South Africa Economy Update by CareEdge Ratings

FY27 Budget Signals Intent of Fiscal Discipline Key highlights of the FY27 Budget:

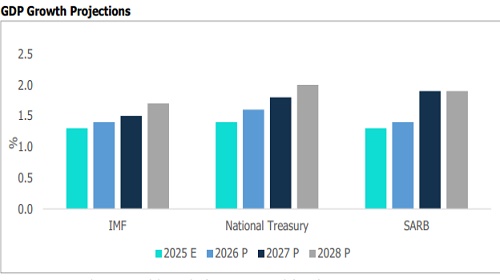

Growth is estimated to be higher in 2025 at 1.4%, from 0.6% in 2024. Growth is projected at 1.8% in 2026. The ongoing structural reforms may support the medium-term outlook.

Tax revenue collections were higher compared to budget estimates in FY26 following stronger valueadded tax (VAT) and corporate income tax (CIT) collections. Moderate revenue growth is expected for personal income tax (PIT) and VAT tax revenues in FY27

Expenditure was lower compared to budgeted estimates in FY26, mainly due to underspending by some government departments and lower debt service costs. For FY27, expenditure growth is expected to moderate, driven by a significant reduction in debt service costs and public sector wage growth. Notably, over the medium term (FY27-29), capital expenditure growth will be the fastest-growing expenditure item.

Fiscal metrics: Better-than-expected revenue and expenditure outcomes will enable the government to realise a primary surplus of 1% of GDP in FY26, up from 0.8% in FY25. The fiscal deficit for FY26 is now estimated at 4.5% of GDP, unchanged from FY25. For FY27, both the fiscal deficit and the primary surplus are expected to improve to 4.0% and 1.4%, respectively. Overall, debt-to-GDP is projected to peak in FY26 at 78.9% of GDP and then decrease to 77.3% of GDP in FY27.

Overall: The FY27 Budget outcome demonstrates the government's intent to maintain fiscal discipline. Further, the easing of tensions within the government of national unity (GNU) has also paved the way for policy continuity and improved sentiment. Despite these commendable achievements, the road ahead remains challenging, and the sustainability of fiscal discipline is key.

The IMF acknowledges that while fiscal deficits are moderating, debt is projected to continue to rise over the medium term. The Fund estimates debt at 78.5% in FY26, but it is expected to increase to 79% in FY27. Thereafter, debt-to-GDP will gradually increase, reaching 82.7% by FY30. Risks to debt sustainability include high contingent liabilities and weaker-than-expected growth outcomes.

Data Signals Positive Growth Momentum

Q4 2025 GDP data is scheduled for release on 10 March. The International Monetary Fund (IMF) estimates GDP growth for 2025 at 1.3%, in line with the South African Reserve Bank (SARB) and marginally lower than the National Treasury at 1.4%.

High-frequency data over the quarter have been generally positive, although there were notable decreases in the manufacturing, electricity, and wholesale trade sectors.

Manufacturing production declined 1.3% YoY in 2025 compared with 2024, with nine out of the ten subsectors showing weaker output. The “wood, paper, printing & publishing” and “iron & steel, metal products & machinery” sub-sectors were the most significant negative contributors. “Textiles & clothing” was the only sub-sector which experienced positive growth. On the other hand, mining production increased 0.1% YoY, following a 0.5% increase in 2024. There were increases in the production of manganese ore, diamonds, chromium ore, iron ore and nickel. However, the industry produced less copper, platinum-group metals, gold and coal. Consumer spending was stronger in 2025, with retail sales increasing 3.7% from 2.5% in 2024. General dealers and textiles & clothing were the most significant positive contributors. Lastly, motor trade sales grew by 2.0% in 2025 following two consecutive years of declines. The positive momentum was driven mainly by stronger new vehicle sales.

Risk-off Sentiment Will Dictate Rand Movements

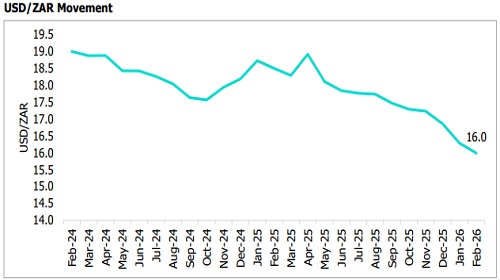

Over the past six months (September 2025 and February 2026), the South African Rand (ZAR) appreciated by 8.4% against the US Dollar (USD), and 5.1% over the past three months (December 2025–February 2026). In 2026 alone (January-February), the Rand gained 4.8%. During February, the Rand gained due to supportive factors on both the domestic and global fronts. Domestically, the Rand gained on the back of the FY27 Budget delivered on 25 February. The Budget reflected the government’s intent towards fiscal discipline and the active steps taken to achieve it. Further,

the FY27 Budget was presented against a favourable macroeconomic backdrop (see above). On the global front, the Rand benefited due to a weaker US Dollar. This was due to the US Supreme Court's ruling that all tariffs imposed under President Trump's emergency powers were illegal. However, in early March, emerging market currencies, including the Rand, were on the back foot due to risk-off sentiment in financial markets amid the escalating conflict between the US and Iran.

State of the Nation Address: Key Takeaways

In the State of the Nation Address (SONA), President Cyril Ramaphosa highlighted the positive economic accomplishments in FY26. Notably, the macroeconomic backdrop is favourable, given four consecutive quarters of positive economic growth, low inflation, which has enabled rate cuts, improvements in the country’s public finances and the removal from the Financial Action Task Force’s (FATF) grey list

The reform strategy under Operation Vulindlela has seen stabilisation of the energy supply, easing of logistical constraints, and other improvements. The President reaffirmed that Eskom’s unbundling will continue. Further, the National Treasury has made provisions for infrastructure spending, which will assist with infrastructure gaps in critical sectors. Over the medium term (FY27-FY30), public-sector infrastructure spending totals ZAR 1.07 trillion, with capital expenditure growing by 9.9% YoY. Investment will be supported by a pipeline of projects across energy (20%), water (17.4%) and transport infrastructure (39.2%). The government will continue to endorse greater private-sector participation, particularly in critical sectors such as logistics. This aligns with the broader reform of trying to crowd in the private sector, given that fiscal space remains constrained.

Structural weaknesses were also addressed- for example, the water sector and local governments. With respect to the water sector, a National Water Crisis Committee, chaired by the President, will be established to address sectoral challenges. With respect to local governments, ZAR 54 billion has been set aside for municipalities to improve their water and electricity revenues and direct the funds towards infrastructure maintenance. Municipalities will also be guided to curb water losses and illegal electricity connections. These developments are welcome ahead of local elections poised to take place this year.

South Africa Records Trade Surplus in January 2026

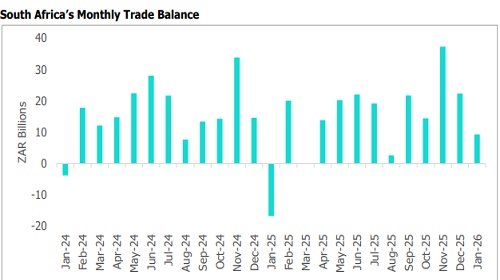

South Africa recorded a trade surplus of ZAR 9.3 billion in January 2026, reversing the ZAR 16.7 billion deficit registered in January 2025. Notably, the country had recorded trade deficits in January for the past three consecutive years (2023–2025), making this year’s surplus a significant improvement. The turnaround primarily reflects stronger export performance alongside a notable contraction in imports.

Exports increased by 4.9% YoY to ZAR 155.8 billion in January 2026, supported by stronger shipments of precious metals1 which increased by 53% YoY. Meanwhile, imports declined more sharply by 11.4% YoY to ZAR 146.5 billion during the same period. The contraction was largely driven by lower imports of mineral products (-14.5%) and reduced purchases of machinery, equipment, and chemical products (-7.6%).

Looking ahead to 2026, South Africa’s trade performance could benefit from ongoing reforms aimed at improving logistics efficiency and ensuring a more stable electricity supply. This may support exportoriented sectors such as minerals, vehicles and manufactured goods. In addition, the renewal of the African Growth and Opportunity Act (AGOA) until December 2026 provides short-term relief by maintaining preferential access to the U.S. market for South African exports. However, heightened geopolitical tensions, potential supply chain disruptions and volatile energy prices could raise import costs and dampen global demand, potentially moderating export momentum despite these supportive factors.

Headline Inflation Marginally Decreased in January

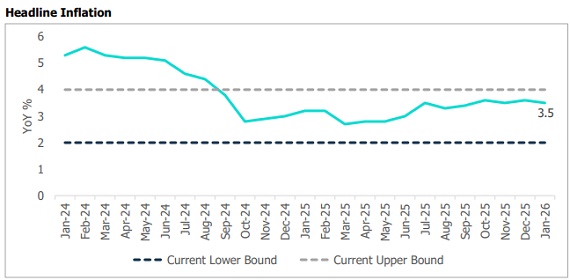

Headline inflation marginally decreased to 3.5% YoY in January from 3.6% in December. The decline was mainly due to a sharp decline in fuel prices, which contracted by 3.7% after four consecutive months of increases. This was due to a stronger Rand and lower oil prices. Food inflation was steady for the third consecutive month. However, meat prices continued to increase to 13.5% in January from 12.6% in December, due to the lingering impact of foot-and-mouth disease. On the other hand, core inflation increased marginally to 3.4% in January from 3.3% in December. Looking ahead, meat prices may remain elevated due to the continued impact of foot-and-mouth disease. There has been some progress on the vaccination rollout; however, this has been slow due to medication shortages. Nonetheless, lower global food prices and strong domestic crop production will help cushion the impact. On the other hand, fuel prices may be higher as oil prices pick up, fuelled by escalating conflict between the US and Iran. The SARB's baseline scenario is for inflation to moderate throughout 2026 from a peak of 3.6% in December 2025, averaging 3.3% for the year. However, the SARB has modelled an adverse scenario for 2026, with the Rand at ZAR 18.50 to the USD and oil prices at USD 75 per barrel. Under this scenario, they find that, instead of peaking at 3.6%, inflation will peak at 4% and converge toward its point target of 3% more slowly. Even in this scenario, inflation remains well-anchored.

Above views are of the author and not of the website kindly read disclaimer