India`s Mutual Fund Investors Are Chasing the Wrong Returns: Vallum Capital

According to Vallum Capital’s Monthly Macro Grid Chartbook report, across asset classes, India's mutual fund industry held firm at Rs 81.58 lakh crore in assets as of May 31, 2026, and equity funds recorded their 63rd consecutive month of net positive inflows — a streak that has survived elections, rate cycles, and now global commodity shocks. SIP contributions hit Rs 30,954 crore for the month, 16% higher than a year ago, with 9.64 crore active accounts.

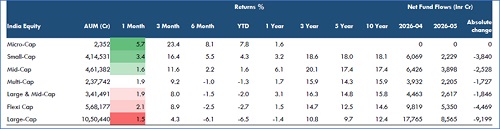

Cap-Wise: The Highest-Returning Funds Got the Least Money

(all Returns fig are average of their category)

Within domestic equity, May produced one of the clearest disconnects between returns and flows this year. Micro-cap funds were this month's best performers, gaining 5.7%. Small-cap funds returned 3.4%, the second-best showing across all cap categories, and drew Rs 2,229 crore. Mid-cap funds gained 1.6% and collected Rs3,898 crore.

Large-cap funds, however, returned just 1.5% the weakest monthly return in the cap-wise pack and pulled in Rs 8,565 crore, nearly four times what small-caps received and more than double mid-caps. Flexi-cap funds, which delivered 2.1%, drew Rs 5,350 crore, while Large & Mid-cap funds collected Rs 2,617 crore at 1.9%.

The pattern is unambiguous: the lower the return, the more flows the category received. This is not investor irrationality it is SIP mathematics. Monthly standing instructions on large-cap and flexi-cap index trackers mechanically route the bulk of retail savings toward the largest, most liquid end of the market, regardless of where monthly performance was generated. The result is that India's biggest fund category by AUM large-cap, at over Rs 10.5 lakh crore continues to accumulate capital even in months where smaller, higher-performing categories are left undersubscribed.

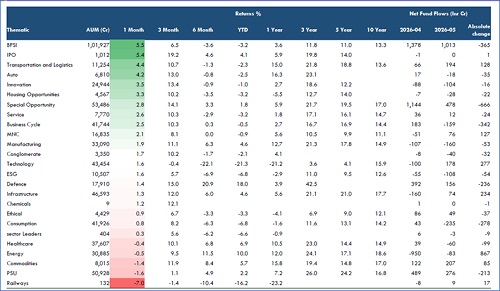

Thematic Funds: Bets in Banking.

(total Thematic funds universe market cap is around 5.99 Lakh Cr)

Sectoral and thematic funds told a more nuanced story in May. BFSI funds led the entire thematic universe, returning 5.5% for the month and attracting Rs 1,013 crore. The behaviour inside banking was even more instructive: PSU Bank funds gained 6.9% and collected Net Inflow of Rs 436 crore; Private Bank funds gained 6.5% and collected Rs 329 crore — together drawing Rs 765 crore. Broad-basket Bank funds returned the same 6.5% as private banks and simultaneously saw Rs 421 crore in redemption. Investors are actively rewarding targeted exposure and penalising category breadth at identical return levels.

Transportation and Logistics funds gained 4.4% and drew Rs 194 crore. Auto funds gained 4.2% but saw a small outflow of Rs 18 crore, suggesting the sector's May bounce was not trusted as durable.

Technology funds down sharply over the past year returned 1.6% in May and attracted Rs 178 crore, reversing a Rs 100 crore outflow from April. The buying came specifically through passive IT index trackers (Rs 90 crore from IT Index funds) and large Technology Broad funds (Rs 185 crore), while Digital India thematic funds, which actually returned a better 2.3%, saw Rs 101 crore in redemptions. Investors are dip-buying tech through index vehicles while simultaneously exiting thematic wrappers a deliberate structural preference.

Consumption funds were the month's cleanest reversal story in the wrong direction. Returning just 0.8% for the month, the category bled Rs235 crore in net outflows led by Consumption Broad funds, which alone accounted for Rs 207 crore in redemptions. No sub-category within consumption held positive flows.

Defence funds continued to attract steady Net Inflow at Rs 156 crore. Railways funds posted the month's steepest sectoral loss at -7%, with effectively no buyers in sight.

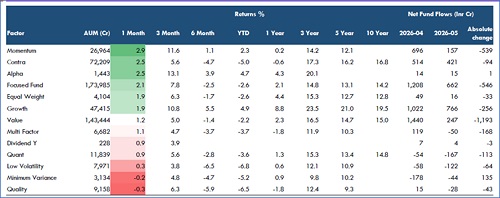

Factor Funds: Growth and Contra Lead; Defensive Factors Are Being Sold

Factor-based funds — now a Rs 5 lakh crore category — showed May's most counterintuitive flows pattern. Momentum funds posted the best monthly return across all factors at 2.9%, yet drew only Rs 157 crore. Growth-style funds returned 1.9% and led the category in flows at Rs 766 crore. Focused funds drew Rs 662 crore at 2.1%, and Contra funds drew Rs 421 crore.

The real signal: Quality funds returned -0.3% for the month and saw Rs 28 crore in outflows. Low Volatility funds returned 0.3% and bled Rs 122 crore. In a month of genuine global uncertainty — West Asia conflict, FII selling of Rs 32,963 crore, commodity price swings India's factor investors sold their traditional defensive allocations and held their growth-oriented ones. Whether this reflects confidence or complacency will likely only be answered in the months ahead.

On the other side of FII selling of Rs 32,963 crore, domestic institutional investors bought Rs 82,165 crore worth of equities in May, providing the market's stabilising counterweight. Debt funds saw Rs 96,949 crore in net outflows — a large headline number that reflects the unwinding of April's record Rs 2,47,490 crore inflow, which was driven by institutions parking short-term treasury liquidity around the fiscal year end. The reversal was always expected and is technical, not structural.

India has 27.65 crore mutual fund investor accounts today up from 10.04 crore just six years ago. Its SIP infrastructure now generates nearly Rs 31,000 crore every month without flinching. What May 2026 confirms is that the inflow machine is built and running. The open question is allocation quality: the funds that earned the most in May got the least money, the funds that earned the least got the most, and the only categories being actively bought with discretion banking specifics, technology passives, infrastructure recovery plays are those where informed capital is operating alongside, not inside, the SIP stream.

The resilience of India's retail investor is no longer in question. What May 2026 reveals, instead, is a sharper question: where is the money actually going — and is it going to the right place?

Above views are of the author and not of the website kindly read disclaimer

.jpg)

Tag News

Quote on the AMFI data for July 2026 Nitin Agrawal, CEO, Mutual Funds, InCred Money