Buy Godrej Consumer Ltd for the Target Rs. 1,300 by Motilal Oswal Financial Services Ltd

Weak international margin; near-term cost pressure persists

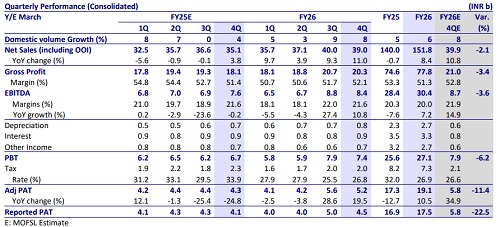

* Godrej Consumer’s (GCPL) consolidated revenue rose 11% YoY to INR39b (est. INR39.9b) in 4QFY26, while volume growth stood at 6%. EBITDA grew 11% YoY (est. 15%), dragged down by lower-than-expected international business performance. India EBITDA grew by 19% YoY, while international EBITDA fell 4% owing to high brand investments.

* India revenue rose 10%, with underlying volume growth of 8% YoY, driven by innovation and improved execution on the ground. Home Care delivered 12% revenue growth, while personal care sales rose 3% YoY. Considering RM inflation, GCPL has taken a price hike of 5% in soaps and HI portfolios and 6-7% in detergents. Most of these price hikes are taken in Apr’26.

* International revenue rose 15%, led by 20% growth in GAUM. Indonesia grew 3% (with 4% UVG) and LATAM rose 26%. Management said that pricing pressure in Indonesia has bottomed out and that operating conditions should improve from FY27. EBITDA for Indonesia/GAUM grew by only 1%/2%, dragging down overall profitability.

* India’s GM expanded by 90bp YoY to 52.3%, while EBITDA margin expanded by 200bp YoY to 24.9% (in line). EBITDA grew 19% YoY to INR5.9b (est. INR6.1b), aided by lower ad spends. GCPL expects India business to deliver continued, calibrated growth at normative EBITDA margins (guided range of 24-26%) going ahead. That said, GCPL stated that 1HFY27 margins can be slightly compressed compared to 1HFY26.

* The India business is witnessing steady improvement, with personal wash showing a positive trajectory. HI portfolio is gaining market share across segments, and GCPL is taking various initiatives to reduce seasonality. Given volatile RM scenario, GCPL has taken price hikes in the range of mid-single digit across its portfolio. Near-term raw material pressure delays the margin recovery for the company. We expect improvement in international business profitability in FY27. We model 12%/16% revenue/EBITDA CAGR for FY26-28E. Given its focus on growth, we reiterate our BUY rating on GCPL with a TP of INR1,300 (based on 45x Mar’28E EPS).

India performance shines with UVG of 8%

* Strong India performance: Net sales (including OOI) grew 10% YoY to INR23.4b in 4QFY26 (est. INR23.9b). India business reported underlying volume growth of 8% YoY (7% excluding Muuchstac). Home Care business registered 12% revenue growth, while Personal Care posted 3% growth. Gross margin expanded by 90bp YoY to 52.3%, while GP was up by 11% YoY. EBITDA margin expanded by 200bp YoY to 24.9% (est. 25.1%). EBITDA grew 19% YoY to INR5.9b (est. INR6.1b), aided by lower ad spends. PAT stood at INR4.2b (est: INR4.1b).

* Muted international print; margin pressure across geographies: Indonesia delivered 4% UVG and 3% sales growth (1% CCG) led by Shampoo HC and Baby care. GCPL said that Indonesia pricing pressure largely bottomed out and it is seeing early signs of stabilization. EBITDA grew by a mere 1% in 4QFY26. GAUM business delivered revenue growth of 20% in INR (6% CCG), led by Hair Fashion and scale-up of Air Fresheners. However, EBITDA fell 4% YoY as GCPL continued to invest in media for its FMCG categories in the region.

* Consolidated revenue in line, but EBITDA below est.: Consolidated net sales grew 11% YoY to INR39b (est. INR39.9b). Consolidated volume growth was 6%. Gross margins expanded 70bp YoY to 52.1% (est. 52.8%). EBITDA margin remained flat YoY at 21.6% (est. 21.9%). Employee expenses rose 24% (on a base of -19%) and other expenses were up 17.5% (on flat base), while ad spends were down 2% YoY (on a base of -8%). EBITDA was up by 11%. Depreciation rose 5%, while interest costs stood flat. However, lower taxes (down 12% YoY) led to 20% growth in APAT to INR5.2b (est. INR5.8b).

* FY26 consolidated sales grew by 9% YoY with UVG of 6%. EBITDA/APAT grew 8%/13%

Highlights from the management commentary

* GCPL said that underlying consumption remains stable, with some distortion in soaps due to pack-size changes rather than demand weakness.

* The portfolio mix continues to improve, with home care gaining share vs. soaps, which is structurally positive for margin.

* Considering RM inflation, GCPL has taken ~5% price hike in soaps and HI portfolios and 6-7% in detergents category. Most of these price hikes are taken in Apr’26.

* 1HFY27 margins can be slightly compressed compared to 1HFY26.

* Godrej Fab generated ARR of INR5b in FY26 and is largely near the breakeven at EBITDA level.

Valuation and view

* We maintain our EPS estimates for FY27-FY28.

* Management remains committed to improving Indian business volumes and optimizing efficiencies across the value chain. Going forward, the GAUM business is expected to deliver improved profitability growth. Indonesia's recovery is anticipated to start meaningfully from FY27 as market conditions normalize. Management is confident of sustaining profitability momentum into FY27, despite the macroeconomic headwinds.

* The company is expanding its TAM by foraying into new, faster-growing categories, such as men’s face wash and toilet cleaners, and continues to strengthen its core portfolio. Besides, the company has made consistent efforts to address gaps in profitability and growth across its international business. Given the growth-centric focus, we remain constructive on GCPL and reiterate our BUY rating with a TP of INR1,300 (based on 45x Mar’28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)