India Strategy : Beyond the AI Rally: The Great Rotation by Motilal Oswal Financial Services Ltd

Over the past two years, the Indian market has experienced a phase of heightened volatility, prolonged consolidation, and time correction, driven by uncertainties related to the US trade tariff war, evolving domestic policy dynamics, energy price shocks, and supply disruptions stemming from the West Asia conflict. India has largely borne the brunt of these geopolitical shocks. It initially faced a higher US tariff burden and subsequently grappled with elevated energy prices, which weighed on key macroeconomic indicators. Meanwhile, corporate earnings growth moderated sharply in FY26, with the Nifty-50 registering a modest 5% EPS growth (following a 16%+ CAGR during FY20-25) after a period of significant market rerating that left broader market valuations stretched. The combination of geopolitical uncertainties, moderating earnings growth, and elevated valuations kept FII sentiment toward India firmly negative, resulting in cumulative outflows of USD60b over the past 21 months since the Indian market peak in Sep’24. However, record DII inflows (USD162b over the same period) and resilient retail participation (average monthly SIP inflows of ~USD3b) emerged as a powerful counterbalance, comfortably absorbing foreign selling. As a result, despite sustained FII outflows and multiple external shocks, the Nifty’s peak-to-trough correction remained limited to ~15% during the past two years.

Sharp underperformance and valuations favor mean reversion

* Nearly two years of range-bound performance in Indian equities and a strong rally in global markets have widened the performance gap to near-historic levels. India's cumulative outperformance compared to the MSCI EM Index of +10% (between Jun'21 and the Sep'24 peak) has swung to an underperformance of -40% (between the Sep'24 peak and Jun'26). Simultaneously, India's valuation premium over EM has compressed to a historic low of 18% in Jun'26, significantly below its long-term average of 73% and CY22 peak of 147%.

* India's underperformance, following its status as one of the world's bestperforming equity markets between 2020 and 2024, has been difficult to reconcile with its strong underlying fundamentals. A key factor has been the sharp global capital rotation toward a narrow group of AI-driven Big Tech companies and related technology beneficiaries, which has left non-AI markets, such as India, bearing the brunt of this shift.

* While the AI-driven rally may persist, the unprecedented concentration of capital among a limited set of beneficiaries over a short period appears to present greater risks than opportunities. In contrast, India's prolonged period of relative underperformance has led to more attractive valuations and positioning. Any broadening of global market leadership or rotation away from AI-centric trades toward a wider range of sectors and markets is likely to serve as a meaningful tailwind for Indian equities

Constructive macro; selective opportunities

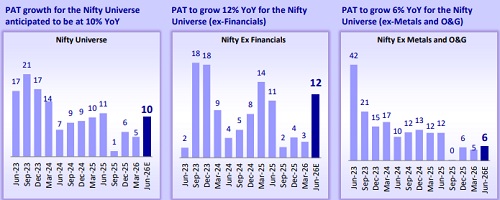

* Today, the backdrop has turned considerably more constructive. Geopolitical concerns have mellowed, energy prices have eased from their peaks, and global oil trade has largely normalized. The earnings outlook has strengthened meaningfully, with corporate earnings expected to clock ~15% CAGR over FY26– 28, despite temporary pressure in 1QFY27. Meanwhile, valuations have corrected trading below their historical averages. Additionally, India's valuation premium compared to global peers has compressed to near historical lows. After nearly two years of consolidation and underperforming most global markets over the past year, Indian equities appear to have largely priced in the key downside risks.

* Despite an improving macroeconomic backdrop, the market remains. fundamentally bottom-up, with growth-oriented themes and companies scaling up expected to be the key beneficiaries. As leadership becomes increasingly stockspecific, company rankings are likely to evolve meaningfully over the next 3–5 years.

* Companies that successfully gain scale and strengthen their competitive positioning are expected to command larger market caps and, in turn, higher portfolio weights. Accordingly, our portfolio reflects this divergence in growth prospects, remaining underweight in sectors with a muted earnings outlook while overweight in businesses and themes where the growth trajectory continues to strengthen. We expect the market to disproportionately reward superior growth.

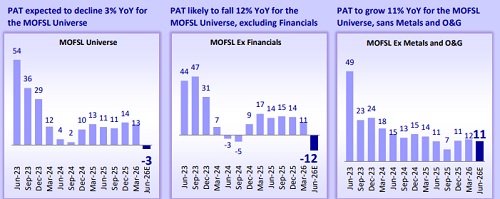

OMC weakness offsets strength in Financials and Metals

* Against this backdrop, we present our views on the upcoming 1QFY27 earnings season, which will reflect the anticipated impact of the West Asia crisis and higher energy prices. We expect a modest 3% decline in earnings across the MOFSL universe, primarily weighed down by OMCs affected by elevated crude prices.

* Excluding OMCs, PAT growth is projected at 14% YoY. The MOFSL large- and mid-cap universes are expected to report PAT declines of 2% YoY and 14% YoY, respectively, primarily due to losses in the OMC segment within the O&G sector. Conversely, the MOFSL small-cap universe is expected to post a healthy 20% YoY earnings growth, supported by a favorable base (vs. a 1% YoY decline in 1QFY26) and driven largely by Financials.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412