Buy Mrs Bector Foods Ltd for the Target Rs. 235 by Motilal Oswal Financial Services Ltd

Weak exports; domestic business growth in line

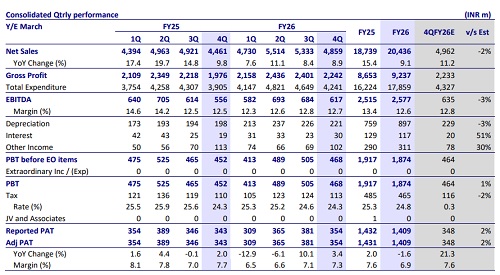

Mrs. Bectors Foods (MBFSL)’s consolidated revenue grew 8.9% YoY to INR4.8b in 4QFY26, led by strong performance in the bakery segment (+8.9% YoY; B2C – high teens and QSR – mid-single digit). Biscuits grew 8.2% YoY, led by high singledigit growth in the domestic segment, while exports reported low single-digit growth. Management guides a low-to-mid-teen revenue growth in FY27, led by mid-teens growth in Bakery, low-to-mid-teen growth in Biscuit exports, and high single-digit growth in domestic biscuits and QSR. EBITDA margin improved to 12.7% (+25bp YoY) despite export incentive suspension and management’s target EBITDA margins of ~13–13.5% by FY27. We expect Revenue/EBITDA/APAT to clock 13/18/22%, respectively, over FY26-28.

Management expects low-to-mid-teen growth, led by bakery & exports

MBFSL surpassed the INR20b revenue milestone in FY26, driven by mid-teens growth in bakery, followed by high single-digit growth in export of biscuits and low single-digit growth in domestic biscuits. While FY26 growth remained hit by GST-led pricing disruptions, US tariff uncertainties, and West Asia conflict, management guides a low-to-mid-teen revenue growth in FY27, led by midteens growth in bakery, low-to-mid-teen growth in biscuit exports, and high single-digit growth in domestic biscuits and QSR. In 4Q, exports of biscuits were affected by higher competition in Latin America, along with tariff-related issues, whereas bakery demand remained healthy despite temporary Navratri-led softness. The company is expanding its geographic footprint, strengthening its presence in Kolkata and Hyderabad while planning to enter new markets such as Chennai and Ahmedabad, alongside deepening its distribution network in Mumbai. On distribution, the company aims to add 40k outlets by FY27 from ~310k currently, focusing on expansion within a 400km radius of its plants.

Margin improves YoY, led by product mix; expect improvement in 1H

In 4Q, gross margin came at 46.2% (+190bp YoY, led by product mix). EBITDA stood at INR617m (+11.1% YoY), settling EBITDA margin at 12.7% (+25bp YoY), despite an increase in employee costs (+19.5% YoY) and other expenses (+10.8% YoY). APAT grew 3.4% YoY to INR354m despite higher interest expense (+58.6% YoY). With ~3% raw material inflation, the company plans calibrated price hikes to protect margins, targeting EBITDA margins of ~13–13.5% by FY27.

Financial highlight for FY26

Consolidated revenue grew 9.1% YoY to INR20.4b, backed by mid-single-digit volume growth. Gross margin contracted by 100bp YoY to 45.2%. EBITDA stood at INR2.5b (+2.5% YoY), recording an EBITDA margin of 12.6% (-80bp YoY). The Board has recommended a final dividend of INR0.7/share, taking the total dividend to INR1.3/share for FY26. The company is net debt positive and has generated an FCFF of INR35m as of Mar’26, alongside maintaining a cash conversion cycle in the range of 33 days.

Valuation and view:

Reiterate BUY We expect MBFSL to deliver a 13% revenue CAGR over FY26-28, driven primarily by 1) strong growth in domestic bakery, 2) premiumization and health-focused innovation, and 3) growth in export revenue after the reduction in tariffs. Domestic biscuits and QSR remain the weaker growth segments. We believe distribution expansion in the domestic market (especially in the lower North) and export growth will be a key monitorable. We trim our earnings and reiterate our BUY rating with a DCF-based TP of INR235 (based on an implied P/E of 34x for FY28). Key risks: potential supply chain disruptions impacting production and distribution/execution risks related to plant consolidation.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412