Maize Report on 20th Apr 2026 by Kedia Advisory

Conclusion - 20 February 2026

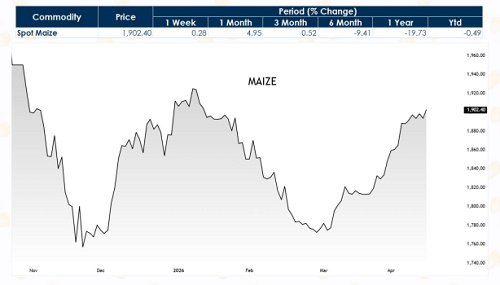

Price Performance: Maize prices corrected nearly 6% over the past month amid heavy rabi arrivals and improved acreage expansion. Arrivals during Jan–Feb 2026 surged 62% YoY to 19.61 lakh tonnes, pressuring spot markets. However, the decline appears largely supply-driven rather than demand destruction, suggesting downside may moderate once peak arrivals taper.

Domestic Supply & Production: As per 1?? Advance Estimates, maize production for 2025–26 is projected at 283.03 lakh tonnes, up over 14% YoY, reflecting improved yields and acreage. Rabi sowing increased 30.08% to 0.68 lakh hectares. Higher output strengthens domestic availability, potentially capping sharp rallies unless demand absorption accelerates meaningfully in coming quarters.

Ethanol Diversion & Domestic Demand: Maize diversion toward ethanol blending is projected to rise 68% to 13.3 MMT in 2025, significantly tightening free-market surplus. Additionally, the poultry industry’s 8–10% annual growth ensures structurally strong feed demand. While sugarcane-based ethanol relaxation trimmed near-term offtake, structural biofuel blending targets remain supportive over the medium term.

Global Trade & Stock Dynamics: US export commitments are up 37% YoY, reflecting strong global appetite, while WASDE lowered global corn stocks to 289 MMT. However, IGC projects ending stocks rising to 305 MMT, a four-year high. Record Chinese production at 301 MMT and higher Ukraine output could offset weather risks, keeping global sentiment balanced.

Technical Outlook: Technically, weekly RSI dropped below 28, indicating oversold territory and potential rebound. Volatility indicators suggest exhaustion of recent selling pressure. MACD remains weak but flattening, hinting at base formation. Harmonic structure supports recovery from lower bands, provided prices sustain above recent swing support zones

Conclusion - 23 March 2026

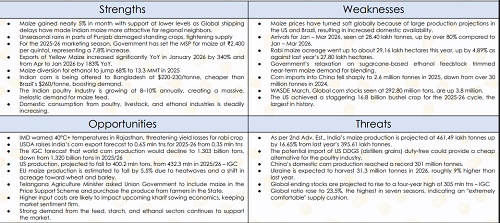

rice Performance: Maize prices have shown resilience, gaining over 1.60% in the last month, supported by strong buying interest at lower levels. Global shipping disruptions have improved export competitiveness, stabilizing domestic prices. However, upside momentum remains capped due to heavy arrivals (26.14 lakh tonnes, up 66% YoY) and higher rabi acreage, limiting sharp price appreciation.

Demand & Exports: Export demand remains a key bullish driver, with Yellow maize exports rising 340% YoY in January 2026 and 183% YoY during Apr–Jan. Competitive pricing ($220–230/tonne vs Brazil’s $260) has strengthened regional demand. Additionally, USDA raised India’s export forecast to 0.65 MMT from 0.35 MMT, supporting domestic price stability.

Ethanol & Domestic Consumption: Structural demand is improving as maize diversion for ethanol is projected to rise 68% to 13.3 MMT, supporting long-term consumption. The poultry sector’s steady 8–10% annual growth further reinforces demand. However, government relaxation on sugarcane-based ethanol feedstock has temporarily reduced maize demand, creating short-term pressure.

Supply & Global Balance: Supply-side pressures persist with production estimated at 461.49 lakh tonnes (+6.31% YoY) and higher sowing at 29.16 lakh hectares (+4.89%). Globally, rising stocks (292.8 million tonnes, +3.8 million) and China’s reduced imports (2.6 MMT vs 30 MMT) weigh on sentiment, though weather risks and global output cuts offer partial support.

Technical Outlook: Technically, maize shows early recovery signals with a Bullish Harmonic Pattern formation and RSI near 35, indicating oversold conditions. This suggests potential for short-term rebound. However, elevated arrivals and supply pressure may cap rallies. Momentum indicators remain mixed, implying a gradual recovery rather than a sharp uptrend.

Performance

Highlights

* Maize prices gained nearly 5% monthly supported by lower-level buying.

* Shipping delays made Indian maize more competitive for regional export markets.

* Unseasonal rains in Punjab damaged crops, tightening short-term domestic supply.

* Government raised maize MSP to ?2,400 per quintal for 2025-26.

* Maize exports surged 340% in January and 183% during Apr–Jan period.

* Ethanol demand expected to rise 68%, consuming 13.3 MMT maize.

* Indian maize offered cheaper than Brazil, boosting demand from Bangladesh.

* Poultry sector growth of 8–10% annually supports steady maize demand.

* Domestic demand from feed, ethanol, and starch industries remains strong.

* IMD warns extreme heat above 40°C may impact rabi maize yields.

* USDA raised India’s maize export forecast to 0.65 million tonnes.

* Global corn production expected to decline, supporting overall price sentiment.

* EU maize output projected lower due to heatwaves and acreage shifts.

* Rabi maize acreage increased 4.89% to 29.16 lakh hectares.

* Arrivals during Jan–Mar 2026 surged over 80%, increasing supply pressure.

* Government ethanol policy changes reduced short-term maize demand for blending.

* India maize production projected higher at 461.49 lakh tonnes this season.

Above views are of the author and not of the website kindly read disclaimer