Neutral Aditya Birla Fashion and Retail Ltd for the Target Rs 65 by Motilal Oswal Financial Services Ltd

Strong 4Q growth; cash outflow remains high in FY26

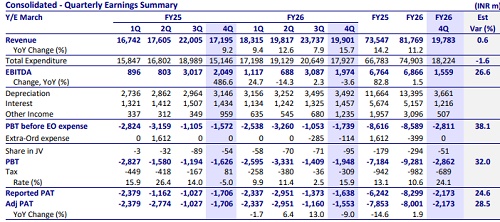

* Aditya Birla Fashion and Retail (ABFRL) delivered a strong 4QFY26, with ~16% YoY revenue growth and ~29% YoY comparable EBITDA growth, driven by a healthy ~17% YoY growth in Pantaloons, ~380bp YoY ethnic margin expansion, and losses reducing in TCNS and TMRW.

* FY26 revenue grew ~11% YoY, driven by Ethnic (+14%) and TMRW (+34%), while Pantaloons inched up ~4% YoY. Estimated pre-Ind-AS operating loss stood at ~INR4.6b, with a loss margin at ~5.7%.

* Pantaloons reported a solid 14% LTL growth in 4Q, aided by a shift in EoSS and rising customer acceptance of the refreshed brand identity. EBITDA margin expanded ~30bp YoY (~185bp beat) despite continued investments toward OWND ramp-up.

* Ethnic portfolio EBITDA grew 42% despite muted ~3% revenue growth, driven by lower losses in TCNS, which remains on track for breakeven by FY27-exit.

* TMRW revenue grew ~45% YoY in 4Q, while losses declined ~25% YoY. FY26 revenue grew 34%, with management expecting losses to have peaked in FY26, with breakeven targeted by FY29.

* FY26 FCF outflow stood at ~INR16b, driven by higher working capital, higher investments into TMRW, OWND, and Galeries Lafayette, leading to ~INR10.8b increase in net debt. However, management noted that cash outflow remained on track and expects ~INR6b/INR5b cash outflows in FY27/FY28. with company expected to become FCF positive by FY29.

* We tweak our estimates for FY26 actuals and model a CAGR of ~13%/ 25% in revenue/reported EBITDA over FY26-28E, though we do not expect ABFRL to achieve pre-IND AS EBITDA breakeven by FY28.

* We value ABFRL on an SoTP basis and ascribe a revised TP of INR65. We reiterate our Neutral rating on the stock.

Valuation and view

* Consistent revenue growth and steady margin expansion in Pantaloons with the refreshed brand identity, along with loss reduction in TCNS and scale-up of TASVA/OWND, remain the key long-term catalysts for ABFRL.

* However, higher investments and/or slower profitability ramp-up in some of the currently loss-making businesses could remain a key drag on overall profitability and cash flows for ABFRL.

* We tweak our estimates for FY26 actuals and model a CAGR of ~13%/ 25% in revenue/reported EBITDA over FY26-28E, though we do not expect ABFRL to achieve pre-IND AS EBITDA breakeven by FY28.

* We value ABFRL on an SoTP basis. We assign an EV/EBITDA multiple of 9x to Pantaloons (inc. OWND!), and 13x to the designer-led ethnic portfolio. We ascribe EV/sales multiple of 1x/0.9x/1.5x to ABFRL’s attributable stakes in premium ethnic/TMRW/Luxury Retail portfolio to arrive at our revised TP of INR65 (earlier INR70). The cut in TP is largely attributed to higher net debt. Reiterate Neutral.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412