Sell Tata Technologies Ltd For Target Rs. 500 by Motilal Oswal Financial Services Ltd

Encouraging FY26 exit

Auto shows early signs of recovery; execution and deal ramp-up critical for FY27

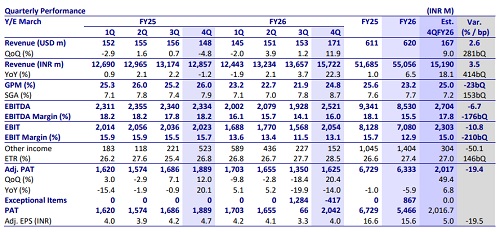

* Tata Technologies (TTL) reported revenue of USD171m in 4QFY26, up 12.4% QoQ in CC terms vs. our estimate of 9.5% QoQ in CC. Services segment revenue stood at USD133m, rising 11.9% QoQ in CC (organic 7.8% CC). EBIT margin was 13.1% (down 158bp QoQ), below our estimate of 15.2%. Adj. PAT was up 20.5% QoQ/down14% YoY at INR1,625m (below our estimate of INR2,017m).

* For FY26, TTL’s revenue grew 6.5% and EBIT/adj. PAT declined 12.9%/5.9% YoY in INR terms. For 1QFY27, we expect revenue/EBIT/adj. PAT growth of 28.6%/32.7/14.8% YoY. RoE came in at 14.6% in FY26 (vs. 19.8%/21.9%/ 23.7% in FY25/FY24/FY23).

* While 4QFY26 saw a strong rebound with improved deal momentum, growth remains in the early stages and is dependent on execution of recent wins and FVP conversions over the next few quarters. Auto spending is yet to see a clear inflection, with recovery still at an early stage, making execution a key monitorable. At ~29x 12M Fwd P/E, we view TTL’s valuations as premium relative to its current growth and peers; we assign a TP of INR500 and reiterate Sell.

Our view: Signs of auto ER&D recovery are emerging

* Strong exit quarter, but sustainability of momentum remains key: TTL reported a strong 4QFY26 with ~12.4% QoQ CC growth, led by deal rampups, JLR normalization and some contribution from ES-Tec. Demand improved in 2HFY26 as OEM decision-making resumed, and the pipeline now includes multiple full-vehicle programs (FVPs), with a few already closed and more expected in the near term.

* Management has guided for double-digit organic growth in FY27, with a relatively even quarterly progression and stronger 2H. That said, we believe the near-term growth trajectory will still depend on execution of recent wins and timely conversion of the FVP pipeline. We build in 10.6% YoY cc organic growth for FY27E.

* Automotive seeing early recovery: The automotive segment grew ~13.6% QoQ in USD terms, supported by normalization at key clients and improved activity across both anchor and non-anchor accounts. OEMs in Europe and North America have resumed investments in new product development, driven by competitive pressure and the need to accelerate product cycles. While this has led to a pickup in deal activity, including FVP wins, we believe the recovery is still at an early stage. Large programs typically ramp up gradually, and any delay in client decision-making or program execution could push out revenue realization

* Deal wins improving visibility, but ramp-up will be gradual: The company closed four large deals in 4Q and added two more post quarter, including a Japan entry via an FVP. These programs are multi-year in nature (18-36 months) and should support medium-term visibility. In our view, contribution from these deals should build progressively through FY27, with a more visible impact in 2H.

* Margins improving, but expansion back-ended: EBITDA margin improved ~200bp QoQ to 16% in 4Q, supported by operating leverage. Management has guided for FY27-exit EBITDA margin at >18%, driven by scale benefits, offshore mix and AI-led efficiencies. However, in the near term, margins may remain range-bound due to investments in talent, pyramid build and initial costs of new program ramp-ups. We estimate margins at ~16.6% in 1HFY27, with improvement towards ~17.6% by 4QFY27E.

* While 4QFY26 saw a strong rebound and deal momentum has improved, revenue growth remains in the early stages of recovery and is dependent on execution over the next few quarters. Margin expansion is likely to be gradual and back-ended. We remain watchful of deal ramp-ups, FVP conversions and sustainability of demand before turning constructive. Auto spending is yet to see a clear inflection and recovery remains at an early stage, and management execution over the next couple of quarters will be key monitorables.

Valuations and changes to our estimate

* Revenue growth is expected to be ~10% USD CAGR over FY26-28E. We keep our estimates largely unchanged.

* Margins are expected to improve gradually in 1HFY27, with EBITDA margin guided to exit FY27 at >18%. However, near-term margins are likely to remain range-bound (~16-17%) due to ramp-up costs, pyramid build and mix, with meaningful expansion back-ended.

* At ~29x 12M Fwd P/E, valuations remain premium relative to the current growth trajectory and execution risks. We retain our TP of INR500 and reiterate Sell.

Beat on revenue and miss on margins; Services segment grew 11.9% QoQ CC (vs. guidance of 10% QoQ cc)

* USD revenue came in at USD171m, up 12.4% QoQ in CC terms vs. our estimate of 9.5% QoQ CC growth. For FY26, revenue stood at USD620m, up 1.3% YoY CC.

* Services segment revenue stood at USD 133m, grew 11.9% QoQ CC.

* Auto segment revenue was 81% (vs. 80% in 3Q).

* Adj. EBIT margin was 13.1% (down 158bp QoQ), below our estimate of 15%. For FY26, adj. EBIT margin stood at 12.9% vs. 15.7% in FY25.

* Adj. PAT was up 20.5% QoQ/down 14% YoY to INR1,625m (below our estimate of INR2,017m). For FY26, adj. PAT stood at INR6,333m, down 5.9% YoY.

* Onshore-offshore revenue mix was 67%-33% vs. 61%-39% in 3QFY26.

* The net headcount was up 0.5% QoQ in 4QFY26, taking the total headcount to 12,646. Attrition (LTM) increased by 40bp QoQ to 16.2%.

* The company declared a final dividend of INR8.35/share for FY26 and a special dividend of INR3.35/share, aggregating to a total dividend of INR11.7/share for FY26.

Key highlights from the management commentary

* Demand environment improved meaningfully in 2HFY26 as geopolitical and tariff-related uncertainty eased, prompting OEMs to restart decision-making after a prolonged pause spanning much of FY25 and 1HFY26.

* Non-Chinese OEMs in Europe and North America are now reinvesting in new product development to address competitive pressure from Chinese players -- a dynamic that is directly influencing order book improvement.

* Management guided for double-digit organic CC revenue growth in FY27, excluding any inorganic contribution from Aztec; growth is expected to be broadly consistent across quarters, with 2HFY27 likely growing faster as pipeline converts.

* More than 50% of the engineering workforce is now AI-ready, positioning Tata Tech well to drive productivity and delivery improvements through FY27.

* Chromosome AI, Tata Tech's proprietary AI orchestration platform, acts as an integration layer across product development stages, enabling workflow automation, faster decision-making, and cross-functional collaboration across multi-geography programs.

* Management views AI not as an experiment but as a core execution enabler, helping compress cycle times, improve quality, and enhance delivery predictability on complex programs.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412