Buy Tata Consultancy Services Limited for the Target Rs 2,825 by Religare Broking Ltd

Strong Q1FY27 Financial Performance: TCS reported a healthy start to FY27 with revenue of Rs 72,275 crore, up 13.9% YoY and 2.2% QoQ, supported by strong BFSI demand, large deal execution and favourable currency movement. Net profit increased 4.7% YoY to Rs 13,420 crore, though growth was impacted by a one-time legal settlement. Operating margin stood at 24%, down 130 bps sequentially due to annual wage hikes, partly offset by operational efficiencies and currency benefits. The company declared an interim dividend of Rs 12 per share, highlighting its strong cash generation and shareholder-friendly capital allocation despite a challenging macro environment.

Healthy Deal Pipeline & AI-Led Growth: TCS secured US$9.5 billion in Total Contract Value (TCV) during the quarter, including an US$800 million mega deal with SKF, marking its sixth mega deal in the last five quarters. Although deal bookings moderated sequentially, the pipeline remains healthy. AI continued to be a key growth driver with annualized AI revenue rising to US$2.6 billion. Strategic partnerships with Anthropic and Mistral AI, along with growing adoption of Agentic AI, are strengthening TCS’ AI capabilities. Management highlighted that AI is increasingly moving from pilots to enterprise-wide deployment, creating long-term growth opportunities.

Demand Trends & Business Outlook: The BFSI segment remained the strongest contributor to growth, while Technology Software & Services also delivered healthy performance. However, Manufacturing, Life Sciences and Consumer businesses witnessed some softness due to macroeconomic uncertainty and cautious discretionary spending. Management indicated that recently won deals in these segments are expected to ramp up over the coming quarters. AIdriven transformation, cloud modernization and cost optimization continue to remain the key areas of client spending. TCS believes enterprises still have a significant technology investment backlog, which should gradually translate into stronger demand as business confidence improves during FY27.

AI Strategy & Talent Investments: TCS continues to strengthen its AI leadership through investments in technology partnerships, platforms and workforce capabilities. The company added over 9,200 employees during the quarter, taking total headcount to nearly 594,000, while onboarding around 14,000 fresh graduates focused on AI-native skills. Employees completed 14.6 million learning hours, adding over 1.3 million new competencies. Management reiterated that AI is expected to enhance productivity rather than replace jobs, creating new opportunities in prompt engineering, AI governance and model lifecycle management. AI-led projects are currently delivering 10-15% productivity improvements, supporting client efficiency and longterm engagement growth.

Strategic Initiatives & Key Monitorables: TCS launched the Sovereign Secure Cloud for Europe to address increasing demand for data sovereignty and regulatory compliance. It also established a dedicated Global Value & Innovation Center to support enterprises in setting up and transforming Global Capability Centers (GCCs). While execution remains strong, investors should monitor moderation in quarterly deal bookings, pressure on operating margins from wage hikes, and weak discretionary spending across select verticals. Manufacturing and Consumer demand remain soft, although management expects gradual improvement. Continued execution in AI-led transformation and large cost optimization programs will remain key drivers for sustaining longterm growth.

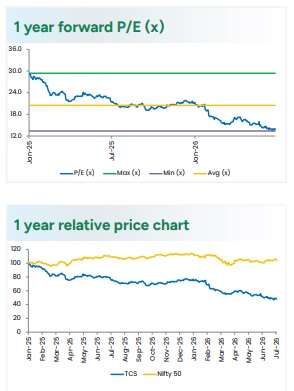

Outlook & Valuation: Management remains optimistic that demand will improve from Q2FY27, supported by AI adoption, cloud transformation, cost optimization programs and the ramp-up of recently won deals. Recovery in Manufacturing and Life Sciences, along with continued strength in BFSI, is expected to support growth over the medium term. While near-term revenue may remain influenced by cautious enterprise spending and lower sequential TCV, TCS remains well positioned given its strong client relationships, robust execution capabilities and leadership in AI services. We estimate Revenue/EBIT/PAT CAGR of 4%/2.9%/2.6% over FY26-28E and maintain a BUY rating with a target price of ?2,825

Please refer disclaimer at https://www.religareonline.com/disclaimer

SEBI Registration number is INZ00017433