Debt Monthly Observer by Sneha Pandey, Fund Manager -Fixed Income, Quantum AMC

When the Reserve Bank of India (RBI) announced a fresh FCNR(B) mobilization scheme and concessional swap facility in its June 2026 monetary policy, markets immediately drew parallels with September 2013.

The comparison is understandable.

The last time this toolkit was deployed, India was at the center of the "Fragile Five" episode, alongside Brazil, Indonesia, South Africa and Turkey. A sharply depreciating rupee, record current account deficits and deteriorating investor confidence had placed significant pressure on India's external balance sheet.

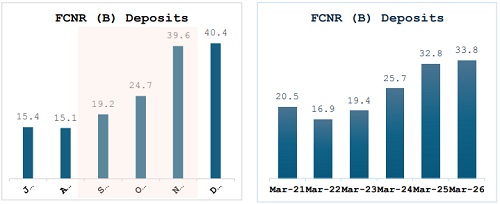

The FCNR(B) programme introduced under Governor Raghuram Rajan eventually mobilized nearly USD 34 billion, helping stabilize the rupee and restore confidence in India's external position.

Yet viewing 2026 as a replay of 2013 misses the bigger story.

The instrument may be the same, but the macroeconomic backdrop is fundamentally different.

In 2013, India needed dollars. In 2026, it is seeking to strengthen an already robust external position while improving domestic liquidity and lowering the economy's cost of capital. With foreign exchange reserves above USD 680 billion, a manageable current account deficit and stronger financial-sector fundamentals, this looks less like a crisisresponse measure and more like a proactive balance-sheet optimization exercise.

India's ability to mobilize overseas capital through its diaspora is not new.

From India Development Bonds in 1991 and Resurgent India Bonds in 1998 to India Millennium Deposits in 2000 and the FCNR(B) scheme in 2013, policymakers have repeatedly leveraged a unique structural advantage: access to a large and globally diversified NRI investor base. What makes the 2026 programme particularly noteworthy is that it has been launched in the absence of an actual external funding crisis.

At its core, FCNR(B) is a mechanism for importing dollar liquidity into the Indian banking system. NRIs place foreign currency deposits with Indian banks, earning dollardenominated returns while remaining insulated from rupee depreciation. Banks gain access to foreign currency funding and India benefits from an inflow of stable external capital.

The success of the 2013 programme stemmed from the RBI's concessional swap facility, which significantly reduced hedging costs and made participation attractive.

The 2026 framework goes a step further, with more supportive terms on hedging, broader eligibility and the potential use of leverage, raising the possibility that inflows could match or may be even exceed the levels achieved in 2013.

To understand why, it is worth revisiting the circumstances that made the original FCNR(B) programme so effective.

Chapter One: When India Was One of the Fragile Five

To appreciate the significance of the 2013 FCNR(B) programme, it is worth remembering how vulnerable India appeared at the time

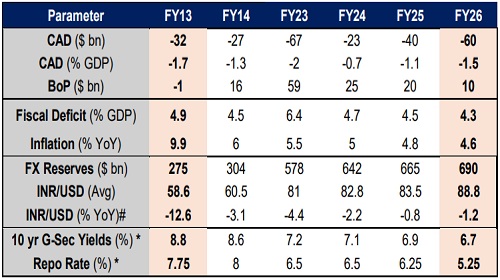

The current account deficit had widened to a record 4.8% of GDP. Inflation remained elevated, fiscal deficits were large and the economy had become increasingly dependent on foreign capital to finance its external imbalance.

What appeared manageable in a world awash with liquidity suddenly became far more precarious when global conditions began to change and that change arrived in May 2013…

When Federal Reserve Chairman Ben Bernanke first hinted at tapering quantitative easing, investors rapidly reassessed emerging-market risk. The resulting "Taper Tantrum" triggered a broad flight of capital from developing economies. Currencies weakened, bond yields rose and countries with large external financing requirements found themselves under intense scrutiny.

And India was among the most exposed economies…

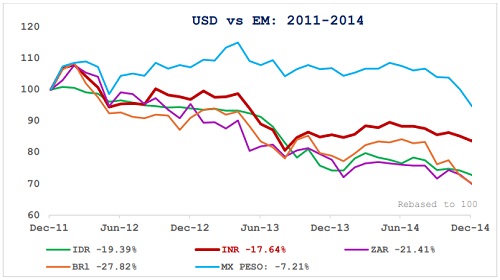

The rupee depreciated from around ?55 per dollar to nearly Rs69 within months. Foreign investors reduced exposure, sovereign risk premia widened and India was grouped alongside Brazil, Turkey, South Africa and Indonesia in the now infamous "Fragile Five" basket.

By mid-2013, the issue was no longer the rupee alone. Markets were beginning to question India's ability to finance its external deficit without a sharp adjustment in growth, imports or domestic liquidity.

It was against this backdrop that Raghuram Rajan assumed office as RBI Governor in September 2013

What followed is often remembered as an FCNR(B) deposit mobilization programme. In reality, it was a broader confidence-restoration exercise

FCNR(B) deposits already existed. Rajan's innovation was to transform the incentives surrounding them. Banks were allowed to swap NRI dollar deposits with the RBI at a fixed concessional rate of 3.5%, while selected overseas borrowing restrictions were relaxed.

The economics became compelling. Banks could offer attractive returns without bearing the full hedging cost. Investors gained access to yield at a near-zero interest-rate . India gained a rapid source of stable foreign currency funding.

Equally important, the programme changed the market psychology.

At a time when confidence was fading , the RBI demonstrated that it had both the policy flexibility and institutional credibility to mobilize capital at scale.

The signal mattered almost as much as the dollars themselves.

Rajan's intervention succeeded not because it directly defended the currency, but because it restored confidence in India's external balance sheet.

That distinction is important when evaluating the RBI's decision to revisit the same approach in 2026.

Chapter Two: From Fragile Five to Global Growth Engine

The most important difference between 2013 and 2026 is not the policy.

It is India's starting point.

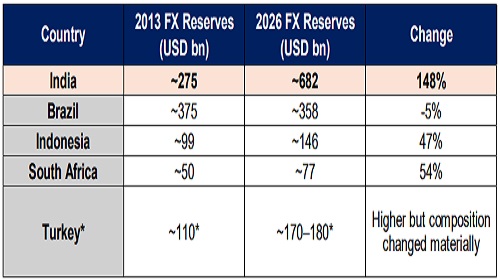

In 2013, investors worried about India's external vulnerability. In 2026, India enters this phase with foreign exchange reserves exceeding USD 680 billion, a manageable current account deficit, stronger banking-sector fundamentals and increasing integration into global debt markets.

Over the past decade, India's macroeconomic profile has undergone a significant rerating.

The election of Prime Minister Narendra Modi in 2014 marked an important turning point in investor sentiment. While reforms evolved gradually over time, perceptions shifted materially. India strengthened its macroeconomic foundations, expanded digital infrastructure, deepened capital markets and improved policy credibility.

The cumulative result has been a transformation in how investors view the country.

India is no longer seen primarily through the lens of vulnerability.

Four Reasons 2026 Is Not 2013

1. India Is Not Fighting a Crisis

The 2013 programme was designed because India needed dollars.

The 2026 programme appears to be designed because the RBI would prefer to have more dollars.

That distinction is critical.

India today has one of the largest reserve buffers in the emerging-market universe. External vulnerability indicators are materially stronger, reserve adequacy metrics remain comfortable and the current account deficit appears manageable.

This looks less like a rescue measure and more like a precautionary step

2. Global Capital Is More Expensive but the Economics are different

The arithmetic that powered the success of 2013 is considerably less favourable today.

In 2013, US interest rates were near zero, Treasury yields were historically low and dollar liquidity was abundant.

Today, investors can earn meaningful returns in US Treasuries, money-market funds and a wide range of alternative assets. The yield differential that once made FCNR deposits attractive has narrowed significantly.

Participation can still be meaningful in 2026. But replicating the extraordinary scale of 2013 will be considerably more challenging.

While the interest-rate differential between India and the United States has narrowed materially over the past decade, the RBI has simultaneously improved the economics of participation for banks and depositors.

The comparison with 2013 is revealing. Under the 2013 scheme, banks bore a concessional swap cost of 3.5% per annum. Under the 2026 framework, the RBI absorbs the entire hedge cost for FCNR(B) deposits. In effect, banks receive fully hedged foreign currency funding at no swap cost

Deposits will also continue to be exempt from Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR) requirements, preserving the funding advantages that made the 2013 programme successful.

The new scheme also permits both fresh and renewal FCNR(B) deposits, unlike the 2013 programme which was limited to fresh mobilization. While this may slightly inflate headline flow numbers, it also broadens the potential pool of participation.

Furthermore, banks can now mobilize deposits with maturities ranging from three to five years, compared with the earlier requirement of three years and above.

Although the macro backdrop is less stressed than in 2013, the economics for banks may be better.

Above views are of the author and not of the website kindly read disclaimer