Neutral CDSL Ltd for the Target Rs.1,160 by Motilal Oswal Financial Services Ltd

Weak performance; the KYC segment to dent revenue

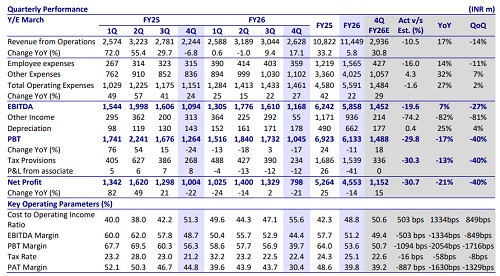

* CDSL’s operating revenue rose 17% YoY but declined 14% QoQ to INR2.6b (11% miss). The sequential decline was led by a sharp fall in the IPO/corporate actions segment income. For FY26, revenue grew 6% YoY to INR11.4b.

* Operating expenses grew 27% YoY/flat QoQ to INR1.5b, driven by a 32%/14% YoY increase in employee/other expenses. EBITDA rose 7% YoY but declined 27% QoQ to INR1.2b, resulting in an EBITDA margin of 44.4% (vs. 48.7% in 4QFY25 and 52.9% in 3QFY26). For FY26, EBITDA declined 6% YoY to INR5.9b.

* PAT for the quarter declined 21% YoY and 40% QoQ to ~INR798m (31% miss due to a miss on revenue growth). PAT margin came in at 30.4% vs. 44.8% in 4QFY25 and 43.7% in 3QFY26. For FY26, PAT declined 14% YoY to INR4.6b.

* In the KYC segment, with an ~80:20 fetch-to-creation revenue mix, the recent pricing revisions—sharp cuts in creation charges (INR20 to INR5) and moderation in fetch charges (INR35 to INR28)—are expected to have a meaningful adverse impact on CVL’s revenue.

* We cut our earnings estimates by 15%/17% for FY27/FY28 to reflect the impact of KYC pricing cuts in the CVL segment and slower traction in transaction revenues, while costs remain largely unchanged. We now expect a revenue/EBITDA /PAT CAGR of ~10%/8%/9% over FY26–28E and maintain a Neutral rating with a oneyear TP of INR1,160 (44x FY28E P/E).

IPO & corporate actions lead to a sequential dip in revenue growth

* The transaction revenue increased 20% YoY to INR 590m, while remaining flat QoQ due to moderation in the market activity during the quarter.

* Annual issuer charges grew 31% YoY to INR 1.1b, driven by growth in unlisted issuers and rising folios. However, it remained flat QoQ due to a slowdown in new unlisted issuer additions during the quarter.

* IPO and corporate action revenue dipped 32% YoY/71% QoQ due to lower corporate activity and a weak IPO pipeline during the quarter. However, this is likely to recover with a strong pipeline of large IPOs going forward.

* Online data charges grew 32% YoY to INR490m (flat QoQ), with an ~80:20 fetch-to-creation mix; recent pricing cuts are expected to materially impact CVL’s revenue.

* During FY26, the revenue from operations of its subsidiary, CVL, declined to INR1.8b from INR2.3b in FY25, while total expenses were at INR1.2b vs. INR1.1b in FY25. PAT declined to INR554m vs INR1.1b.

* The insurance segment has scaled to partnerships with 49 insurers (vs. 45 in 4QFY25), with policies rising to 2.1m across 2.3m e-IAs (vs. 1.8m policies in 1.8m e-IAs YoY).

* Other operating income declined 82%/81% YoY/QoQ to INR55m due to the mark-to-market impact. It comprised E-CAS/E-Voting income of INR120.8m/ INR55.8m for the quarter.

* Total expenses surged 27% YoY but were flat QoQ at INR1.5b, led by a 41% YoY increase in tech expenses and a 32% YoY rise in other expenses. CIR stood at 55.6% vs. 51.3% in 4QFY25 and 47.1% in 3QFY26.

* Impairment costs for the quarter stood at INR76.2m vs. INR40m in 3QFY26.

* Total number of issuers and ISINs grew 34%/29% YoY and 4%/5% QoQ to 48.1k/0.1m.

* Demat account additions for the quarter stood at 7.4m in 4QFY26 vs. 6.4m in 4QFY25 and 7.6m in 3QFY26. Assets Under Custody (AUC) stood at INR77t, progressing from INR71t in 4QFY25 but declining from INR85t in 3QFY26.

Key takeaways from the management commentary

* Received no objection letter to set up a separate business unit at GIFT City as the first KYC-registering agency to support international investors and issuers.

* Continues to invest in scalable, tech-driven infrastructure—strengthening application, network, and cybersecurity layers while expanding APIs to enable seamless onboarding, transactions, and high-volume processing.

Valuation and view

* While steady demat account additions (7.4m in 4QFY26) and healthy unlisted company admissions continue to underpin recurring revenue visibility, ongoing investments in talent and technology may limit operating leverage, with recent KYC pricing revisions further weighing on revenue growth.

* We have cut our earnings estimates by 15%/17% for FY27/FY28 to reflect the impact of KYC pricing cuts in the CVL segment and slower traction in transaction revenues, while costs remain largely unchanged.

* We now expect a revenue/EBITDA/PAT CAGR of ~10%/8%/9% over FY26–28E and reiterate our Neutral rating with a one-year TP of INR1,160 (premised on 44x FY28E P/E).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412