Neutral Info Edge Ltd for the Target Rs 1,050 by Motilal Oswal Financial Services Ltd

Non-recruitment segments anchor growth 99acres momentum improving; margins to remain range-bound

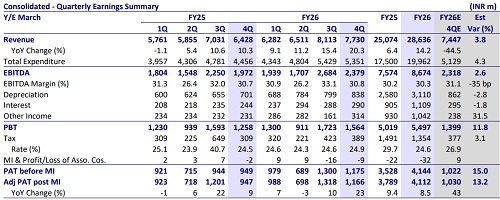

* Info Edge (INFOE)’s standalone revenue stood at INR8.1b in 4QFY26, up 17.2% YoY/5.3% QoQ, above our estimate of ~INR7.6b. EBITDA margin came in at 43.4% (up 90bp/570bp QoQ/YoY), above our estimate of 39%. Total billings rose 7.4% YoY to INR10.6b.

* Adj. PAT was up 18.4% YoY to INR2.9b (vs. our est. of INR2.7b).

* In FY26, its revenue/EBITDA/adj. PAT grew 15%/16.3%/13.5% YoY. In 1QFY27, we expect its revenue/EBITDA/adj. PAT to grow 12.9%/21%/19.2% YoY. We reiterate our Neutral rating on the stock with a TP of INR1,050, implying a 9% upside

Highlights from the management commentary

* Recruitment: Full-year FY26 standalone recruitment billings grew ~10% to ~INR2.4b, with revenue up ~14% to ~INR2.3b; operating profit margin held at ~57%, modestly improving versus prior year.

* Billing growth moderated to the 9-11% range across all quarters of FY26, stepping down from ~18% YoY in Q4 FY25, reflecting geopolitical headwinds, tariff-related uncertainty, and a generally cautious corporate hiring stance.

* 99acres: 99acres now commands ~52% web traffic timeshare (April figure), up from ~46% a quarter prior; app traffic share is ~54% overall and ~67% on iOS, reflecting consistent market share gains across categories.

* Medium-term target: double billings over three years (to ~INR10b) from the FY26 base of ~INR5b, with a ~25-30% EBITDA margin; management expects the business to return to cash generation in FY27 if current momentum is maintained.

* Management views AI as a structural tailwind, not a disintermediation risk, for its platforms; proprietary data, two-sided network effects, and deep domain context are cited as the key moats enabling better matching and workflow automation across all verticals.

Valuation and view

* We tweak our estimates by ~3% for FY27/28E. While growth remains steady across recruitment and 99acres, recruitment continues to track at ~10% growth with a still-cautious hiring environment, limiting the scope for any sharp acceleration.

* At the same time, we do not see a meaningful step-up in margins in the near term, given continued investments and only moderate growth. In our view, most of the near-term growth is already factored into current valuations, leaving limited room for re-rating.

* We value the company’s operating entities using DCF valuation. Our SoTP-based valuation indicates a TP of INR1,050. Reiterate Neutral.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412