India`s Valuations Ease from Peaks, Bringing EM and World Multiples Closer: Equirus Securities

Financial services firm Equirus Securities has released a press note on India Equity Strategy. As per the note, Indian equity markets’ valuations have eased from peak due to the latest correction, bringing EM and the World multiples closer. The Nifty is expected to trade between 18x-22x PE; similar to post Covid. Sectors like Auto, Banks, Capital Markets, FMCG, Internet Platforms and Oil & Gas are Over Weight.The earnings growth is likely to return from H2FY26 onwards. Stable monetary policy, India’s valuation premium has become reasonable within EM due to the recent correction amid AI mania.

Equirus Securities is Overweight on sectors like Auto, Banks, Capital Markets, FMCG, Internet Platforms. Underweight on Building Materials, Industrials and Defense, Real estate, Textile and Logistics and Equal Weight on Cement, Chemials, Consumer Durables, EMS, Infra, IT Services, Metals and Mining, NBFCs, Healthcare and Retail.

India Anti-AI trade: The market benefits from structural stability due to robust domestic flows (strong SIP inflows sustained a 27% CAGR). DII ownership has risen to 18.6%, structurally absorbing FII selling, whose ownership has slipped to 16.9%. Within EM, South Korea, Taiwan outperformed as FIIs chased AI trades. India notably doesn’t have many direct/indirect play resulting into underperformance.

Earnings Momentum a key positive trigger: Earnings growth in the Nifty 50 is expected to improve meaningfully in CY26–CY27 (17–14%). Given that valuation upside from multiple expansion is constrained due to elevated prices, future returns must be driven by earnings delivery. Although consensus EPS for CY25 was cut heavily (-13%), the current data points to an earnings surprise cycle that materially revises EPS up as the more plausible positive trigger for benchmarks to materially re-rate upward, rather than a renewed liquidity or flow impulse.

Valuation Risks Persist: While large-cap valuations have moderated from their post-COVID highs, they remain above historical averages. Small-cap valuations are highly stretched, with the Small/Large forward P/E ratio at approximately 1.25x, significantly above the long-term average of 0.9x, making them vulnerable to reversals.

The valuations of the Indian markets have moderated from peaks but remain elevated vs Pre-COVID and Past Cycles. Valuations have cooled from the Sep-24 peak but remain elevated — the share of NSE-500 stocks trading >50x PE is 36%, sharply higherthan 16% pre-COVID, though lower than the 50% seen at the Sep-24 high. Lower buckets (10–20x, 20–30x) have normalised versus peak levels

but still sit below pre-COVID distributions.

Compared with prior market highs (Aug-18, Feb-15, Dec-10), today’s skew is clearly richer, especially in the >30x segments, where thecombined weight (30–40x + 40–50x + >50x) remains materially higher than historical cycles. This indicates valuation froth is off the top, but themarket is still priced well above long-term norms.Risk-reward favours large caps and quality compounders where valuations are closer to historical bands, while mid/smallcaps and >50x names remain vulnerable to any earnings disappointment. Broader re-rating from here requires earnings upgrades, not furthermultiple expansion.

Key Tailwinds (Oil & Rural): India benefits from stable, softer Brent crude prices (US$ 63–70/bbl range), which are margin-accretive for multiple sectors (e.g., OMCs, chemicals, transport). Additionally, rural demand is gathering momentum, supported by high reservoir storage levels and improving sentiment.

External Headwinds: The primary external risk is the U.S. tariff shock, which has caused India’s exports to the U.S. to drop 40% since May 2025, significantly affecting labour-intensive sectors like textiles. However, diversification of exports to non-US markets is helping to cushion the disruption.

India’s 5-year market return tops global peers; strong ROE and MSCI outperformance post-COVID underpin long-term strength, while a year of correction has made valuations somewhat more reasonable

Monetary Easing Cycle: With inflation cooling sharply to ~1–2% YoY, RBI has already delivered a cumulative 100 bps of rate cuts, which has helped ease system liquidity and stimulate an early pickup in credit growth. The persistence of low inflation continues to provide the RBI additional room to cut rates further, keeping monetary conditions supportive for growth and asset re-pricing.

Nifty 50 Earning Revisions

The Consensus EPS for CY25 has been cut heavily (~-13%); that implies much of market ‘good news’ on volumes/margins must be re-earnedthrough actual company results. Valuation upside from multiple expansion is constrained unless earnings revisions reverse. The cuts moderate through CY26–CY28 but remain negative in aggregate. This implies the next two years are likely to be about earnings recovery(or further disappointment). The benchmarks will likely be constrained: to materially re-rate upward we need either (a) an earnings surprise cycle that materially revises EPS up,or (b) a renewed liquidity/flow impulse. Current data points to earnings surprises as the more plausible positive trigger.

Market Cap Performance Divergence – Mid Caps outperformed Large & Small Caps

The Post-COVID the rally has been breadth-led: mid& small caps outpaced large caps on arebased basis, with the sharpest cyclic gains inFY17, FY22 and FY24 driven by selectiveearnings recoveries, rising retail participationand expanding domestic demand.That said, small-cap valuations are now

stretched — the Nifty Smallcap 100 sitsmaterially above its 10-yr +1σ — leaving thesegment highly vulnerable to risk-off reversalsdespite strong past returns.Mid caps trade above long-run multiples too,but earnings visibility and balance-sheet repairin many pockets provide a more defensible

upside case than the small-cap cohort.Large caps have delivered lower absolutereturns but offer better stability, lowervolatility and deeper FPI interest, makingthem the preferred anchor while

macro/earnings clarity is lacking. Equirus Securities’ stance would beto avoid broad small-cap exposure, beselectively constructive on mid caps with clearearnings/sector catalysts, and retain large-capoverweight for risk management until valuationsand earnings converge.

Small-Cap Valuations at Multi-Year Extremes

The Small-cap valuations remain the most stretched across the curve, with theSmall/Large fwd P/E at ~1.25x, far above the long-term average of 0.9x(+2.2σ) and close to previous peaks—signalling that recent performance hasbeen dominated by multiple expansion rather than earnings delivery. The

Small/Mid fwd P/E (~0.89x) has eased from extreme highs but still sitsmarginally above its long-term mean. Mid-caps, while still expensive, screenmore defensible: the Mid/Large fwd P/E (~1.4x) remains elevated but belowthe euphoric 2024 zone, and mid-cap premiums today are increasinglysupported by earnings catch-up rather than pure re-rating. Net-net, mid-capsappear stretched but fundamentally anchored, while small-caps are mostvulnerable to mean reversion if earnings revisions soften or domestic flowsweaken.

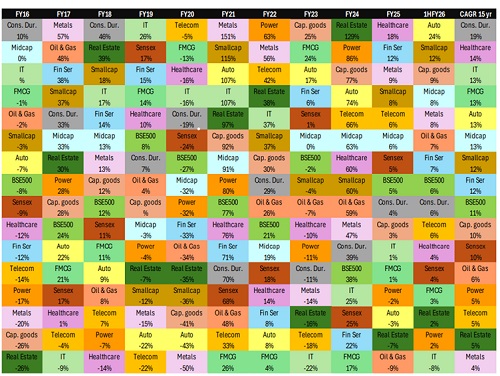

Annual Sectoral Performance Snapshot

The sector rotation over the past decade has been highlycyclical, with leaders shifting each year — Metals, RealEstate, Smallcaps, Power, and Capital Goods all takingturns at the top — underscoring the dominance ofmacro, liquidity and policy cycles.The recent phase (FY23–1HFY26) marks a clear shifttoward earnings-backed leadership. FY24 strengthcame from Real Estate, Power, Cap Goods and Autos onthe back of domestic demand and the capex upcycle.FY25 saw narrower leadership, with Healthcare, Metals,Financials and Cap Goods delivering steady,fundamentally supported gains even as market breadthsoftened.

In 1HFY26, performance remained anchored infundamentals: Autos, Healthcare, Midcaps and selectivecyclicals led on earnings delivery, while smallcap gainswere more liquidity-driven. FMCG and IT improved butstayed mid-pack due to slower demand recovery andelevated valuations.Across 15 years, Consumer Durables, Healthcare, IT,FMCG and Financials remain the most consistentcompounders, while Metals, Power, Real Estate andsmallcaps continue to display boom–bust cyclicality.Overall, the market has transitioned from the broadliquidity-driven re-rating of FY21–22 to a moreearnings-anchored and capex-led regime, implyingcontinued dispersion ahead — with quality cyclicals andstrong midcaps better placed than valuation-stretchedsmallcaps.

Sector Valuation Snapshot – Relative Stretch vs Historical Averages

Significantly Above Long-Term Average

* Capital Goods (41.6x vs 3Y avg 35.0x, 10Y avg 26.3x) – Trading close to cycle highs; strong capex and manufacturing optimism priced in with limitedvaluation cushion.

* Consumer Durables (53.2x vs 3Y avg 52.8x, 10Y avg 40.7x) – Near 3-year peaks; premium valuations hinge on continued premiumisation anddiscretionary demand resilience.

* Healthcare (32.2x vs 3Y avg 29.2x, 10Y avg 25.0x) – Near upper historical band; market pricing strong domestic demand and stable margin recoveryahead.

* Realty (32.1x vs 3Y avg 37.0x, 10Y avg 28.7x) – Below the Sep-24 peak but elevated vs long-term average, supported by strong housing cycle andpre-sales momentum.

At or Above Mid-Cycle Valuation:

* Auto (23.9x vs 3Y avg 22.0x, 10Y avg 20.3x) – In line with 3-year trend; valuations supported by margin recovery and improving PV/CV cycle visibility.

* FMCG (32.4x vs 3Y avg 34.9x, 10Y avg 29.4x) – Slightly below the 3-year average but still rich; requires sustained volume recovery to justify multiples.

* Financial Services (16.6x vs 3Y avg 15.6x, 10Y avg 16.9x) – Around mid-cycle levels; reasonable valuations supported by diversified financial earningsgrowth.

Near or Below Long-Term Average (Potential Value Zones):

* Banks (14.6x vs 3Y avg 13.4x, 10Y avg 15.8x) – Slightly above 3Y but below 10Y mean; healthy credit growth and stable asset quality offer relativevalue.

* IT (23.5x vs 3Y avg 24.7x, 10Y avg 21.1x) – Below recent peaks; valuations consolidating amid muted global tech spending and slower dealconversions.

* Metals (14.4x vs 3Y avg 11.5x, 10Y avg 10.3x) – High vs history but still cyclical; near-term pricing strength baked in, earnings visibility key.

* Oil & Gas (10.0x vs 3Y avg 9.2x, 10Y avg 9.5x) – Fairly priced, close to long-term average; policy risks and regulated segments cap re-rating potential.

* Power (20.7x vs 3Y avg 21.6x, 10Y avg 15.7x) – Slightly below 3Y avg but well above 10Y mean; reflects strong demand momentum and tariffvisibility.

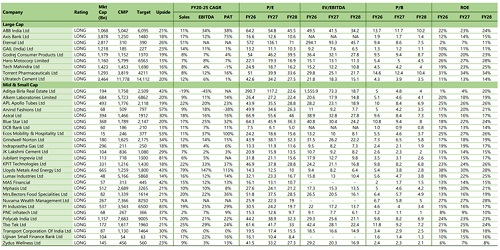

Stock picks

Equirus Securities has listed their top picks in Large, mid and small cap segment. ABB India, Axis Bank and Eternal are among top picks in largecaps, Aditya Birla Real Estate, Alkem Labs, APL Apollo Tubes are top picks in mid and small caps.

Above views are of the author and not of the website kindly read disclaimer