The Corner Office Interaction with the Ms. Gauri Kirloskar, Vice Chairperson & Managing Director, Kirloskar Oil Engines by Motilal Oswal Financial Services Ltd

Multiple growth levers

We recently hosted KOEL management, represented by Ms. Gauri Kirloskar, Vice Chairperson & Managing Director, and her team, for a meeting with a group of investors. We remain positive on the overall demand environment in the segments in which KOEL is currently operating such as powergen, industrial and even exports. Recent large order win from one of the hyperscalers is also positive for the company, with execution to be completed during this fiscal. We believe that the successful and timely completion of this order will open up opportunities from other data centre projects. Ongoing capex of the company will also enable it to capitalize on the strong demand in the powergen and industrial segments as highlighted in our previous note. The company’s initiatives on new product development will also yield results over time. We bake in execution of this order and raise our FY27/FY28 estimates by 3%/10%. We maintain BUY with a revised TP of INR2,750. Key risks to our estimates would come from delays in execution and lower margins going forward

Powergen segment has many growth levers for future

We expect KOEL’s powergen segment to benefit from

1) Volume and pricingled growth in below-750kVA gensets

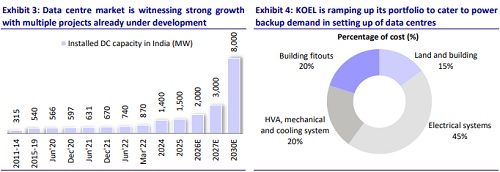

2) Scale-up of demand in HHP products across user segments which is coming from data centers and infrastructure sectors, including real estate, hospitality, hospitals and industrial customers

3) Future order wins in HHP/Optiprime from data centers as the company is scaling up across colocation, edge and hyperscalers

4) Capacity expansion for scaling up engine capacity. The company has a gross block of INR26b and is incurring a capex of INR21b over the next two years. This indicates the confidence of management in the overall demand scenario going forward. We, thus, believe that the powergen segment can potentially grow at a much faster pace, as the demand environment remains strong and the company is preparing itself with capex as well as with its work on bigger projects to target future opportunities. We bake in execution of HyperNext order for 96 units of 2500kVA Optiprime product in powergen segment and expect this segment’s revenues to clock 35% CAGR over FY26-29E.

Industrial segment targeting new applications using existing platforms

The company continues to expand its industrial business by developing application-specific engine solutions for sectors such as railways, defense, construction and mining, using its existing engine platforms and in-house engineering expertise. Management indicated that the transition to BS-V emission norms not only helped retain existing customers but also enabled the company to win new customer accounts through deeper engagement during the product validation process. Looking ahead, execution of the NPCIL order worth INR7.7b is expected to commence in FY27 and continue over the next couple of years. Execution of the Navy's Make-I category 6MW Medium Speed Marine Diesel engine order worth INR2.7b will begin from FY28-29 onward. Management believes the successful delivery of these strategic prototypes could unlock significantly larger opportunities in the nuclear and defense segments.

Financial outlook

We raise our estimates for the powergen segment to factor in execution of hyperscaler order. We thus expect revenue/EBITDA/PAT to post a CAGR of 28%/34%/38% over FY26-29E, with margin of 14%/15%/15% for FY27/FY28/FY29. We expect improved revenue to result in operating leverage gains, thereby driving margin expansion over FY27-29E.

Valuation and view

The stock is currently trading at 55.1x/38.5x/29.3x P/E on FY27/FY28/FY29E earnings. Adjusted for subsidiary valuation, KOEL is trading at 51.3x/35.9x/27.3x P/E on FY27/FY28/FY29E earnings. We reiterate our BUY rating with a revised SoTP-based TP of INR2,750

Key risks and concerns

Any slowdown in demand in key segments, aggressive competition from other players, and a surge in commodity prices could adversely impact overall earnings for the company.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412