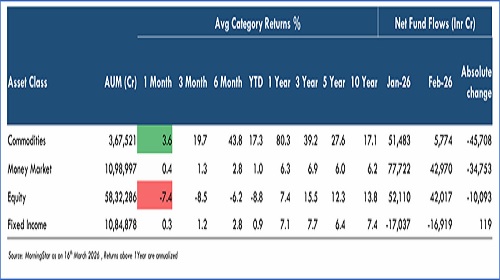

Commodity inflows plunged Rs.45,708 Cr in Feb despite leading 80% 1Y return : Vallum Capital

Commodities: Net fund flows declined from Rs51,483 Cr in January to Rs5,774 Cr in February, a sharp drop of Rs45,708 Cr (~-89%).

Money Market: Net fund flows fell from Rs77,722 Cr in January to Rs42,970 Cr in February, down Rs34,753 Cr (~-45%).

Equity: Net fund flows moderated from Rs52,110 Cr in January to Rs42,017 Cr in February, a decline of Rs10,093 Cr (~-19%).

Fixed Income: Net outflows narrowed slightly from -Rs17,037 Cr in January to -Rs16,919 Cr in February, improving by Rs119 Cr (~+1%).

According to Vallum Capital’s Monthly Macro Grid Chartbook report, total net asset-level flows nearly halved from Rs1,64,277 Cr in January to Rs73,842 Cr in February (-55%). Commodity flows collapsed as gold mania faded, while the money market cooled sharply. Fixed income continued steady outflows, whereas equity flows held relatively firm.

Commodities (Rs5,774 Cr, -89%)

Precious Metals cratered to Rs5,774 Cr from Rs51,483 Cr as gold correction as well as silver saw sharp dip in February after January's surge. Sharpest single-month flow reversal across all asset classes. Retail investors lost interest as momentum faded away in gold and silver.

Money Market (Rs42,970 Cr, -45%)

India Money Market normalized to Rs42,970 Cr from Rs77,722 Cr after January's quarter-end driven spike. February still represents elevated institutional cash preference.

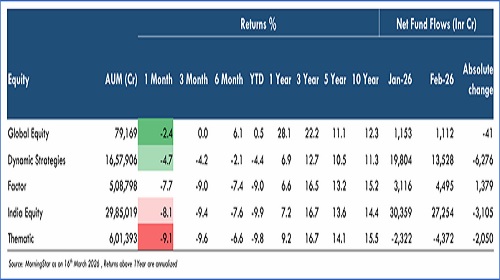

Equity (Rs42,017 Cr, -19%)

- Broad market equity funds moderated to Rs27,254 Cr from Rs30,359 Cr. Large-Cap eased to Rs9,316 Cr from Rs11,007 Cr but remained dominant. Notably, Mid-Cap and Small-Cap moved against the trend — Mid-Cap rose to Rs3,739 Cr from Rs3,297 Cr and Small-Cap to Rs3,055 Cr from Rs2,536 Cr, signaling dip-buying in beaten-down segments. Flexi Cap slowed to Rs6,046 Cr from Rs8,100 Cr.

Broad-based domestic equity correction in the near term (1M: avg -7.4%), fund flows turned cautious as Dynamic Strategies and India Equity saw Rs6,276 Cr and Rs3,105 Cr outflows in Feb-26.

- Global Equity flow saw no major change at inflow of Rs1,112 Cr.

- Dynamic Strategies slowed to Rs13,528 Cr from Rs19,804 Cr. Multi-Asset Allocation remained the anchor at Rs9,060 Cr. Arbitrage dipped to Rs535 Cr from Rs5,075 Cr — the sharpest monthly Inflows equity drop.

- Factor Funds accelerated to Rs4,495 Cr from Rs3,116 Cr, led by Quality at Rs2,261 Cr (from Rs125 Cr) on the back of a new NFO launch absorbing over half the category.

- Thematic outflows deepened to -Rs4,372 Cr from -Rs2,322 Cr. PSU Fund category saw large outflows at -Rs5,389 Cr from -Rs3,859 Cr. On the flip side, Technology was the biggest contrarian winner, flipping to +Rs1,541 Cr from -Rs210 Cr despite a weak -11.1% monthly return. BFSI also turned positive at Rs828 Cr from -Rs205 Cr.

Fixed Income (-Rs16,919 Cr, +1%)

India Fixed Income worsened to -Rs16,919 Cr from -Rs17,037 Cr. Government Bonds were the bright spot, improving to -Rs346 Cr from -Rs1,850 Cr. Core outflow remains entrenched.

February shows January extremes mean-reverting — gold mania cooling, money market normalizing, dip-buying emerging in mid/small caps & tech — while fixed income outflows remain entrenched.

Above views are of the author and not of the website kindly read disclaimer

.jpg)

Tag News

Quote on the AMFI data for July 2026 Nitin Agrawal, CEO, Mutual Funds, InCred Money