Buy SBI Life Insurance Ltd for the Target Rs. 2,350 by Motilal Oswal Financial Services Ltd

In-line performance; VNB margin within guided range

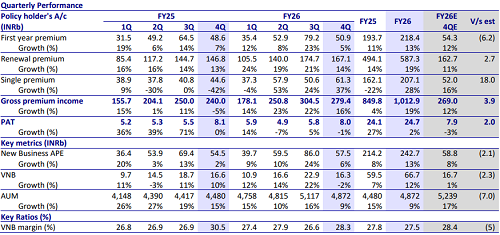

* SBI Life Insurance (SBILIFE) reported 6% YoY growth in new business APE to INR57.5b (in line). For FY26, APE grew 13% YoY to INR242.7b.

* Absolute VNB declined 2% YoY to INR16.3b (in line), reflecting VNB margin of 28.3% for the quarter vs. 30.5% in 4QFY25 (vs. our est. of 28.4%). For FY26, VNB grew 12% YoY to INR66.7b with VNB margin of 27.5%, which was at the upper end of guidance of 26-28%.

* EV at the end of FY26 was at INR807.9b, up 15% YoY, with operating RoEV at 19.7%. SBILIFE reported 1% YoY decline in shareholder PAT to INR8b (in line). For FY26, PAT grew 2% YoY to INR24.7b. Excluding the GST and labor code impact, FY26 PAT stood at INR 31.2b, up 29% YoY.

* Management is confident of sustaining ~14% APE growth trajectory. With an improving product mix and GST impact largely baked in, VNB margins are expected to be in the 27-28% range.

* We have slightly cut our APE estimates and expect ~14% CAGR over FY26- 28E, resulting in a 2% decline in VNB/EV estimates for both FY27/FY28. Operating RoEV is expected to remain stable at 18%. We reiterate our BUY rating with a revised TP of INR2,350 (based on 2.1x FY28E P/EV).

Continued shift toward non-ULIP products

* SBI LIFE reported gross premium of INR279.4b (in line), up 16% YoY, driven by 14% YoY growth in renewal premium and 37% YoY growth in single premium.

* Total cost ratio was 9% vs. 8.4% in 4QFY25, with the commission ratio at 3.1% and opex ratio at 6%. For FY26, opex ratio was above 6% vs. 5.3% in FY25, with the rise driven by GST impact, branch expansion, IT investments, and agent training. Management expects better cost efficiency going forward with no incremental spends planned apart from tech capabilities.

* On the product front, ULIP APE was flat YoY, contributing 52% to total APE (54.3% in 4QFY25). Low base and new product launches resulted in ~3x YoY growth in par APE, raising its contribution to 9% (3% in 4QFY25). Non-par savings declined 9% YoY. Individual protection maintained the strong growth trajectory (+30% YoY), with contribution at 7% of APE (5.5% in 4QFY25). The annuity segment saw 33% YoY growth.

* On the distribution front, the agency channel posted 28% YoY growth, driven by 140%/5%/30% YoY growth in par/non-par/ULIP segments. Management expects the growth trajectory to remain robust with continued investments in agent hiring and productivity improvement. Individual APE in the bancassurance channel declined 5% YoY, with ULIP/non-par down 12%/8% YoY, which was offset by ~4x YoY growth in the par segment. Other channels (brokers, digital, etc.) witnessed 28% YoY growth in individual APE, driven by 2.5x YoY growth in the par segment and 32% YoY growth in non-par, while ULIP was flat YoY.

* The company witnessed improvement across all persistency cohorts, except for 61M, which declined to 56.7% from 61.5% in 4QFY25. 13M persistency was at 87.9% (86.6% in 4QFY25), and 37M persistency increased to 71.7% (70.7% in 4QFY25).

Highlights from the management commentary

* Increase in cost ratio in FY26 was driven by GST impact, branch expansion, IT investments, and agent training. Going forward, incremental costs are expected to be limited, apart from continued IT investments.

* Agency channel has strengthened over the past two years, with increasing contribution. The company continues to invest in agency expansion (branch additions, agent hiring, productivity improvement), along with emerging and direct channels.

* Positive operating variance was driven by conservative assumptions and betterthan-expected business quality, with contributions primarily coming from mortality and persistency (and to a lesser extent expenses).

Valuation and view

* SBILIFE’s 4Q VNB margin was impacted by GST changes, which was offset, to some extent, by a strong traction in protection products, rising rider attachment rates, and a shift in the product mix toward non-ULIP products. Going forward, steady traction in non-linked products is expected to drive VNB margin expansion.

* Continued investments in agency and digital channels are expected to drive overall growth, supported by a gradual growth recovery in the bancassurance channel.

* We have slightly cut our APE estimates and expect ~14% CAGR over FY26-28E, resulting in 2% decline in VNB/EV estimates for both FY27/FY28. Operating RoEV is expected to remain stable at 18%. We reiterate our BUY rating with a revised TP of INR2,350 (based on 2.1x FY28E P/EV).

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412