23% and 7% below their respective Sep'25 peaks.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412