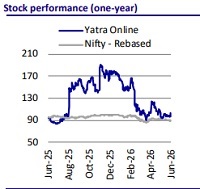

Buy Yatra Online Ltd for the Target Rs.125 by Motilal Oswal Financial Services Ltd.

Play on India’s enterprise travel market

* Yatra Online Limited (YATRA) is India’s largest corporate online travel agency (OTA), serving over 1,300 large and medium enterprise clients along with 58,000 SME customers. The company provides a comprehensive travel offering, enabling bookings across more than 400 domestic and international airlines, access to ~80k Indian hotel properties, a growing base of homestays across ~1,497 cities, and ~2m contracted hotels globally. It also offers end-to-end booking solutions for rail, bus, activities, and other travel services through a single platform.

* YATRA has ~15.6m registered users and 21m mobile app downloads. Notably, ~59% of bookings come from repeat users, while ~81% of traffic is generated through direct and organic channels, indicating strong brand recall value.

* The sizeable ~USD27b B2C travel market (43% online penetration; ~15.6m registered users) and the underpenetrated ~USD16.3b corporate travel market (~22% online penetration) together indicate a structural growth opportunity for the company.

* We expect YATRA to deliver Revenue/EBITDA/PAT CAGR of ~25%/34%/41% over FY26-28E. EBITDA margins are expected to reach 9.2% by FY28E, supported by a favorable shift in GTV and revenue mix, with higher contributions from the Hotel and Packages segment.

* We expect a GTV CAGR of 12%/33%/13% for Air/Hotel/Others, and an overall GTV CAGR of 16% over FY26-28E.

* YATRA’s strategic pivot toward the B2B segment is clearly reflected in its revenue mix, with B2B now contributing ~65% of overall gross booking value (GTV) vs just 21% in FY22. Given management’s continued focus on corporate travel, MICE, and enterprise solutions, this share is likely to expand further and potentially cross 80% over the medium term.

* The new CEO has outlined several strategic priorities:

1) focusing on the SME client segment to drive demand

2) establishing an elite team with a focus on acquiring large corporate accounts every quarter

3) creating a specialized team to retain the existing client base over the long term and increase wallet share through upselling and cross-selling initiatives.

* AI initiatives, such as DIYA AI, are expected to optimize workforce headcount by 70-75 employees in the near term and ~200 employees in the long run.

Play on a highly fragmented enterprise travel market

* We believe YATRA is well placed to gain market share from smaller agents and unorganized players due to its strong supply network and comprehensive offering.

* ~22% of corporates rely on travel management companies like Yatra and others, while ~30% use captive and semi-organized modes. This implies that ~48% of enterprises still rely on small and unorganized travel agents, representing a large addressable opportunity for YATRA and other OTAs.

View and valuation

* We believe YATRA is uniquely positioned as a top-tier franchise in the B2B OTA and MICE space, while its B2C segment offers attractive cross-selling and monetization opportunities.

* The company’s strategic focus on expanding high-margin and sticky B2B revenue streams is clearly evident from its GTV contribution, which increased from ~32% in FY23 to 65% by 4QFY26. We believe there is still significant runway for growth, as only ~22% corporates currently rely on digital travel management companies like Yatra for booking needs.

* YATRA’s B2B segment caters to~1,300 large and mid-sized enterprises, with an addressable employee base of ~9m, providing substantial cross-selling opportunities at significantly lower customer acquisition costs while supporting the scale-up of its B2C business.

* Notably, the continued expansion of the Hotel & Packages segment in overall revenue and GTV mix is expected to support higher margins and improve profitability going forward.

* We expect YATRA to deliver Revenue/EBITDA/PAT CAGR of ~25%/34%/41%, and GTV growth of 16.4% over FY26-28E. We believe contribution margins will expand 100bp amid changes in GTV and revenue mix, with EBITDA margins likely to expand to 9.2% by FY28E from 8.0% in FY26. We initiate coverage on YATRA with a BUY rating and a TP of INR125. We value the company at 21x P/E on FY28E EPS, indicating a 21% upside

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)

2.jpg)