Economic :Trade Deficit : Deficit falls as precious metal imports dip By Emkay Global Financial Services Ltd

The goods trade deficit fell to USD27bn in Feb-26 (prior: USD35bn), led by a decline in precious metal imports (which though stayed high). Total imports fell 11% MoM while exports were flat. Exports to the US rose 4% MoM, likely helped by the interim India-US trade deal, but remained 7% YoY lower from Sep-25 to Feb-26. While the lower headline US tariff of 10% should help exports ahead, there is risk from an extended Iran crisis. Net services exports remained strong, rising to a record USD23.1bn in Feb-26, though those for Jan-26 were revised down. We maintain FY26E CAD/GDP at 0.9%, with upside potential from betterthan-expected net services exports. For FY27E, a benign Brent scenario of USD70/bbl implies CAD/GDP of 1.3%. However, a scenario analysis of average Brent at USD90/bbl for FY27E implies CAD/GDP widening to 1.9%.

Goods deficit moderates albeit precious metal imports remain high The goods trade deficit reduced to USD27bn (vs USD35bn in Jan-26) but was higher than estimated (Emkay: USD23bn). This was due to a lower-than-estimated moderation in imports (USD63.7bn; -11% MoM), led by gold (USD7.5bn; -38% MoM) and silver (USD1.7bn; -17% MoM). Exports were flat MoM (USD36.6bn), with oil exports falling 9% MoM, while oil imports declined 3% MoM. For 11MFY26, total goods exports are at USD403bn (~2% YoY), while total imports have risen ~9% YoY to USD714bn, even as oil imports remain lower (USD162bn; -3% YoY). As a result, the 11MFY26 goods trade deficit stands at USD311bn (vs USD261bn for the same period last year).

Core exports steady while core imports decline Core imports declined 5% MoM to USD42bn while core exports were flat at USD30.5bn, leading to a fall in the core deficit to USD11.1bn. Core exports over 11MFY26 were at USD326bn (4% YoY), while core imports stood at USD471bn (9% YoY). Notably, trends for tariff-affected sectors for FY26TD remain mixed. Gems and Jewelry exports were down 3%, while Textile exports were down 1%. On the other hand, Marine Products exports continue to see strong growth (15% YoY FYTD). Among major export categories, Electronics (28% YoY for 11MFY26) remains a strong growth performer, followed by Drugs and Pharma (6% YoY) and Engineering Goods (5% YoY).

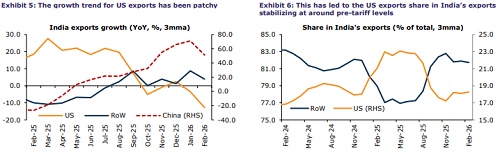

US exports pick up after interim deal; expected to improve going ahead Exports to the US rose 4% MoM (USD6.9bn) and are likely to have been aided by the interim India-US trade deal announcement in early-Feb. RoW exports declined 1% MoM (USD30bn). Exports to the US were up ~4% to USD79bn for FY26TD; however, an unfavorable base is likely to pull down growth for FY26. RoW exports were up ~1% for FY26TD (USD324bn), having risen 4% YoY from Sep-25 to Feb-26. This was led by sharp growth in exports to Spain (68% YoY), China (53%), Hong Kong (34%), Vietnam (30%), and the UAE (10%) post-tariff imposition. While this diversification is welcome, the lower US headline tariffs of 10% going ahead are likely to shift exports back to the US (albeit the Iran crisis puts this at risk).

Services surplus hits a record in Feb-26; Jan-26 sees sharp downward revision Services surplus rose to a record-high of USD21.5bn in Feb-26 from the downwardrevised USD21.5bn in Jan-26 (USD24.3bn earlier). Thus, services surplus for 11MFY26 stood at ~USD201bn, up 18% YoY, with gross services exports (USD388bn) growing 10%. For Feb-26, exports (USD39.5bn) rose 4% MoM while imports (USD16.4bn) dipped 2%. Services exports have been resilient in FY26, helped by GCCs, but are likely to face headwinds in FY27E from a global growth shock if the Iran crisis is protracted.

FY27E CAD/GDP 1.3%, but risk of flaring to 1.9% if average Brent at USD90/bbl We expect 4QFY26E to see an improvement in both CAD and BoP, with CAD/GDP tracking 0.4%, led by moderation in the goods trade deficit and services surplus staying robust. We maintain FY26E CAD/GDP at 0.9%, with some upside potential from strong services surplus. For FY27E, a benign scenario of USD70/bbl for Brent implies CAD/GDP of 1.3%, with BoP deficit at USD15bn. Every USD10/bbl increase in Brent prices is likely to widen the CAD/GDP by ~0.45%, ceteris paribus. However, our scenario analysis of average Brent prices at USD90/bbl implies CAD/GDP widening to 1.9% for FY27E, with BoP deficit worsening to >USD60bn.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354