RBI Policy:Status Quo Maintained Amid Elevated Uncertainly by CareEdge Ratings

As expected, the RBI’s Monetary Policy Committee (MPC) unanimously decided to maintain the status quo on repo rate, keeping it at 5.25%. The monetary policy stance was maintained at ‘neutral’. The April monetary policy comes against the backdrop of heightened geopolitical tensions in West Asia, which have threatened energy supply chains and pose a challenge for an energy importer like India. Despite the recently announced ceasefire, the situation remains fluid and warrants close monitoring.

Given high energy prices and supply-side bottlenecks, the GDP growth forecast for FY27 has been revised downwards, while inflation projections have been revised upwards. While a ceasefire in the West Asia war has been announced for two weeks, much will depend on how the conflict situation evolves and the time required to resolve supply bottlenecks.

RBI Lowers Growth Forecast for H1 FY27

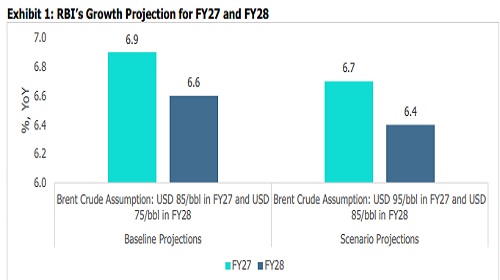

Amid higher energy prices and supply concerns, India’s GDP growth projection for H1 FY27 has been revised downward to 6.8%, from 7.0% in the previous policy review in February. For the full year FY27, the RBI projects GDP growth at 6.9%, based on the assumption of crude oil averaging USD 85/bbl. However, given the volatile situation in West Asia, the RBI highlighted downside risks to growth. In comparison, our FY27 growth projection stands at 6.7%, premised on a higher crude oil assumption of USD 90/bbl. This marks a downward revision from our pre-conflict GDP growth projection of 7.2%, which was based on crude oil prices averaging USD 60–70/bbl.

Going forward, the duration of the conflict and its potential impact on global supply chains will be key factors to monitor. While the recent ceasefire in West Asia is a positive development, the situation remains fluid and warrants close observation. Persistent geopolitical tensions, volatile financial market conditions, and evolving trade dynamics continue to pose risks to the overall growth outlook.

While growth in FY27 is expected to be affected by an energy price shock, the RBI’s monetary policy report also indicates a notable slowdown in projected growth momentum for FY28. Under the baseline scenario—assuming crude oil at USD 75/bbl—growth is projected at 6.6% for FY28. In an alternative scenario with crude oil at USD 85/bbl, growth is estimated slightly lower at 6.4% for FY28. Overall, these projections suggest that economic growth may remain below the 7% potential growth rate estimated in the Economic Survey. This can have implications for the policy rate decisions.

Even though energy prices have moderated following a ceasefire announcement, the extent of further moderation will depend on how the situation evolves and the time required to resolve supply bottlenecks and restore normal supply conditions. In this context, it is important to note that India’s CPI inflation has become more sensitive to retail energy prices under the new series, with the combined weight of diesel, petrol, and LNG rising to 4.8% from 2.4% earlier.

Assuming a full pass-through, a USD 10 increase in crude oil prices can lead to an estimated 55–60 bps rise in headline inflation, with around 45 bps stemming from the direct effects and 10–15 bps from the indirect effects. In the current scenario, indirect inflationary pressures could be higher due to the risk of supply disruptions. We expect the direct effects of higher global crude oil prices on inflation to remain somewhat contained, assuming the price increase burden is shared by households, OMCs, and the government. The OMCs have so far enjoyed high gross refining margins, and, as per our estimate, they may be able to absorb an increase in Brent crude oil prices up to USD 106/bbl

This estimate considers the recent cut in special additional excise duty on petrol and diesel by the government. Apart from higher crude oil prices, the inflationary scenario also faces upside risks from disruptions to the global gas supplies. Beyond the direct impact of higher energy prices, concerns are rising over second-round effects stemming from elevated input costs. There are also concerns around higher food inflation with the rising probability of weather disruption in the form of El Niño.

Overall, assuming global crude oil prices average at USD 90/bbl in FY27, we expect India’s CPI inflation to average between 4.5-4.7%. We have revised our projection upward from the earlier 4.3%, which factored global crude oil prices ranging between USD 60-70/bbl.

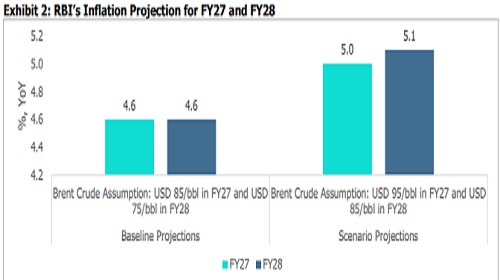

As per the RBI’s monetary policy report, inflation for FY28 is projected at 4.6% under the baseline scenario, which assumes crude oil prices at USD 75/bbl. Under an alternative scenario, assuming crude oil prices of USD 85/bbl, inflation is expected to average 5.1% for the year.

Durable Cessation of Hostilities May Lead to FPI Inflows and Support Rupee

If the US–Iran ceasefire proves durable and culminates in a sustained peace agreement, it could be constructive for India’s external sector. Energy prices have corrected sharply following the announcement. That said, further downside in energy prices will remain contingent on the time taken to rebuild extraction and production capacity in the Persian Gulf. Given that energy prices are likely to average USD 85-90/bbl in FY27, higher than last year, India’s import bill is expected to be higher. Prioritisation of domestically produced refined petroleum products towards local markets amid tighter crude oil and gas supplies, and the conflict’s impact on West Asian demand, may affect India’s exports. Remittances from the region may also be impacted. Taking these factors into account, we project the current account deficit at 2.1% of GDP in FY27, compared with our pre-conflict estimate of 1%.

On the capital account, net FDI flows (gross inflows net of repatriation and outward FDI) have remained negative for six consecutive months. Elevated repatriations and outward FDI have continued to weigh on net inflows. During 10M FY26, net FDI inflows stood at USD 1.7 billion, compared with USD 2.2 billion in the corresponding period of the previous year.

FPIs recorded outflows of USD 16.6 billion in FY26, largely driven by USD 13.6 billion of outflows in March 2026. Thus far in April 2027, FPI outflows amount to USD 5.4 billion. While prevailing uncertainties are likely to keep investors cautious, a moderation in risk aversion should support improved FPI flows over the near-to-medium term.

With the rupee remaining significantly undervalued on a REER basis as of the end of February 2026, a durable improvement in the geopolitical environment provides scope for appreciation. In addition, recent measures undertaken by the RBI are expected to curb speculative activity and help reduce currency volatility. If crude oil prices average USD 90/bbl in FY27, we expect the rupee to average 92-93/USD over the year.

RBI to support Liquidity Conditions

The banking system’s average liquidity surplus moderated to Rs 1.6 trillion in March, down from an average surplus of Rs 2.6 trillion in February. The moderation is largely due to tax outflows and forex interventions. This has also led to a spike in the weighted average call rate (WACR). On the liquidity front, the Governor reiterated the RBI’s commitment to maintaining comfortable liquidity conditions. We expect the RBI to continue supporting liquidity conditions, which is critical for the effective transmission of previous rate cuts and for supporting credit growth.

Elevated oil and gas prices are stoking fears of increased fiscal and inflationary pressures, thereby pushing up Gsec yields across tenors. We estimate the fiscal burden from the excise duty cut on petroleum products, along with the possibility of an increase in subsidy burden and lower tax revenue collections, to be around 0.5% of GDP in FY27. If the West Asia situation stabilises, further moderation in the energy prices should put some downward pressure on G-sec yields. As per our baseline scenario with Brent averaging USD 90/bbl, we expect G-sec yields to average 6.8 – 6.9% in FY27.

Way Forward

Even with the recent two-week ceasefire, the global situation remains volatile, and energy prices are expected to remain high compared to the pre-war period. Going forward, we expect the RBI to maintain the status quo on policy interest rate. While there are upside risks to inflation, the impact of higher global crude oil prices on CPI inflation will be somewhat mitigated by the sharing of the burden between the government, OMCs and households. Given the lingering growth concerns, the RBI will not be in a hurry to reverse the rate cycle. In fact, it can explore the possibility of a rate cut towards the end of the fiscal year if the growth outlook deteriorates significantly below long-term potential growth.

Above views are of the author and not of the website kindly read disclaimer