Buy Dr. Agarwal's Health Care Ltd for the Target Rs 610 by Motilal Oswal Financial Services Ltd

In-line revenue, margin beat; premiumization and surgery mix deliver again Network expansion on track; new centers ramping up well; earnings visibility intact

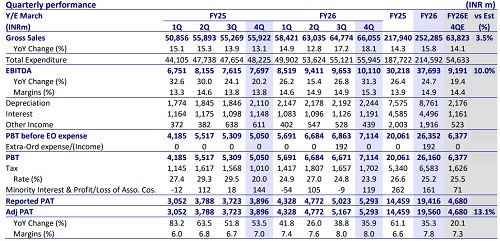

* Dr. Agarwal Healthcare (DAHL) delivered largely in-line revenue and betterthan-expected EBITDA/PAT (8% beat) in 4QFY26. The increased share of surgeries and higher premiumization boosted profitability in 4Q. DAHL beat EBITDA/PAT estimates for the third consecutive quarter in 4Q.

* Interestingly, DAHL achieved the highest-ever quarterly EBITDA margin of 28.6% (Post-IND-AS basis).

* DAHL delivered robust compounding growth of 14% in revenue from facilities set up prior to FY24. Facilities added in FY24/FY25 reported strong revenue growth of 16%/71.6%, implying healthy patient acceptance at new centers. New centers were added to increase the reach within its existing micro markets and to expand to additional micro markets.

* Among regions, South remained the biggest revenue growth driver with 22.6% YoY growth in FY26, followed by North (20.7%), West and East (19% YoY each).

* DAHL added 56 new centers in FY26, and aims to add another 60 in FY27.

* We raise our earnings estimates by 3% each for FY27/FY28, factoring in a robust pace of facility additions, a faster scale-up of existing facilities, and premiumization of high-end surgeries. We value DAHL (25x EV/EBITDA for the surgery business, 15x EV/EBITDA for the opticals business, 10x EV/EBITDA for the pharmacy business, adj. for a stake in Dr. Agarwal Eye Hospital/Thind hospital) and arrive at a TP of INR610.

* FY26 performance was broad-based, with 23.7% YoY growth in patients served and 14.5% YoY growth in surgeries performed. Even region-wise, growth was well-diversified. Given deeper penetration, addition of facilities and doctor talent, and strong brand recall, we expect 22%/23%/40% CAGR in revenue/EBIDTA/PAT over FY26-28, effectively driving return ratios toward mid-teens over the next three years. Reiterate BUY.

Solid quarter caps off strong FY26 earnings growth

* DAHL’s 4QFY26 revenue grew 22.6% YoY to INR5.6b (our estimate: INR5.5b).

* EBITDA margin contracted 30bp YoY to 28.6% (our estimate: 27.2%).

* Consequently, EBITDA grew 21.4% YoY to INR1.6b (our estimate: INR1.5b).

* Adj. PAT came in at INR388m in 4QFY26, up 8.4% from INR358m in 4QFY25.

* For FY26, revenue/EBITDA/PAT grew 22%/26%/59% YoY.

Highlights from the management commentary

* DAHL expects to sustain this growth momentum in FY27, led by deeper penetration in existing markets, addition of greenfield centers, and the implementation of new technologies.

* DAHL also expects to sustain EBITDA margin in FY27.

* DAHL is targeting to add 60 facilities in FY27, comprising 30 surgical facilities. ~24 would be added in South and 16 would be added in North. West is expected to witness 15 new additions. The facilities would be added on organic basis.

* FY27 capex would be INR3.8b for facility additions. Acquisition-related payment would be INR600-650m in FY27.

* The merger of Dr. Agarwal Eye Hospital with DAHL would be completed by Nov/Dec’26

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412