Buy Tbo Tek Ltd For Target Rs.1,485 by Motilal Oswal Financial Services Ltd

Resilient performance in a challenging time

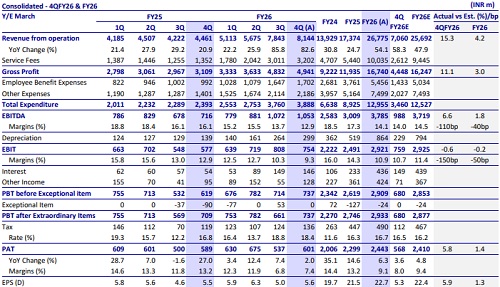

* TBO Tek reported a resilient 4QFY26 performance despite geopolitical disruptions across key travel corridors. Revenue jumped 83% YoY to INR8.14b (est. INR7.06b), aided by the consolidation of Classic Vacations, while organic revenue grew 21% YoY to INR5.42b.

* 4Q MTB reached 32,751 (+15% YoY) on a reported basis and 30,063 (+6% YoY) organically.

* 4Q EBITDA stood at INR1.05b (est. INR988m) and margin came in at 12.9% (est. 14.0%), and FY26 EBITDA stood at INR3.78b (est. INR3.72b) and margin came in at 14.1% (est. 14.5%). * During 4Q, PAT increased by 2% YoY to INR601m (est. INR568m). FY26 PAT was INR2.44b (est. INR2.41b).

* 4QFY26 organic EBITDA margin stood at 15.4% vs. 17.7% in 4QFY25. ? During FY26, consolidated GTV grew 19% YoY to INR368b, while organic GTV grew by 13% YoY to INR347b.

Our view: We expect a strong rebound in travel demand once the global geopolitical situation stabilizes

* The Middle East crisis impacted TBO’s EBITDA by ~INR300-500m (run-rate wise), and in certain ME markets, cancellations exceeded new bookings.

* ME remains one of the largest source markets, and though it is recovering, it has not yet returned to pre-war levels. Management expects that once demand fully normalizes, it is likely to surpass previous peak levels. In Europe, demand remains strong as the diversion of travel from the Middle East to Southern European destinations like Italy, Greece, and Spain has benefited TBO, supported by its broad supply network. Notably, Europe, being a higher take-rate market, has contributed positively to blended margins.

* Domestic airline capacity cuts are temporary, attributed to the oil price surge. International route changes are shifting demand to EU/APAC carriers, and TBO is able to capture this shift. HNI and luxury travelers are still going to Europe, while budget travelers are showing the shift to APAC.

* Management expects 1QFY27 to end positive on YoY and QoQ on both GTV and GP sides, assuming no escalation in geopolitics.

* Debt repayment will commence from 3Q and will continue for four years and management is open to early repayment if cash generation allows.

* Classic Vacation: In the past two quarters, ~50% integration has been completed across platforms, supply and demand channels. TBO expects full integration by the end of 3Q.

Valuation and View

We believe TBO Tek has delivered a strong set of numbers despite a challenging operating environment. Over FY25-28, we expect it to deliver a CAGR of 37%/35%/30% in revenue/EBIT/PAT, mainly on the back of increased contribution from high take-rate hotels and ancillary segments in the GTV mix, We reiterate our BUY rating on TBO with a TP of INR1,485, valued at 32x FY28E EPS

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412