Buy Mrs. Bectors Food Specialities Ltd for Target Rs 260 by Elara Capital

Expect sequential improvement in margins

Mrs. Bectors Food Specialities (BECTORS IN) delivered 8.9% revenue growth in Q4FY26. In the biscuits segment, the domestic business is trending toward low-to-mid teens growth, partially offset by weak exports due to headwinds from US tariffs and GCC disruptions. The Bakery segment continued with its strong momentum with high teens growth in English Oven, supported by expansion in distribution and traction in quick-commerce. BECTORS expects the Bakery segment to grow in mid-teens and domestic Biscuits to grow in low-tomid teens in FY27, with EBITDA margin recovering sequentially, barring a sharp spike in crude oil price. We reiterate Buy with a lower TP of INR 260 from INR 300 on 40x P/E (from 45x) due to slower-than-expected revenue growth on Dec ’27E EPS.

Biscuits and Bakery – Steady growth:

In Q4FY26, net sales grew 8.9% YoY to INR 4.9bn, in line with estimates. Bakery continued to lead, with retail bakery posting high teens growth led by English Oven (high-teens growth for four consecutive years). Management noted that January and February were strong months, though Navratri falling in March temporarily moderated bread consumption. Domestic Biscuits segment grew by low to mid-teens in Q4. Management expects low-to-mid teens growth in FY27. An INR 5/10 salience now at ~65% is in line with the industry. Export growth was muted in low single digit in Q4 due to US tariffs and limited impact from the US-Iran conflict affecting the GCC region (Bahrain and Kuwait hit; others steady). Management expects the exports business to recover to low-to-mid teens growth in Q1 and Q2 of FY27, aided by reduced US tariffs and new customer onboardings. For English Oven, growth opportunity is in Mumbai followed by Hyderabad and Chennai

Capacity additions, distribution and new launches on track:

The Kolkata plant was successfully commissioned in January, strengthening BECTORS' presence in the East. Regarding distribution, BECTORS is driving expansion in distribution within 400km of the Rajpura, Dhar and Kolkata facilities. Management expects total reach to expand to 0.9-1mn outlets (currently 700k) by FY30E. It expects direct reach of 350k outlets in FY27. The company recently launched NaturBaked Super Protein Bread and English Oven jar desserts

Aims at sequential margin improvement:

Q4 EBITDA margin improved 25bps YoY to 12.7% (in line), with gross margin expanding 186bps YoY (up 114bps QoQ) to 46.2%. Raw material (RM) inflation has emerged as a near-term headwind — palm oil, crude derivatives, and packaging material costs have pushed the overall RM basket up ~3%. Management expects sequential margin improvement in the next two quarters. BECTORS has already taken pricing actions to protect margin and will implement further hikes if RM prices rise further.

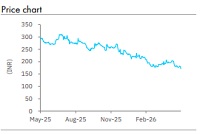

Reiterate Buy; with a lower TP of INR 260:

We cut our earnings estimates by 7.8%/6.7% in FY27E/28E to factor in lower revenue and EBITDA margin. We reiterate Buy with a lower TP of INR 260 from INR 300, on 40x P/E (from 45x) due to slower than expected revenue growth on Dec ’27E EPS as we roll forward. We introduce FY29E.

Please refer disclaimer at Report

SEBI Registration number is INH000000933