Global Headwinds Intensify - Can India Inc Stay the Course? by CareEdge Ratings

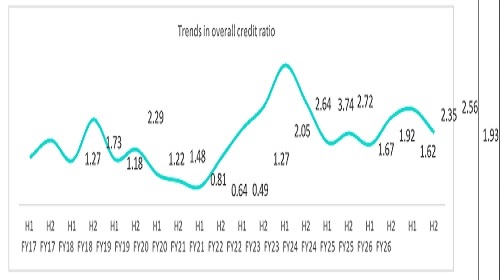

According to CareEdge Ratings Credit Ratio, which measures the proportion of rating upgrades to downgrades, stood at 1.93 times in the second half of fiscal 2026, lower than 2.56 times observed in the first half. During this period, 363 entities were upgraded and 188 were downgraded. While the credit ratio remains above the 10-year average of 1.55, the moderation suggests early signs of stress amid a more challenging environment.

The downgrade rate, at 7%, remains below the long-term average of 10%; however, the moderation in upgrades, from the long-term average of 15% to 13% in the current period, suggests that improvement in credit profiles is becoming more selective. Nevertheless, reaffirmations remained high at 80%, indicating that the bulk of the rated universe continues to hold its ground even as the external environment grows more complex.

This relative stability is underpinned by the continuing corporate deleveraging trend, as also highlighted in our Oct. 2025 edition of the Credit Quality Assessment. Total gearing1 remained low at 0.50 times as of Mar. 31, 2025, compared with 1.04 times as of Mar. 31, 2016, underscoring the structural strength of India Inc.'s balance sheets going into this period of heightened uncertainty.

Sachin Gupta, Executive Director and Chief Rating Officer, CareEdge Ratings, commented on the evolving economic landscape, stating, "The escalation of the West Asia conflict has added a new and potent layer of uncertainty. Given India's high dependence on energy imports, a prolonged conflict situation could have cascading effects — fuelling inflation, widening the current account deficit, exerting pressure on fiscal balances, and weighing on growth. In this context, CareEdge estimates that if crude oil were to average USD 100 per barrel in FY2027, GDP growth could moderate to 6.5%, while inflation may rise to 5.1–5.3%.” He further added, “While domestic policy measures and relatively stronger corporate balance sheets provide some cushion, the critical question is whether these domestic levers will be sufficient to keep credit quality on course if the global environment deteriorates further. For now, the answer leans towards yes — but the margin for comfort is narrowing.”

Amidst the emerging geo-political environment, the credit ratio for the manufacturing and services sector improved to 2.06 times in H2FY26, up from 1.72 times in H1FY26. Ranjan Sharma, Senior Director, CareEdge Ratings (Corporate Ratings), noted, "The upgrades during H2FY26 were fairly broad-based, with key sectors driving the momentum being pharmaceuticals, auto ancillaries, real estate leasing, mid-sized entities in capital goods and agricultural food products, along with hospitality and healthcare in the services space. On the flipside, sectors bearing the brunt of downgrades were small-sized commodity trading and distribution entities, seafood exporters, and paper and paper product companies. The chemical sector continued to face pressure from the twin forces of Chinese dumping and weak global demand. Looking ahead, the sudden outbreak of conflict in West Asia has introduced sectoral vulnerabilities that did not exist around a month ago. Industries like airlines, ceramics, chemicals, glass, fertilizers, oil marketing companies, basmati rice exporters, packaging, tyres, synthetic textiles, gas distribution, cement, paints, semiconductor & electronics, auto ancillaries, and hospitality — face earnings headwinds if the West Asia conflict prolongs. MSMEs, in general, are likely to be the most vulnerable to these shocks. However, Corporate India's deleveraged balance sheets, are expected to provide some cushion in the near term.”

Turning to infrastructure, the credit ratio normalised to 1.67 times in H2FY26, from the elevated 8.54 times in H1FY26. This normalisation is primarily a reflection of the base effect — H1FY26 had been significantly inflated by a large volume of bulk portfolio rating actions, including ownership changes to stronger sponsors and bulk transfers to Infrastructure Investment Trusts, which were episodic in nature. Rajashree Murkute, Senior Director, CareEdge Ratings (Infrastructure Ratings), observed, "The normalisation in infrastructure's credit ratio should not be read as a deterioration — the fundamentals of the sector remain sound. In H2FY26, upgrades were driven by the commissioning of projects, healthy payment cycles from state & central utilities, and multiple portfolio transactions involving transfer to financially strong sponsors or InvITs. Downgrades in H2FY26 were attributable to rising non-project debt at select large renewable sponsor holdcos, combined with a lag in operational performance, which also triggered rating actions on linked ratings. For mid-sized EPC players, increased working capital pressures continue to exert pressure on credit profiles. Additionally, the construction sector companies with significant order book exposure to the Middle East are under cautionary lens amid the ongoing geopolitical tensions. That said, at an overall level, the infrastructure sector remains relatively better placed in the current environment, supported by its predominantly domestic revenue profile and relatively stable cash flow visibility. Execution capability and the ability to mobilise long-term equity capital for growth will be the key differentiators in the infrastructure space going forward.”

The credit ratio for Banking, Financial Services, and Insurance (BFSI) sector improved to 2.25 times — up from 2.10 times in H1FY26, marking a recovery from the stress-driven lows of H2FY25. Sanjay Agarwal, Senior Director, CareEdge Ratings (BFSI Ratings), said, “Upgrades in NBFCs were primarily driven by continued improvement in financial performance, improved credit profile of parent entities, and healthy capital infusions leading to better leverage. Banks remained stable throughout the period, with no downgrades in H2FY26. BFSI downgrades remained concentrated in smaller NBFCs and MFIs. Looking ahead, advances growth is expected to remain moderate. While the asset quality deterioration, especially in MFIs and other small ticket loans has abated, headwinds from geopolitical tensions and consequent impact on the overall economy remain the major risk factors."

In summary, the evolving macroeconomic backdrop, marked by intensifying geopolitical tensions and shifting trade dynamics, is beginning to weigh on India Inc.’s credit quality. If the global conflict deepens and trade flows continue to restructure, the resilience of credit profiles will be tested in the months ahead. CareEdge Ratings expects the credit quality outlook to remain cautious, with the overall credit ratio likely to remain range-bound in the near term. While domestic consumption and the structural strength of corporate balance sheets act as anchors, global trade uncertainty, energy scarcity and export sector stress are likely to limit any meaningful improvement in credit quality.

Above views are of the author and not of the website kindly read disclaimer

More News

Economy : Financing Fragility Over Real Fixes by Choice Institutional Equities Ltd