Buy JK Cement Ltd For Target Rs. 5,183 by Centrum Broking Ltd

Decent performance despite odds

JK Cement (JKCE) reported decent results for Q3FY25 as revenue at Rs29.3bn was largely in-line with our estimate but EBITDA was slightly below estimate owing to higher than expected costs. The company reported 5% YoY growth in Grey Cement volume and 6% in White Cement. Given the challenging conditions, we believe that realizing Rs1,000/mt EBITDA is a good achievement. Overall, the company’s journey is on track with addition of 6mn mt capacity expected in MP, Bihar and UP by Q4FY26. The management announced the acquisition of a small J&K based player, which will help the company in establishing presence in the state. We have maintained our estimate and rating on the stock.

Q3FY25 result highlights (consolidated)

Revenue at Rs29.3bn was flat YoY and up 14.5% QoQ. Aggregate volume at 4.9mn mt was up by 5% YoY and in-line with our estimate. Blended realizations were up 1.7% QoQ. Grey Cement volume increased by 5% while White Cement volume was up by 6% YoY (including JK Cement UAE operations). Grey Cement realization was up 1% QoQ (below our estimate of 2.5% increase) while White Cement realization was up 2.5% QoQ. Operating cost at Rs4,956 increased by 1% YoY and was 2% ahead of our estimate. EBITDA at Rs4.9bn was down 21% YoY and 6% below our estimate. EBITDA/mt came in at Rs1,000 against our expectation of Rs1,062.

Capex plan on track; acquisition of Saifco Cement announced

The company’s expansion plan is on track as 2mn mt GU Prayagraj is already commissioned in record time. Recently announced 6mn mt expansion at Panna (MP) and Bihar is expected to be commissioned by Q4FY26. Total capex for FY25/FY26 is pegged at Rs19bn/Rs17bn. The company announced the acquisition of Saifco Cements, which is based in Sri Nagar, Jammu & Kashmir. At present, it has 0.42MTPA capacity and 0.26MTPA clinker capacity. JK proposes to acquire 60% equity for Rs1.75bn by share subscription agreement. Saifco plant currently operates at 40% efficiency. JK plans to double Saifco capacity in one year. The plant is profitable with ~Rs1,500 EBITDA/mt.

Cost reduction of Rs150-200/mt planned over the next 2-3 years

The company has maintained its cost reduction target of Rs150-200/mt over 2-3 years. In FY25, it expects to accrue cost savings of Rs30-40/mt through logistics initiatives, Rs20-30/mt through green power and AFR usage. Total cost savings would be Rs70- 75/mt in FY25.

Valuation and Outlook

JKCE’s successful capacity addition template has yielded better results in the form of superior volume growth and we believe it will continue to help JKCE to expand its market share in its existing markets. Bihar Grinding unit coupled with gradual ramp-up of Toshali Cement would also aid in enhance its geographical diversification. New capex will deliver ~325bps improvement in ROCE over FY24-FY26E. We maintain our BUY rating with a target price of Rs5,183 based on 14x Mar’27 EV/EBITDA.

Valuation

We are building in 10%/16% CAGR in Revenue/EBITDA for JKCE over FY24- FY27E. We value it at 14x FY27E EV/EBITDA to arrive at our revised target price of Rs5,183.

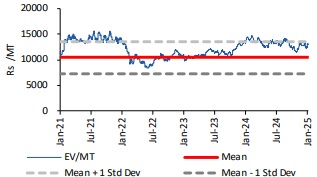

EV / MT mean and standard deviation

EV/EBITDA mean and standard deviation

For More Centrum Broking Disclaimer https://www.centrumbroking.com/disclaimer/

SEBI Registration No.:- INZ000205331