Mauritius Economy Update by CareEdge Ratings

Growth momentum weakened in Q4 2025

Mauritius witnessed loss of momentum in economic activity in the last quarter of 2025. Annual GDP growth slowed to 2.7% YoY from a revised 3.3% in Q3 2025. This slowdown was triggered by moderating domestic demand, sluggish investment activity amid elevated borrowing costs and a thinning project pipeline, as well as weak external demand.

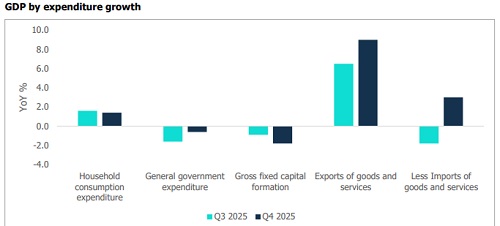

On the expenditure side, investment fell by 1.8% YoY in Q4 2025 as against a 0.9% decline in Q3, marking a fifth consecutive quarter of decline. This downturn was driven by a sharp fall in investment in machinery and equipment (-6.2%). While residential projects and general works nudged up building and construction activity (+0.5%), nonresidential investment remained weak.

Household consumption supported growth in Q4, albeit at a slower pace, while government expenditure exerted a drag on overall consumption. On the external front, net exports contributed with growth (+9%) outpacing import growth (+3%). The improvement in exports was driven by services, particularly financial services and tourism, whereas import growth was primarily led by goods.

Looking at production, the construction sector’s slowdown to 1.0% YoY in Q4 (from 1.3% in Q3) reflects a broader investment slump. This follows a period of contraction in the earlier quarters of 2025. The subdued performance is driven by a thinning project pipeline, ongoing execution delays, weaker activity in commercial and office developments, and slower public sector spending. In addition, increasing construction costs, evidenced by a 4.9% increase in the Construction Price Index in 2025, up from 4.7% in 2024, as well as high borrowing costs, have weighed on project viability and delayed new project launches. Real estate sector growth also moderated to 1.3% from 1.8% in Q3, reflecting softer demand and spillovers from weaker construction activity, while accommodation and food services growth eased to 5.6% (from 6.1%), due to the base effect and capacity constraints following a period of strong expansion. Meanwhile, the agricultural sector maintained steady growth of 1.2%, although sugarcane production continued to contract, pointing to ongoing structural challenges within the sector.

Financial and insurance activities, along with the information and communication sector, remained key drivers of growth, expanding by 5.5% and 6.0%, respectively, supported by resilient global business activity. Wholesale and retail trade also improved markedly to 4.3% from 2.3% in the previous quarter, reflecting still-positive consumption and tourism-related demand. Meanwhile, manufacturing growth edged up modestly to 1.4%, from 1.1% in Q3, although gains were constrained by competitiveness challenges.

2026 outlook: Heightened uncertainty and external risks

In 2025, GDP grew 3.2%, same as projected in December 2025 by Statistics Mauritius, and slightly above 3.1% estimated by the Bank of Mauritius (BoM). This performance is way below 4.9% recorded in 2024.

In 2026, growth is expected to remain moderate. Although January projections pointed to a 3.4% expansion, supported by robust tourism sector and a recovery in private sector investment, the Middle East conflict has significantly heightened external risks, creating uncertainty regarding trade disruptions and rising global commodity prices.

In this context, growth is now projected at around 3.0% under a baseline scenario by Statistics Mauritius, assuming the conflict remains contained. Under a more adverse scenario, where the conflict persists and intensifies through 2026, growth could slow further to around 2.3%, reflecting pressures from higher fuel and input costs (such as fertilisers, gas, raw materials and airfares), potential supply disruptions, with spillovers to key sectors including tourism, construction, and agriculture.

We believe the downside risks to our outlook are elevated. Ongoing fiscal and inflationary pressures are likely to constrain public investment and limit the scope for expenditure-led support to growth. At the same time, private sector investment is expected to remain subdued amid high borrowing costs and a softer real estate market, suggesting continued weakness in construction activity.

Further, Mauritius remains vulnerable to external shocks, particularly higher oil prices, impacting inflation. Such pressures could weigh on household purchasing power and dampen consumption. Consequently, the growth outlook is expected to remain modest, with risks tilted to the downside.

Tourism momentum moderates in March as external headwinds intensify

Growth in tourist arrivals moderated sharply in March 2026, signalling a loss of momentum after a strong start to the year. After recording robust 8% YoY growth in January and 12% in February, tourist arrivals increased by only 1.3% YoY to 114,924 in March. As a result, cumulative tourist arrivals in Q1 2026 reached 348,445, up 6.8% YoY, indicating that the slowdown in March partially offset the strong gains seen earlier in the quarter.

Tourism earnings, however, remained strong through February, reflecting both higher arrivals and increased per capita spending. Gross tourism receipts rose 29% YoY to MUR 9.3 billion in February 2026, while cumulative tourism earnings for January-February 2026 reached MUR 20.6 billion, representing a 30.6% YoY increase. This points to continued pricing power and resilient spending patterns, despite emerging pressures on arrival growth. The deceleration in arrivals in March reflects mounting external headwinds, particularly elevated geopolitical risks in the Middle East. Ongoing airspace disruptions, most notably affecting Emirates Airlines via Dubai, a key transit hub for Mauritius, have weighed on travel flows. In addition, rising fuel prices and supply?related uncertainties have put upward pressure on airfares, dampening travel demand. While enhanced connectivity, higher airline capacity, and sustained promotional efforts supported strong YoY growth early in the year, these factors appear increasingly challenged as cost pressures and logistical disruptions intensify.

Headline inflation eases, but core inflation stays sticky

Headline inflation eased to 2.7% YoY in March 2026, from 3.5% in February, confirming a continued moderation in price pressures. The deceleration was primarily driven by the ‘food and non-alcoholic beverages’ category, where inflation slowed by 3%. Downward pressure was also observed in the ‘restaurant and accommodation services’ category, which declined by 0.7%. In March, core inflation was unchanged at 5.5% compared with February.

In 2026, inflation is expected to exceed the BoM’s pre-crisis forecast of 3.6%, driven by heightened external price pressures stemming from the Middle East crisis and the effective disruption of shipping through the Strait of Hormuz, a key artery for global oil and gas trade. This disruption has pushed up global crude oil, gas and refined fuel prices, which is of particular concern for Mauritius given its status as a small, import?dependent economy and a net energy importer (energy prices have a CPI weight of 12%).

Higher international energy prices are set to drive up domestic fuel and electricity generation costs. Concurrently, surging freight and insurance premiums linked to rerouting, longer transit times, and elevated war?risk cover are expected to raise the landed cost of imports across the board. These pressures are expected to spill over into food inflation, as higher fuel, fertiliser, and gas prices raise agricultural production and processing costs, compounded by increased logistics expenses for imported food items.

Trade outlook faces heightened external headwinds

In January 2026, Mauritius recorded a narrower merchandise trade deficit of MUR 12.8 billion compared with MUR 17.2 billion in January 2025. This improvement reflects a 1.9% YoY increase in exports coupled with a 16.5% contraction in imports.

Export performance in January was underpinned by a strong 51% YoY increase in the ‘food and live animals’ category, providing the key trigger to overall export growth. This improvement was complemented by a marked expansion in exports to key markets. Exports to the United States rose sharply to MUR 805 million, from MUR 223 million in January 2025, reflecting front?loading of shipments ahead of the renewal of the African Growth and Opportunity Act (AGOA) in February 2026. Over the same period, exports to the United Kingdom increased substantially to MUR 843 million, from MUR 507 million a year earlier.

The 16.5% YoY contraction in imports was driven by a pronounced decline in the manufactured goods1 category, which fell by 28.2% because of a marked reduction in vehicles imports, alongside a further fall in imports of mineral fuels, lubricants and related materials (?15.6%). These declines point to lower demand for industrial inputs and favourable price or volume effects in energy imports. However, the overall contraction in imports was partially offset by a 5.9% rise in food and live animal imports.

The government projects Mauritius’ trade position to remain broadly stable in 2026 (March 2026 estimates have incorporated the effects of the Middle East conflict). Total exports are forecast to increase a modest 3.6% to around MUR 501 billion. Imports are expected to edge up by 3.2% to about MUR 574 billion. As a result, the trade deficit is projected to remain broadly unchanged at around MUR 73.5 billion in 2026, compared with MUR 73.4 billion in 2025, reflecting similar growth dynamics in both exports and imports.

Notwithstanding this baseline projection, the trade balance could deteriorate further in 2026, reflecting heightened external cost pressures stemming from the escalation of the Middle East conflict. Disruptions to energy and shipping routes are expected to significantly increase import prices, particularly for fuel, freight, insurance and other energy?intensive inputs, given Mauritius’ high dependence on imports. The high cost could push import values well above the current projections, even in the absence of strong growth in import volumes. While exports may benefit from continued access to preferential markets, most notably under the extension of the AGOA until December 2026 (which supports textile and apparel exports to the US), higher global transport costs and supply?chain disruptions could weigh on export expansion.

Reserves position remains resilient

Mauritius’ gross official international reserves declined to MUR 463 billion (USD 9.8 billion) in March 2026 from MUR 486.2 billion (USD 10.4 billion) in February 2026. Resultantly, import cover eased to 13.6 months in March from 14.3 months in February.

In March 2026, the Mauritian Rupee (MUR) averaged 47.1 against the US Dollar (USD), depreciating by 1.3% from February, amid heightened global uncertainties linked to ongoing geopolitical tensions. Over the past three months (January to March), the MUR has also depreciated by 1.3%.

The MUR is likely to face renewed depreciation pressure, as higher import costs linked to elevated global energy prices, freight, and insurance charges increase demand for foreign currency. While export earnings and service inflows may continue to provide partial support, these are unlikely to fully offset the expected rise in the import bill.

Above views are of the author and not of the website kindly read disclaimer

.jpg)