Buy Sunteck Realty Ltd for the Target Rs. 530 by Motilal Oswal Financial Services Ltd

Pre-sales growth momentum to continue

Stepped up the BD activity; healthy launch pipeline in FY27

In FY26, Sunteck Realty (SRIN) expanded its MMR portfolio by adding three new projects, offering a combined GDV potential of ~INR50b. The total cash outlay of INR8.1b towards business development in FY26 was notably higher than INR1.8b in FY25. These would offer additional avenues of growth over the medium term. The company has a launch pipeline of INR60-70b, including projects in Andheri, Mira Road, Vasai, and Naigaon. The Dubai project is launch-ready, and the timing would depend on the evolving dynamics in West Asia. The Dubai launch would provide an additional delta to its pre-sales growth.

Pre-sales likely to clock a 23% CAGR over FY26-28E

SRIN reported pre-sales growth of 22% YoY to INR10.6b in 4QFY26 on the back of strong contribution from the uber-luxury segment (57% share) and healthy response at the Avenue 5 project. Consequently, FY26 pre-sales grew by 25% YoY to INR32b. The company’s strong launch pipeline worth INR60-70b, would aid its pre-sales in FY27. The management expects growth momentum (seen in FY26) to sustain in the current year. We bake in a 23% CAGR in pre-sales to reach INR48b over FY26-28E.

Healthy cash flows; balance sheet remains sturdy

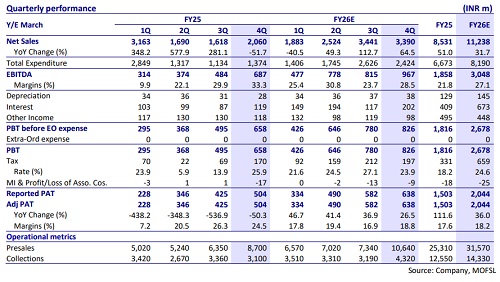

Collections grew by 14% YoY to INR14.3b in FY26, supported by a strong 39% YoY growth to INR4.3b in 4QFY26. SRIN expects better collections growth in FY27. Further, the net operating cash flow (NOCF) surplus at INR5.5b in FY26 (up 48% YoY) is the highest in the last 7 years. Consequently, NOCF-to-collections at 39% was among the best levels since FY21. Net debt-to-equity remained low at 0.06x (excluding loans to JDA partners) despite a robust ramp-up in the BD activity. Fueled by continued pre-sales growth and healthy project execution, we expect collections to record 22% CAGR to reach INR21b over FY26-28.

P&L highlights

In 4QFY26, revenue was up 65% YoY to INR3.4b. The company reported EBITDA of INR967m, up 41% YoY. EBITDA margin contracted 482bp YoY to 28.5%. Adj. PAT stood at INR638m, up 27% YoY. PAT margin was at 19%. In FY26, revenue was up 32% YoY to INR11.2b. EBITDA was at INR3b, up 63% YoY. EBITDA margin stood at 27% vs 22% in FY25. Adj. PAT stood at INR2b, up 36% YoY.

Key highlights from the management commentary

* Management aims to sustain the pre-sales growth rate of 25% YoY in FY27 too (similar to FY26).

* In 4QFY26, pre-sales contribution from the uber-luxury segment, i.e., the BKC and Nepean Sea Road projects, was INR6.1b (~57% of quarterly sales).

* Incurred INR8.1b towards business development in FY26 vs. INR1.8b in FY25. It plans to continue investing in BD in the coming quarters.

* FY27 launches: A redevelopment project on WEH in Andheri, an additional tower in Skypark (Mira Road), two towers in Beach Residences (Vasai), and a new phase in Sunteck World (Naigaon). The newly acquired project in Mira Road is expected to be launched in the next 12 months. Overall, it has planned for INR60-70b launch apart from the Nepean Sea Road formal launch in FY27.

* Recently acquired projects would have blended EBITDA margins of 30–35%.

* Sunteck One World in Naigaon is scheduled to be delivered in FY27.

* Construction for the first phase of the Nepean Sea Road project is expected to commence in FY27.

* There is a shortage of labor currently, likely due to the elections in West Bengal – this situation is expected to normalize post-Apr’26.

* The Dubai project is launch-ready, and the company plans to proceed once the Middle East situation stabilizes.

* The company had invested AED130m in the Dubai project.

Valuation and view

* Given the favorable base and healthy launch pipeline, we expect SRIN to deliver 23% presales CAGR over FY26-28E. The recent project acquisitions would support growth over the medium term. Growth in collections and healthy cash flows would support business development vis-à-vis keeping leverage at healthy levels in the coming years.

* We value its residential segment at its NAV (implying a 5.2x embedded EV/EBITDA multiple on FY28E) and commercial segment at an 8.5% cap rate.

* We have BUY rating on the stock with a TP of INR530, implying a 48% upside potential.

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412