Economic : CPI Inflation : Headline CPI 3.2%; 4% in FY27E if quick end to Iran conflict By Emkay Global Financial Services Ltd

Feb-26 headline inflation ticked up, to 3.2%, driven by moderately higher food inflation (3.4%) as favorable base effects fade. Core CPI was flat at 3.4%, with the pace of precious metals price inflation moderating. As a result, core exprecious metals CPI was flat as well, at 2%. FY27E headline CPI is tracking at 4-4.1%, assuming average Brent price of USD70/bbl with a quick end to the Iran conflict. However, a prolonged crisis would have a significant impact on macro dynamics. While every USD10/bbl rise in crude prices is likely to lead to headline CPI rising by 40bps on annualized basis assuming full pass-through, the final impact is expected to be lower as the government and OMCs will share the burden. The Iran crisis has also created a dilemma for the RBI regarding FX intervention, as sustained intervention will drain domestic liquidity while a hands-off approach risks a speculative downward currency spiral.

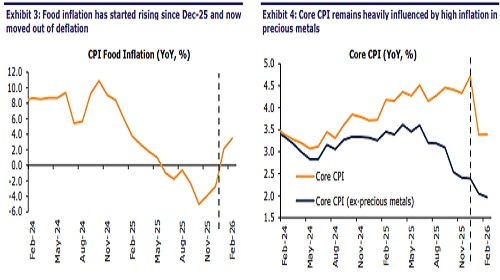

Headline CPI rises to 3.21%, as food inflation picks up Headline CPI inflation rose to 3.21% in Feb-26 (Emkay: 3%; prior: 2.73%), with food inflation also picking up mildly (F&B CPI: 3.4% YoY) as favorable base effects fade. However, monthly momentum declined to 0.1% MoM (vs 0.3% prior), driven by food (-0.2% MoM). Within food, vegetable prices fell MoM (-6%) but have moved into the positive territory on YoY basis (3% YoY). Other significant movers included eggs (-5% MoM), meat (-1% MoM), and fruits and nuts (4% MoM).

Core inflation flat, with moderation in pace of precious metals inflation Core inflation (ex-intoxicants) was flat at 3.4%, with monthly momentum dipping to 0.3% (prior: 0.6%). This is largely attributed to a moderation in the pace of price rises for precious metals, especially silver. Additionally, the new CPI series considers gold and silver jewelry prices rather than those of underlying metals, which will also reduce price volatility for these categories. Gold jewelry prices rose ~5% MoM during the month (vs 8% prior), while silver jewelry prices saw a sharp reduction in the pace of growth (4% MoM vs 35% prior). Ex-personal care (which includes jewelry), other core inflation categories logged subdued monthly momentum at less than 0.2% MoM. As a result, core CPI ex-precious metals saw extremely subdued momentum at 0.1% MoM (2% YoY).

FY27E headline CPI at 4-4.1% in a USD70/bbl Brent scenario We continue to track FY27E headline CPI at 4-4.1% in our base-case scenario of USD70/bbl average Brent crude price (assuming the Iran conflict ends within a month). However, an extended conflict would have a severe impact on the macro dynamics. The eventual fiscal, inflationary, and external balance impact will depend on how the burden is shared between the government (via excise duty cuts and higher fuel subsidies), OMCs and consumers (via fuel price hikes). Assuming full pass-through, headline CPI could be higher by ~40bps on an annualized basis for every USD10/bbl increase in crude oil prices. However, we note that this is unlikely, given that the government and OMCs are likely to absorb some of the pain and cushion consumers to some extent.

Ongoing crisis puts the RBI in a dilemma regarding FX intervention With the Iran crisis persisting longer than anticipated, India’s challenge is likely to quickly evolve from a current account issue to one of capital account. In such an environment, global developments may constrain the RBI’s ability to stabilize the INR through FX intervention, complicating policy trade-offs ahead. Financial stability will therefore no longer play second fiddle in the RBI’s policy function in our view, and may well emerge as the primary focus. While rate easing in April is off the table, the real dilemma for the RBI will be about drawing the line between FX intervention and tolerance. Letting the INR depreciate freely to absorb the shock is not an option in times of stress, as speculation can quickly lead to a slippery slope for the currency. However, sustained and significant unsterilized spot FX intervention would drain domestic liquidity at a time when banking liquidity is seasonally tight, while expanding the heavy net short FX position by intervening in the forward markets will also come at a cost.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354