MO Advisor - July 2026 by Motilal Oswal Wealth Mangement

Technical & Derivatives Outlook

* Nifty index started June on a positive note but witnessed selling pressure in the first week, slipping towards 23000 marks. It later recovered steadily over the following weeks and tried to reclaim the psychological 24K zones. In the tug of war between the bulls and bears, the index managed to find strong support based buying while multiple hurdles were seen intact near 24000-24250 zones. Slight profit booking was seen in the final week but the index managed to close near 23900 highlighting buy on decline at crucial support zones.

* Technically, Nifty formed a small bodied bullish candle on the monthly chart, indicating volatility after the sharp recovery from lower levels. The index also recouped a major part of the previous month’s weakness. For July, positional supports are seen at 23500 and then 23300 zones, while on the upside hurdles are placed at 24500 then 24750 zones.

NIFTY

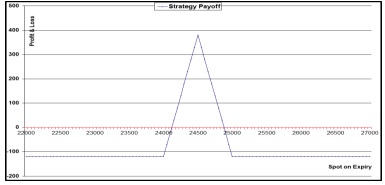

BULL CALL BUTTERFLY :

July Series

• June series witnessed a tussle between bulls and bears. Buying was seen from lower levels while selling pressure continued at higher levels.

• Index remained confined to a broad 23500–24500 range from last two series and requires a decisive breakout above this band to trigger the next leg of the rally.

• On the derivatives front, maximum Call OI as well as maximum Put OI are concentrated at the 24000 strike indicating it as a crucial pivot level for the series.

• A Bull Call Butterfly Spread strategy is recommended to capitalize on a moderately bullish outlook as buy on dips expected to continue.

BUY 1 LOT OF 24000 CALL

SELL 1 LOT OF 24500 CALL

SELL 1 LOT OF 24500 CALL

BUY 1 LOT OF 25000 CALL

Bank Nifty

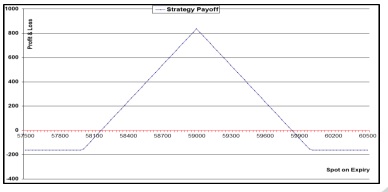

BULL CALL BUTTERFLY :

July Series

• Bank Nifty index has been forming higher lows structure on monthly time frame from last three months as buying is visible at lower levels.

• On weekly scale it is consolidating from last three weeks but holding well above its crucial breakout zone.

• On the derivatives front, maximum Put OI is at 57000 strike while Call OI are concentrated at the 60000 strikes, indicating a positive with overall buy on dips stance.

• Hence, a Bull Call Butterfly Spread is recommended to play the upward momentum going ahead.

BUY 1 LOT OF 58000 CALL

SELL 1 LOT OF 59000 CALL

SELL 1 LOT OF 59000 CALL

BUY 1 LOT OF 60000 CALL

Commodities & Currency Outlook

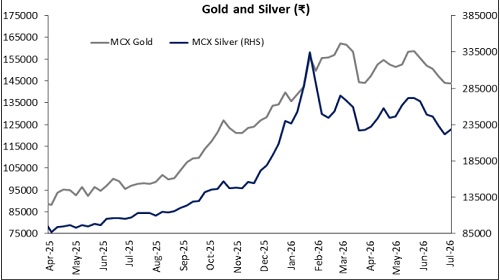

* Gold traded under pressure as geopolitical support was offset by a stronger dollar and Treasury yields

* Silver underperformed gold during the month, pushing the Gold/Silver ratio back near 70

* US-Iran tensions dominated early June, keeping a geopolitical premium embedded in bullion prices

* Strait of Hormuz concerns threatened oil supply, lifting crude prices and inflation expectations

* Markets reduced geopolitical premium as ceasefire headlines & diplomatic negotiations resurfaced

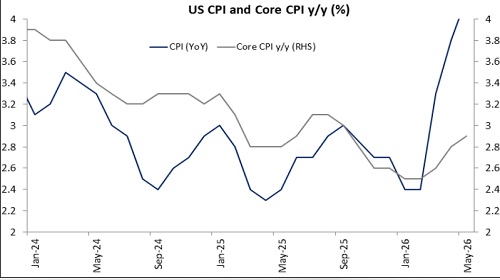

* US headline inflation remained influenced by energy prices, while core inflation showed signs of easing

* US 10-year breakeven inflation remained broadly stable near 2.3%, suggesting markets were not pricing a renewed inflation shock

* Fed maintained slightly hawkish stance, citing persistent inflation risks

* Fed funds futures now price in at least one rate hike in 2026, amidst higher inflation expectations

* Hawkish comments from prospective Fed Chair Kevin Warsh reinforced the higher-forlonger narrative

* BOJ raised their interest rate to 1%, reducing interest rate differential with US & lifting long term japan yields and creating panic in market

* US non-farm payrolls increased by 172,000 in May, while unemployment held at 4.3%, highlighting continued labour market resilience

* PMI and consumer confidence were slightly dull in the previous month

* The Dollar Index recovered and is table above 101, while US 10Y Yield is also hovering around 4.5%, adding another headwind for precious metals.

* Fluctuation in USDINR kept market participants on domestic front on edge

* Gold ETFs recorded net outflows of 16 tonnes during May, with selling continuing into early June

* CFTC speculative positioning stabilised after heavy liquidation in March and April but, fresh long additions remained limited.

* Official sector demand remained a structural pillar for gold despite softer ETF investment demand.

* Poland remained among the largest official buyers during Q1, continuing its reserve diversification

* The PBoC purchased 10 tonnes in May, its largest monthly addition since December 2024, extending its buying streak to 19 consecutive months and lifting reserves to 2,332 tonnes 8.9% of total reserves).

* Chinese gold ETF holdings declined by 8.3 tonnes to 293t in May as first monthly outflow in eight months

* Domestic discounts narrowed sharply from ~US$150/oz after duty hike to ~US$25/oz by mid-June, signalling improving market balance.

Commodities & Currency Outlook

* Indian gold ETF investors booked profits during May, although inflows resumed in June

* Silver fundamentals remained mixed, with stronger Chinese imports offset by rising London inventories and subdued manufacturing sentiment and dent in safe haven demand

* Month of July is likely to be driven by US inflation, labour market data, Fed’s and other central banker’s communication and developments in the Middle East.

* Relief rallies could be seen but, until there is no clarity on interest rates or middle east tensions, both Gold and Silver could trade in a broad range.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041