MO 20 Quant Momentum Model Portfolio - July 2026 by Motilal Oswal Wealth Mangement

Ideal For Capturing Strong Market Trend

This strategy focuses entirely on trend durability, selecting securities that have consistently outperformed their peers and are positioned to continue their upward trajectory. By eliminating noise and concentrating on quantifiable price leadership, the Momentum Model ensures that the portfolio stays aligned with the market’s strongest winners at any given time.

Designed for investors who seek a disciplined, data-led framework that adapts dynamically to market shifts, the Momentum Model offers a high-conviction approach to capturing sustained rallies, improving return potential while maintaining systematic risk control.

Methodology

1. Works on the top 500 listed companies by market cap

2. Evaluates short-term and long-term price trends to identify stocks with strong upward momentum, which is ranked as Momentum Score.

3. The strategy also integrates secondary filters: Quality, Earnings Surprise and Valuation to ensure fundamentally strong momentum stocks make it into the portfolio

4. Employs a systematic, repeatable, and forward looking approach to stock selection.

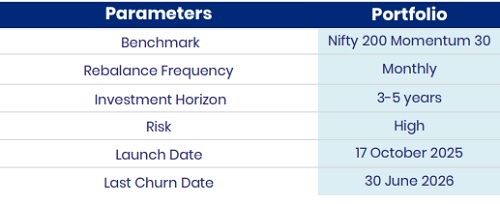

Portfolio Parameters

Portfolio Attributes

Know Your Factor

Momentum

Momentum evaluates a stock's price strength across short (1–10 days), mid (10–90 days), and long-term (6–12 months) timeframes, alongside sector-relative performance. Stocks showing steady, consistent upward movement—particularly in outperforming industries—score higher, while volatile or erratic price action is penalised, ensuring trends reflect genuine underlying strength rather than short-term noise.

Value

The Value factor identifies fundamentally undervalued companies by blending intrinsic valuation—discounting projected earnings to estimate fair value—with peer benchmarking using metrics like P/E, P/B, and EV/EBITDA. Sector-adjusted comparisons ensure fairness across industries, surfacing attractively priced, fundamentally strong businesses that the market has yet to fully recognise.

Quality

Quality assesses the credibility and sustainability of reported profits by favouring companies whose income is backed by strong operating cash flows, low accruals, consistent margins, and efficient asset use. One-time adjustments are identified and penalised, ensuring the model rewards genuinely repeatable performance over figures inflated by accounting distortions.

Earnings Surprise

Earnings Surprise tracks how analyst forecasts and recommendations evolve over time, capturing upward estimate revisions and rating upgrades across multiple periods. Stocks where earnings expectations and analyst conviction move consistently in the same direction are rewarded, as coordinated shifts often signal improving fundamentals before the broader market fully reacts.

Institutional Holding

The Institutional Activity factor monitors how mutual funds, insurers, pension funds, and asset managers allocate capital over time. Rising institutional ownership particularly when aligned with broader investment themes signals deep researched conviction. Early accumulation patterns,, often provide valuable leading indicators of future price leadership

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041