Neutral Navin Fluorine International Ltd for the Target Rs. 6,850 by Motilal Oswal Financial Services Ltd

Continued operational strength with diversified growth levers

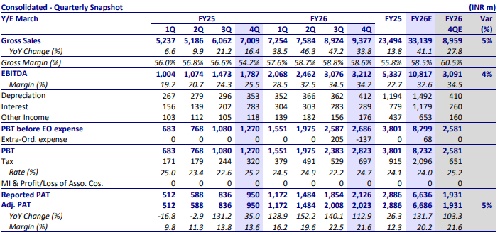

Operating performance in line with estimates

* Navin Fluorine International (NFIL) maintained its robust performance in 4QFY26, with revenue growing 34% YoY, driven by broad-based strength across all segments. HPP/Specialty Chemical/ CDMO revenue increased by 21%/39%/ 61%, while EBITDA surged 80% YoY, led by volume growth, operating leverage, a favorable product mix and a constructive pricing environment for HFC.

* The outlook remains positive, underpinned by a well-diversified portfolio across products, customers, and geographies. We expect the HPP segment to continue to deliver sustainable growth, supported by a firm pricing environment and ongoing capacity expansion initiatives, while the Specialty Chemicals business is poised to maintain its strong momentum, backed by robust order visibility and meaningful scale-up across existing molecules.

* The outlook for the CDMO segment remains equally healthy, driven by a balanced portfolio spanning late-stage and commercial molecules as well as early-stage pipeline opportunities.

* We maintain our FY27/FY28 earnings estimates and reiterate our Neutral rating on the stock with a TP of INR6,850 (40x FY28E EPS).

Robust profitability supported by segmental momentum

* NFIL reported revenue of INR9.4b (est. in line), up 34% YoY, driven by growth across all three segments.

* Gross margin stood at 58.6% (up 440bp YoY) and EBITDA margin stood at 34.2% (25.5% in 4QFY25), driven by a favorable product mix and operational leverage.

* EBITDA stood at INR3.2b (est. in line), up 80% YoY, and adj. PAT grew 2.1x YoY to INR2b (est. in line), adjusted for the write-back of excess labor code provisions amounting to INR137.2m.

* HPP revenue grew 21% YoY to INR3.9b, driven by higher volumes and improved realizations, while the pricing environment for HFC remained constructive.

* Specialty Chemicals revenue grew 39% YoY to INR3.6b, driven by 49% growth in the international business.

* CDMO business sustained its growth trajectory, with revenue growing 61% YoY to INR1.8b.

* India/international revenue grew by 16%/45% YoY in 4QFY26.

* In FY26, revenue/EBITDA/adj. PAT grew 41%/2x/2.3x to INR33.1b/INR10.8b/ INR6.7b.

* FY26 net debt stood at INR11.3b, while OCF stood at INR8.9b.

Highlights from the management commentary

* CDMO: The CDMO portfolio remains well-balanced, with ~50-55 molecules under engagement, reflecting an even mix of late-stage/commercial and earlystage projects. This is complemented by a strategic focus on expanding across high-growth therapeutic areas, including oncology, respiratory, cardiovascular, neurology, and animal health, in partnership with global innovators.

* Outlook: Multiple growth projects, including additional HFC capacity (R32 MPP) and the Chemours project, are nearing transition from the investment phase to revenue generation, with meaningful contributions expected from FY27 onward. Management has reiterated its EBITDA margin guidance of ~30% for the full year (±1-2%).

* Macro environment: Despite geopolitical tensions in the Middle East causing raw material price inflation, there has been no material demand disruption, and the raw material cost increases are largely being passed on to customers.

Valuation and view

* Considering a strong FY26 performance, we believe NFIL is well positioned to sustain its growth momentum, supported by the constructive pricing environment, growing international exposure, robust order visibility and operational leverage, led by capacity ramp-up.

* The outlook is further supported by: 1) a strategic partnership with Chemours to foray into high-growth advanced materials, 2) planned investment for increasing the R32 capacity (likely to be operational by 3QFY27) and MPP debottlenecking for the specialty chemical plant at Dahej (targeted commissioning by 3QFY27), 3) 13 newly launched agrochem molecules in FY26, and 4) the ramp-up of the AHF plant (commissioned in 4QFY26).

* We expect a CAGR of 20%/15%/15% in revenue/EBITDA/adj. PAT over FY26-28. The stock is trading at ~40x FY28E EPS of INR171 and ~25x FY28E EV/EBITDA. We value the company at 40x FY28E EPS to arrive at our TP of INR6,850 and we reiterate our Neutral rating.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412